Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Instructor: Katya Malinova

Course : F741 Fall 2023

Application: DeFi lending

borrowing/lending

on-chain ability to exchange arbitrary value

Idea:

Sidebar: what is a DAO?

1 ETH

(1 ETH = $1,577)

(Feb 15, 2023)

\(\approx\) $1,500

\(\vdots\)

1,500 DAI

(1 DAI = $1)

formally: this smart contract is a collateralized debt position (CDP)

fractional collateral \(\to\) collateralization factor \(=\) 150%

total collateral = $1,500

maximum loan = $1000

overcollateralization = $500

actual loan (example) = $500

buffer = $500

ETH \(\nearrow\) $2,000

value of ETH collateral = $2,000

maximum loan = $2,000/150%=$1,333

total collateral = $2,000

maximum loan = $1,333

overcollateralization = $667

actual loan (example) = $500

buffer = $500

overcollateralization = $667

new loan capacity= $333

ETH \(\searrow\) $750

value of ETH collateral = $750

maximum loan = $750/150%=$500

total collateral = $750

maximum loan = $500

overcollateralization = $250

actual loan (example) = $500

buffer = $0

for reference: former value of collateral

ETH \(\searrow\) $600

value of ETH collateral = $600

maximum loan = $600/150%=$400

total collateral = $600

maximum loan = $400

required overcollateralization = $200

actual loan (example) = $500

buffer = -$100

for reference: former value of collateral

\(\Rightarrow\) triggering of liquidation auction by "keeper"

sell 3.33 ETH=$500=500 DAI

repay $500=500 DAI loan

retain incentive

return remainding ETH to vault owner

\(\Rightarrow\) all relies on behavioral assumptions

\(\Rightarrow\) But: there are also real incentives & mechanisms

borrowers of DAI need to pay interest \(\to\) stability fee

DSR paid on "locked" DAI

total amount of debt (or DAI) outstanding is limited

Sidebar: how is this decided?

\(\to\) special "governance" token MKR

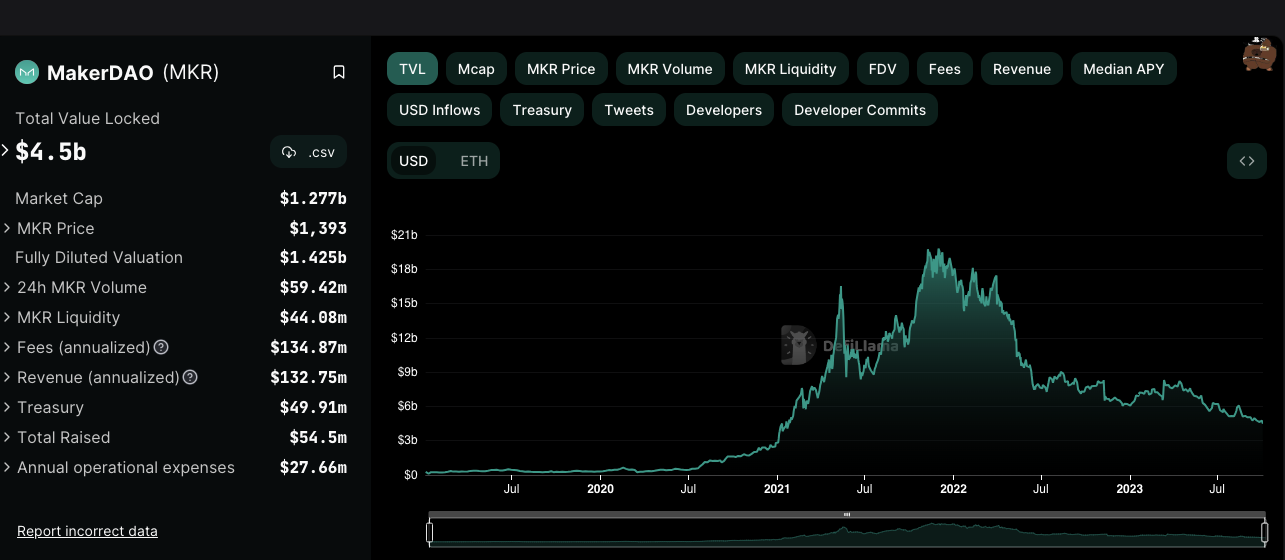

Source: daistats.com (Oct 27, 2021)

Source: daistats.com (Oct 26, 2022)

The Problem:

The Solution:

Note: In May 2021, ETH prices dropped again by >30% but no drama in DAI

Interest rates influenced by the FED, access to loan products controlled by regulation and institutional policies

MakerDAO platform is openly controlled by the MKR holders.

Difficulty of obtaining loans for large majority of population

Open ability to take out DAI liquidity against an overcollateralized position in any supported token.

Costs of time and money to acquire a loan

Instant liquidity with minimal transaction costs.

Can't seamlessly use the same USD (esp. outside the US)

DAI, a permissionless USD-tracking stablecoin backed by cryptocurrency. DAI can be used in any smart contract or DeFi application.

interoperability

inefficiency

centralized control

limited access

opacity

Unclear collateralization of lending institutions.

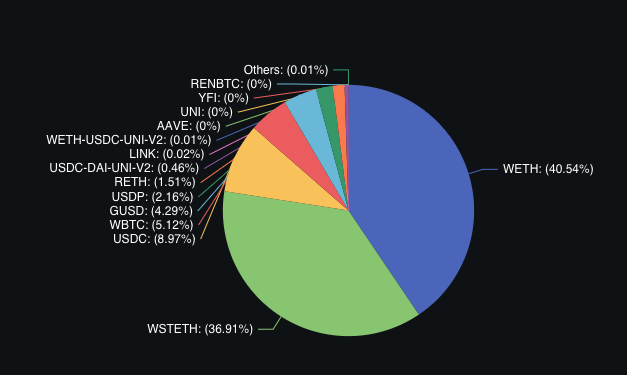

Transparent collateralization ratios of vaults visible to entire ecosystem

TradFi

MakerDAO

MakerDAO bought another $700 million U.S. Treasurys, taking the total to $1.2 billion [...]

[... ]to diversify the assets backing the $4.5 billion dollar-pegged stablecoin

Application: DeFi lending:

Compound (and Aave)

Fundamentally, what does a bank do?

And how is this done?

on blockchain

Nothing new is minted

Example 1

Example 2

Example 3

In Compound

translated to c-tokens (example, can be different conversion)

new deposit

1,000 DAI

100 cDAI

500 DAI

add 50 new cDAI

In Compound

translated to c-tokens

new deposit

1,000 DAI

150 cDAI

500 DAI

1 year later: 10% interest on compound

150 DAI

(same cDAI, each cDAI is worth more)

interest

common theme in DeFi: jumping between dApps

Source: Harvey, Ramachandran, and Santoro (2020)

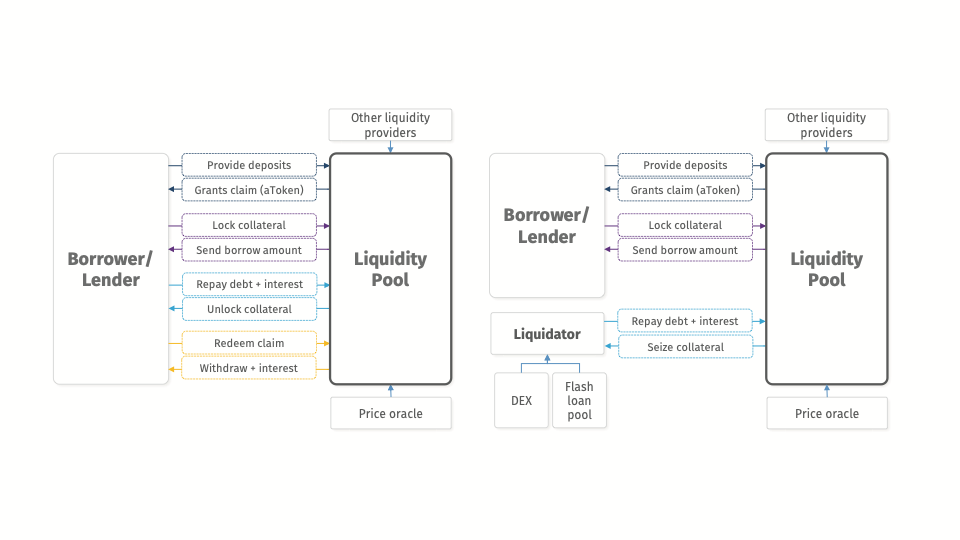

The Flow of Event: Normal Times

The Flow of Event: Collateral Liquidation

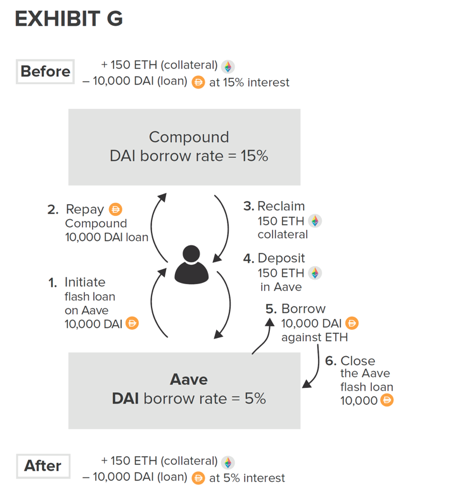

1. flash-borrow DAI

5. repay DAI

3. receive the collateral (ETH) at a discount

4. convert ETH to DAI

2. liquidate ETH-collaterilized loan with DAI

Loan liquidation opportunity

either all of these execute or none -> true arbitrage

Stopped here in lecture 4

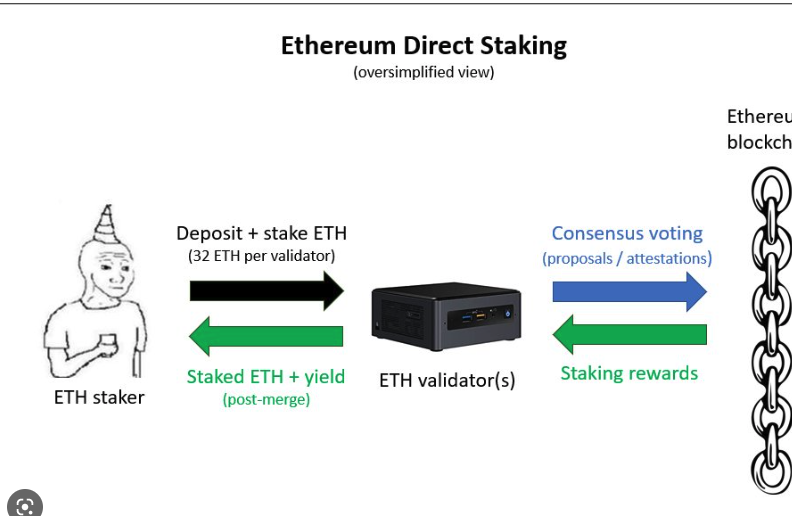

Staking: One word, multiple meanings

Very loosely: locking in the funds

Staking as a Validator

Similar rule in Canada: look up "Pacific Coin test"

When is it a security (SEC point of view)?

In the case of Howey, the buyers of the Florida citrus groves saw the transactions as valuable primarily because the labor and expertise were provided by others. Buyers only needed to invest capital to access an income stream.

Staking More Broadly & Yield Farming

Staking in DeFi

Staking in DeFi: Why?

"Yield farming"

Many automated DeFi products are emerging

Obvious Smart Contract Application: Automate Investment Strategies

"yield aggregator:" push capital where rate of return is highest

Caution: "yield farming" has its risks ....

Odd Lots: SBF and Matt Levine on How to Make Money in Crypto (podcast, April 25, 2022)

If too pressed for time to listen, start at minute 21:17, or check out:

And yet: staking, lending, and supplying liquidity on DEXes - at least in theory - allows (non-expert) investors to passivley participate in and benefit from the promise/growth of cryptoassets

For a more rigorous analysis (not for F741), see Augustin, Chen-Zhang, and Shin, Donghwa, "Reaching for Yield in Decentralized Financial Markets"

https://ssrn.com/abstract=4063228

"investors chase farms with high yields and that [...] farms with the highest headline rates record the most negative risk-adjusted returns"

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

By Katya Malinova

This is an intro to DeFi (DeFi Lending) for F741 in the Fall of 2023.