Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Instructor: Katya Malinova

Course : F741 Fall 2023

A quick recap

blockchain=

an infrastructure for digital resource transfers

software protocols that allow multiple parties to operate under shared assumptions and data

without trusting each other.

Updates are packaged into “blocks” and are “chained” together cryptographically to allow an audit of the prior history

cryptocurrency =

internal payment mechanism to pay for operation of a blockchain

Consensus Protocol =

a set of rules that determine what kinds of blocks can become part of the chain and become the “truth”.

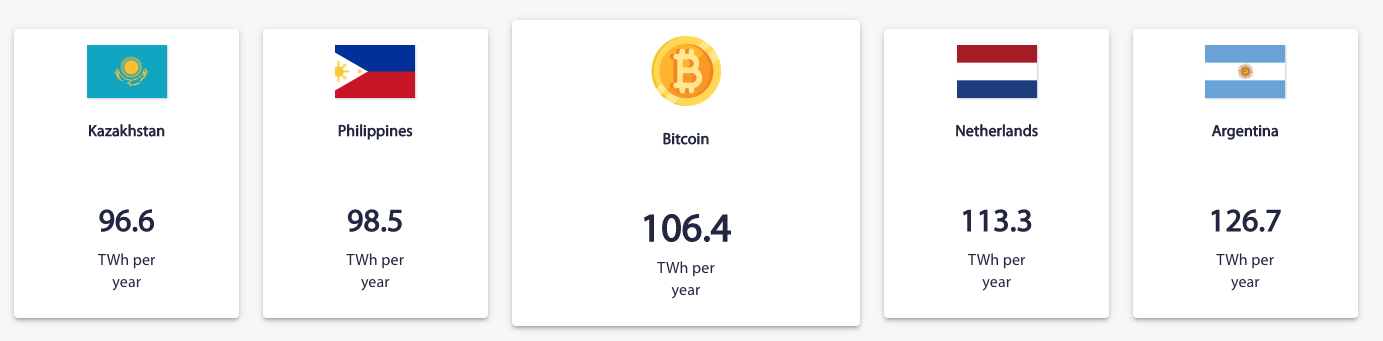

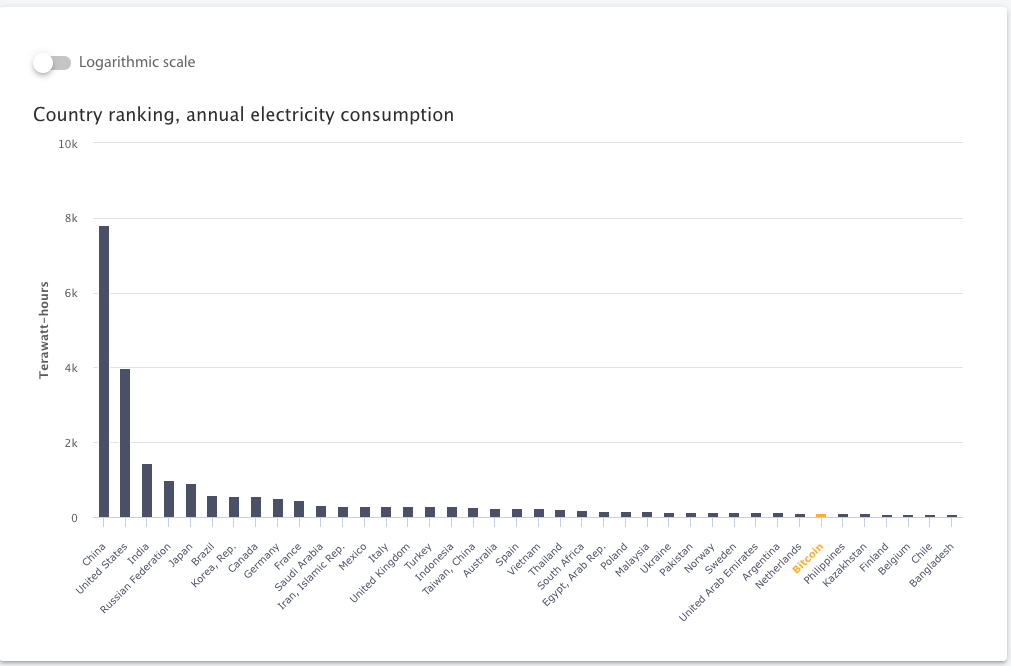

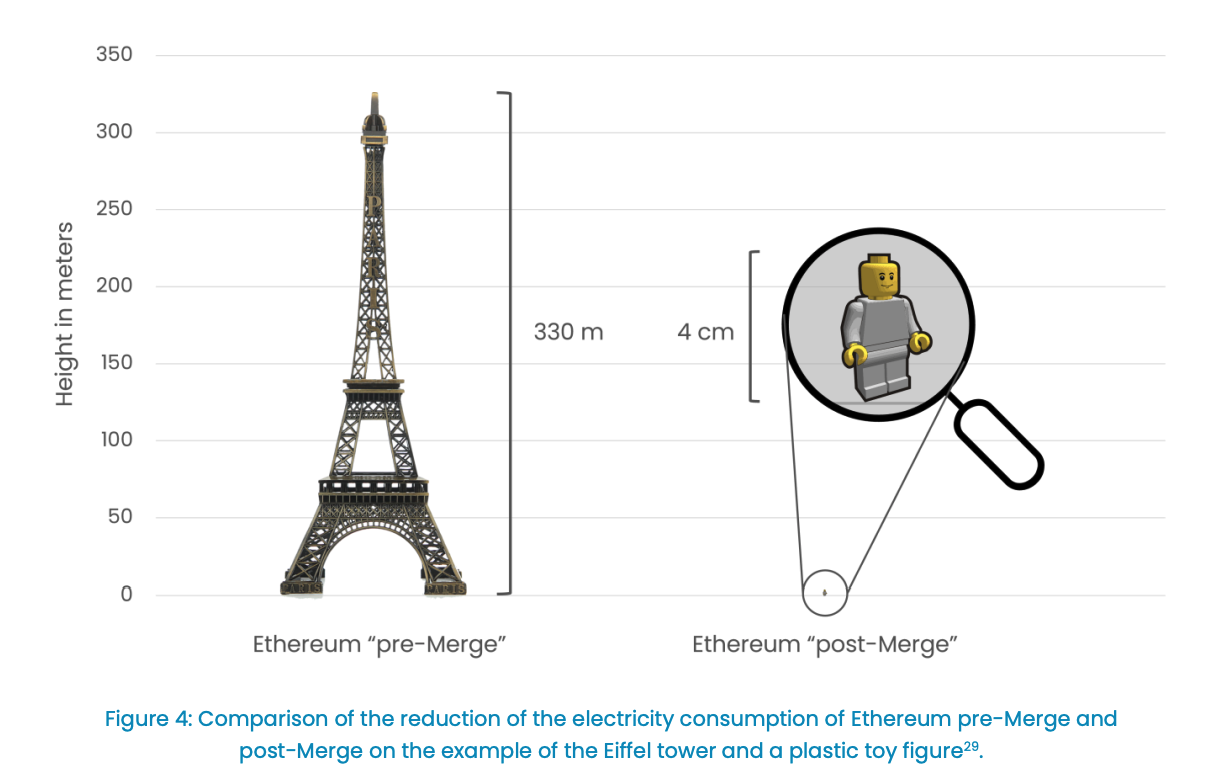

Source: Cambridge Bitcoin Energy Consumption Index https://cbeci.org/

Proof of work protocol: unsustainable amount of energy

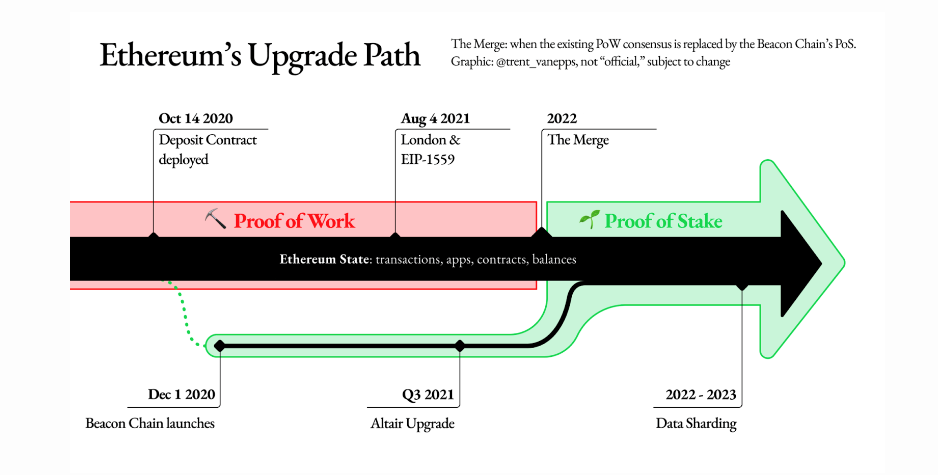

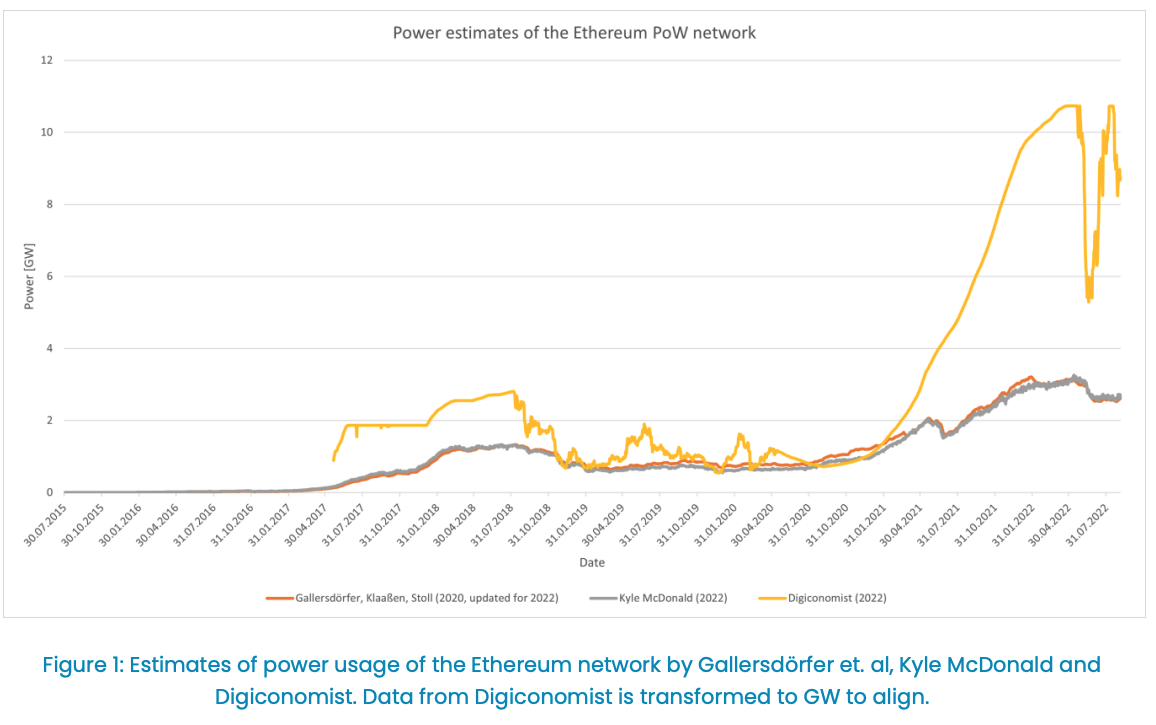

Ethereum power usage before the Sept 15, 2022 Merge

Why is this idea powerful?

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

A blockchain is a

What makes DeFi different from TradFi

decentralized finance =

provision of financial service functionality without the necessary involvement of a traditional financial intermediary like a bank or broker-dealer*

digital media =

provision of information service functionality without the necessary involvement of a traditional information intermediary like a publisher, library, or newagency

*my take: applies to only commoditizable services

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

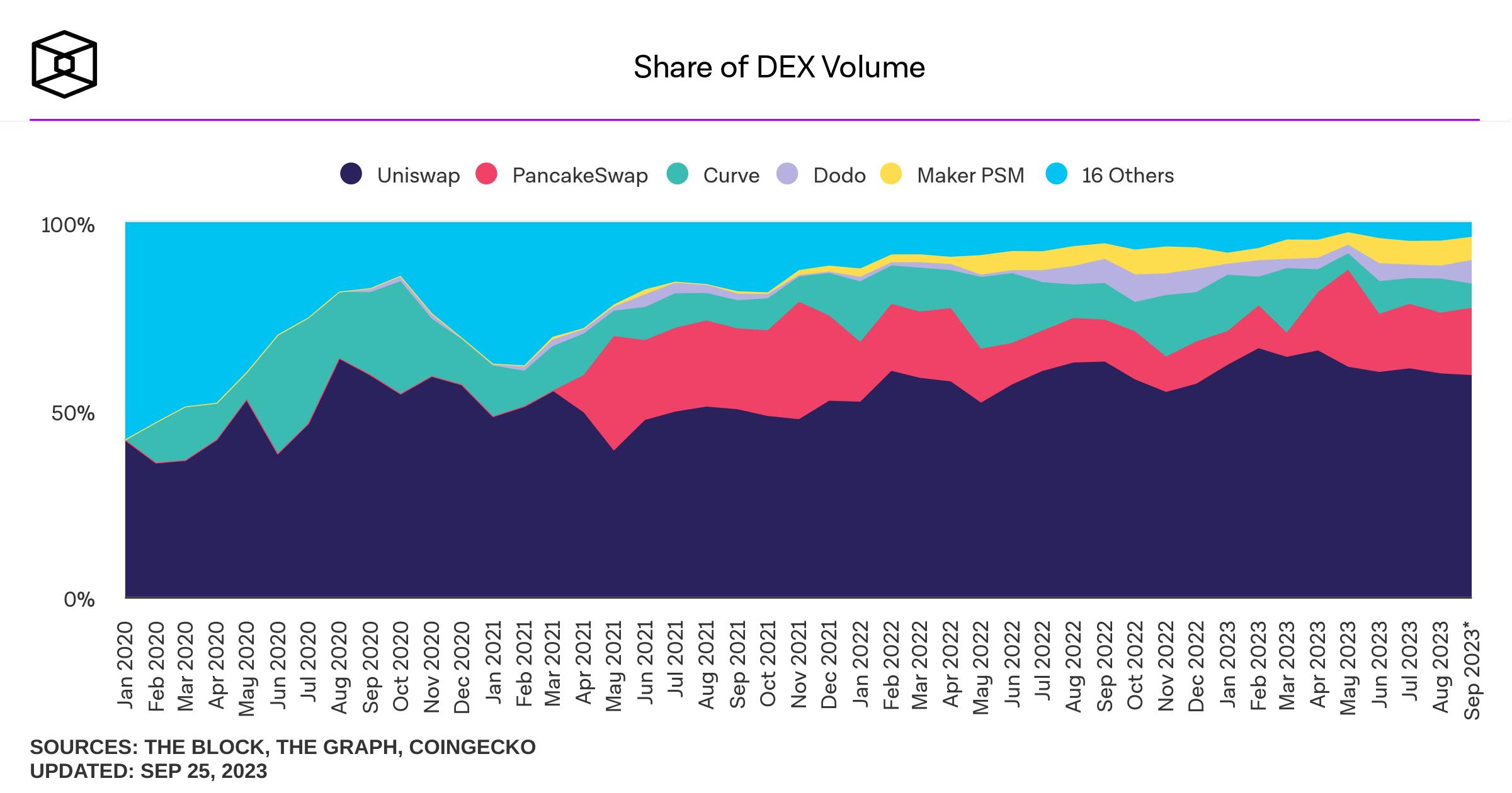

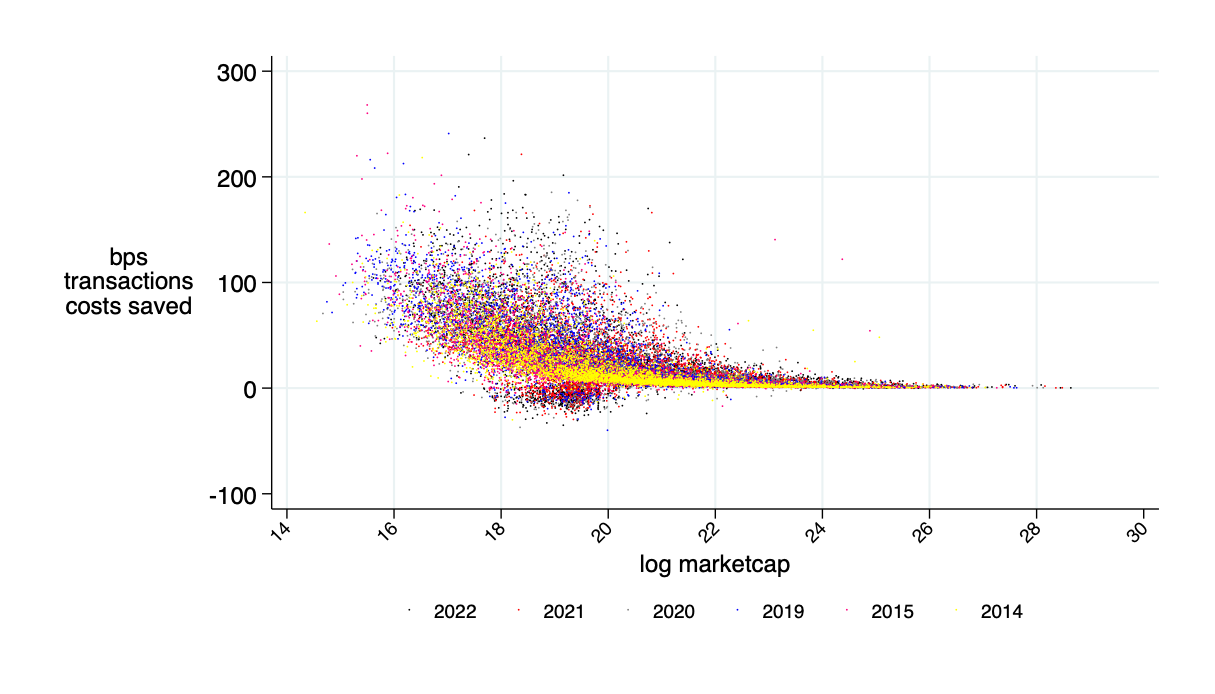

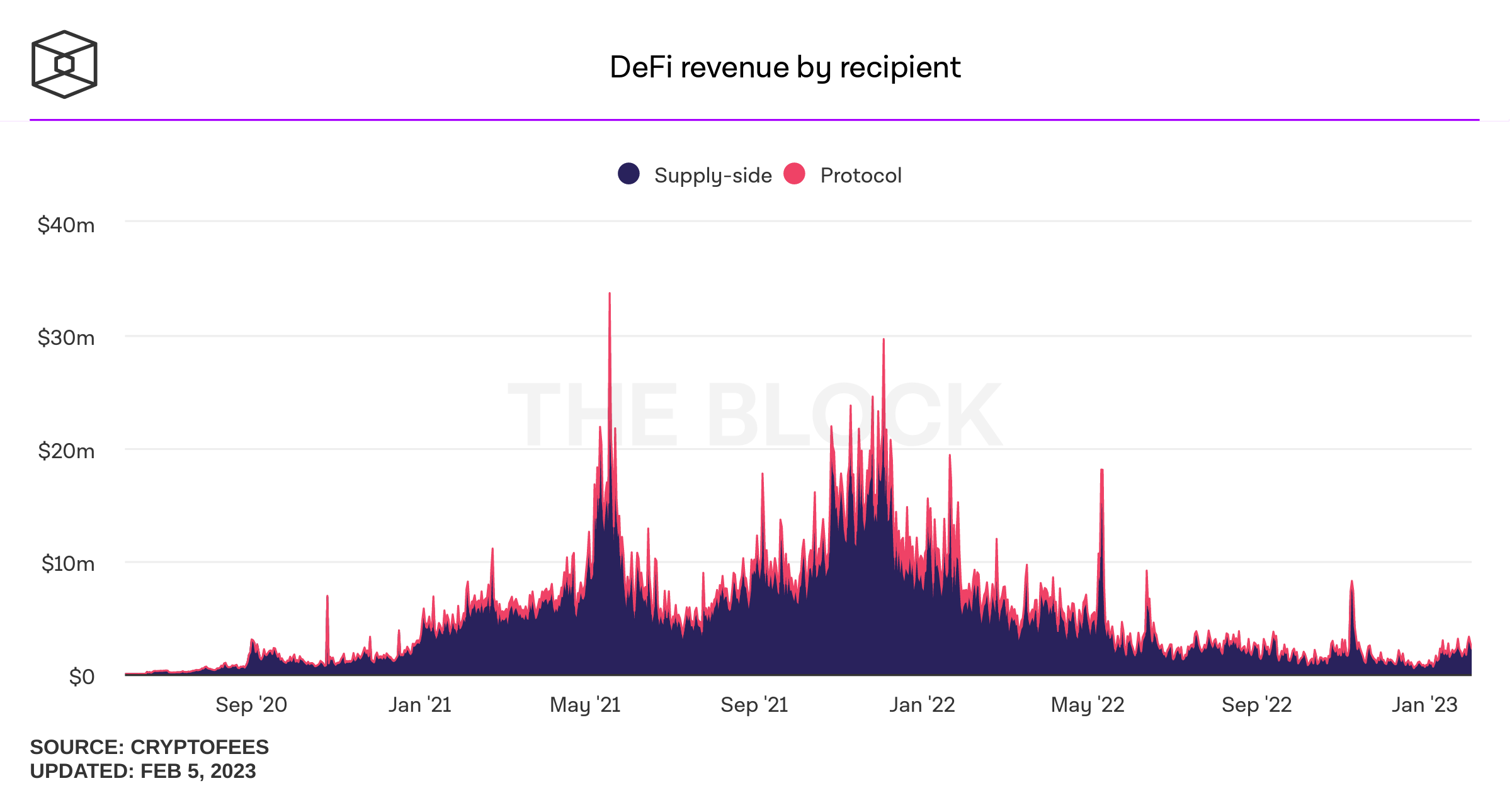

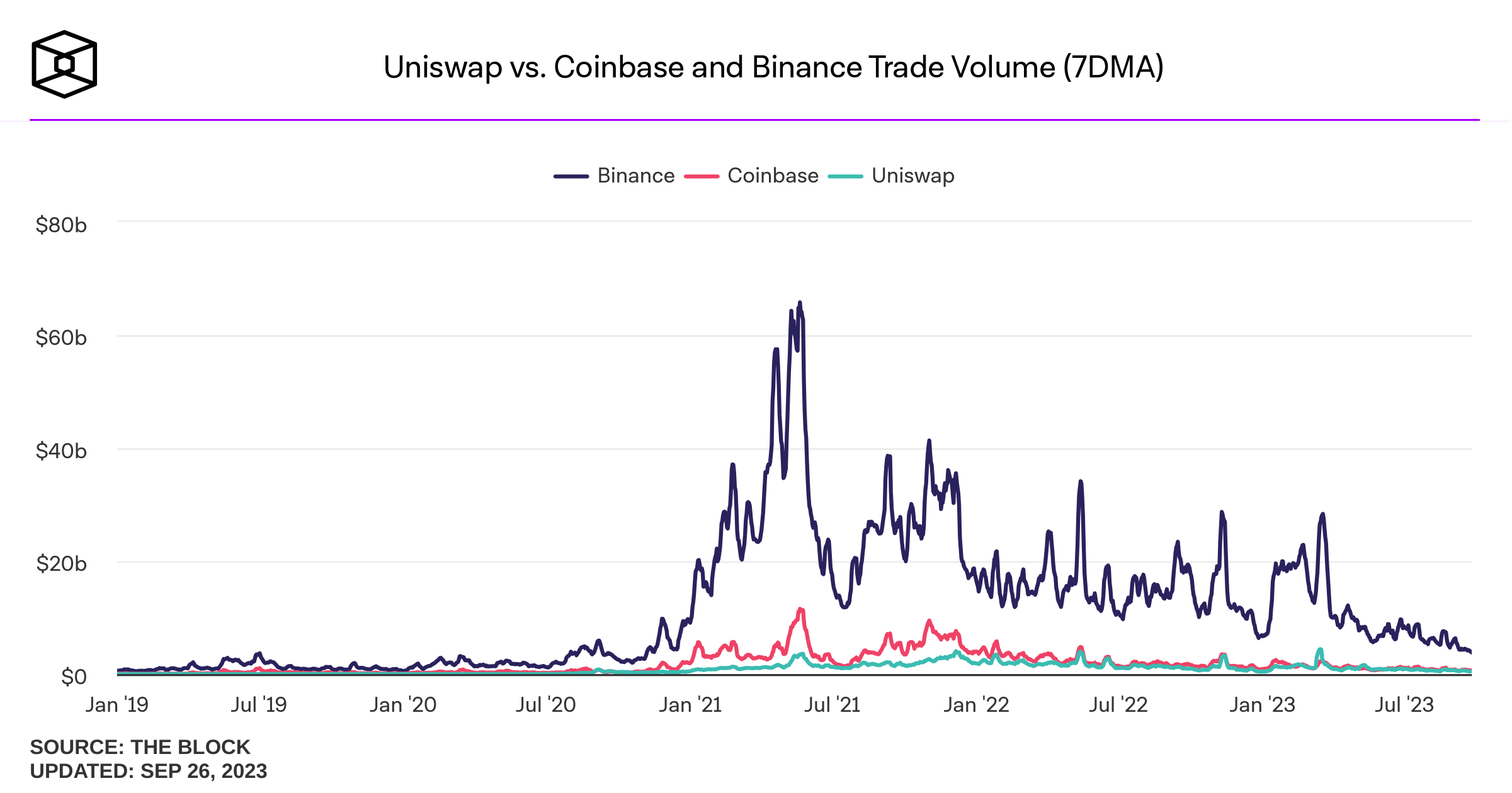

Sources of savings:

Possible transaction cost savings in cash equities: \(\approx\) 30%

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

UniSwap Lab supports development

a website app accesses the code

token holders control contact features

don't own the code

operation = decentral

control = decentral

anyone can use the baseline code

core code runs on the blockchain

tokens used as rewards

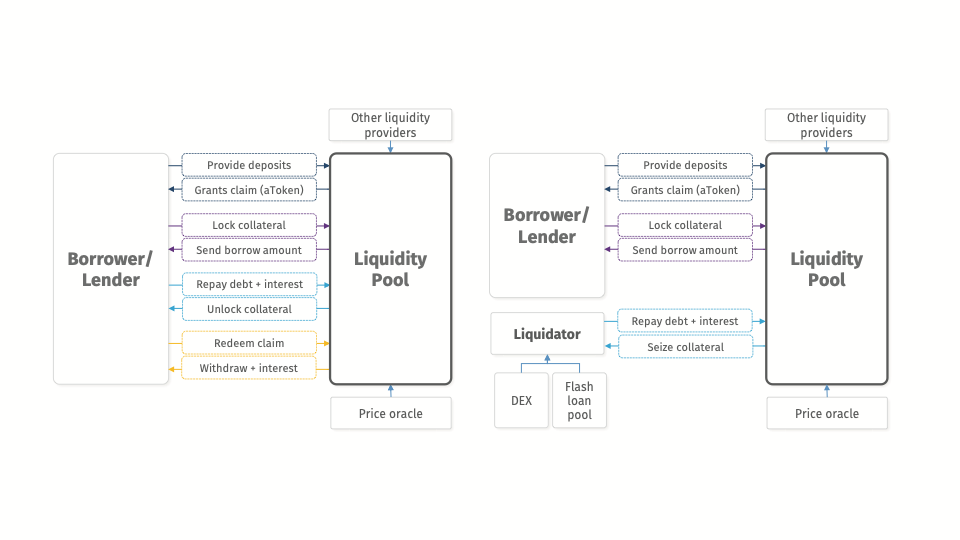

Application: Decentralized Borrowing & Lending

borrow

provide collateral

The Flow of Event: Normal Times

The Flow of Event: Collateral Liquidation

1. flash-borrow DAI

5. repay DAI

3. receive the collateral (ETH) at a discount

4. convert ETH to DAI

2. liquidate ETH-collaterilized loan with DAI

Loan liquidation opportunity

New tools: flash loan

Many automated DeFi products are emerging

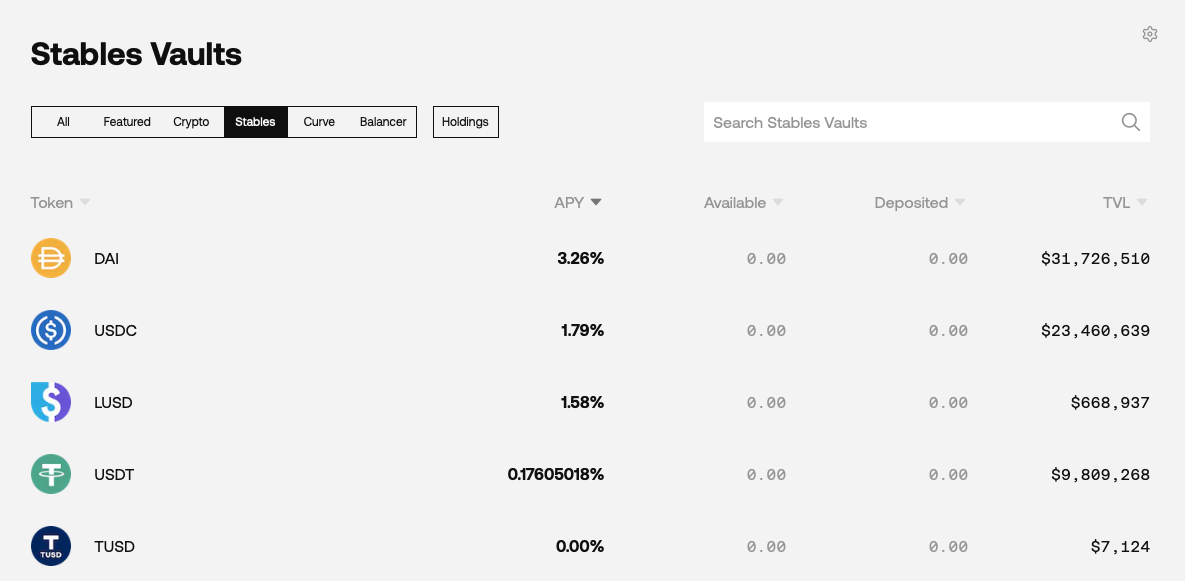

Obvious Smart Contract Application: Automate Investment Strategies

"yield aggregator:" push capital where rate of return is highest

Crypto Trading

Broker

Exchange

Internalizer

Wholeseller

Darkpool

Venue

Settlement

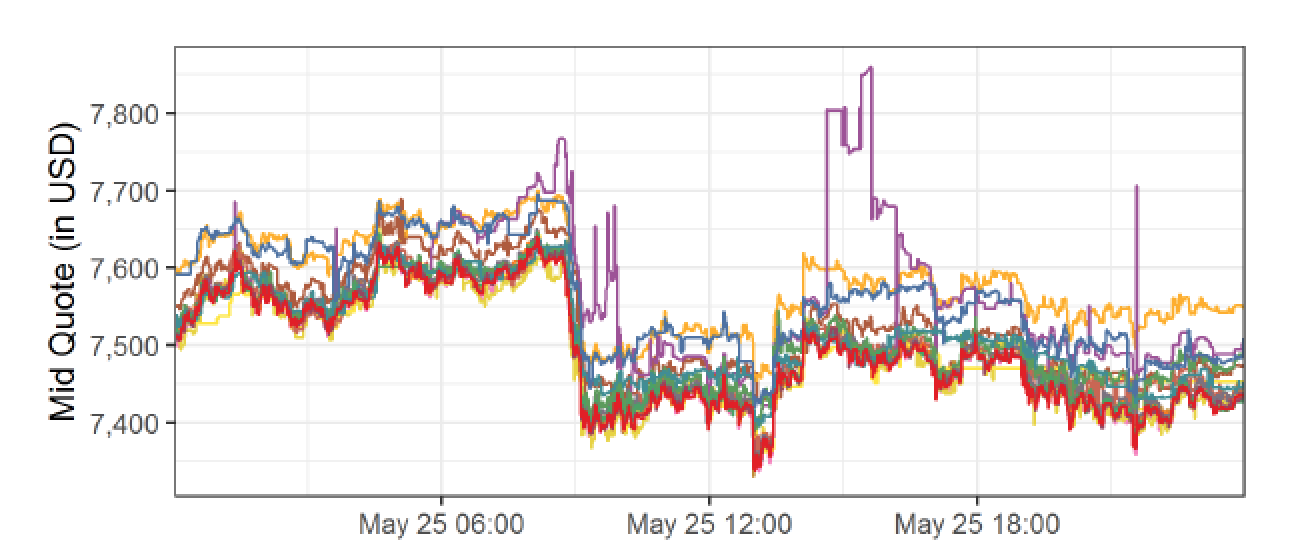

Centralized Trading

BTC/USD

ask: 7,600

bid: 7,550

BTC/USD

ask: 7,500

bid: 7,450

buy BTC

sell BTC

move BTC to Kraken

Crypto Wash Trading, Lin William Cong, Xi Li, Ke Tang, Yang Yang

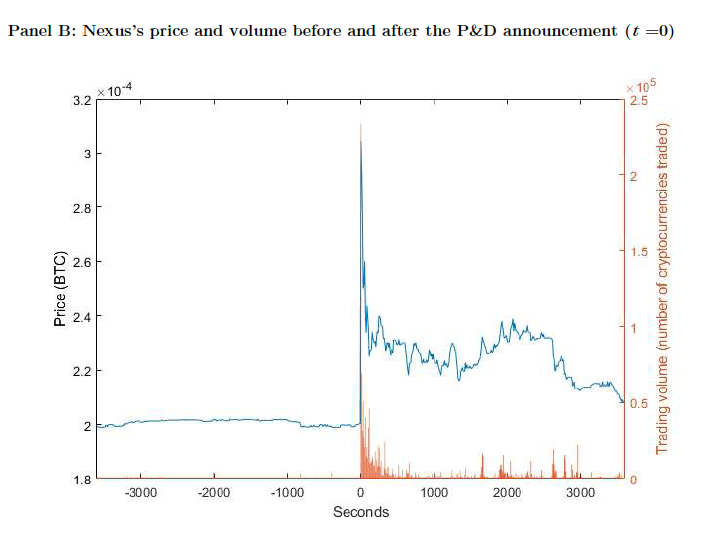

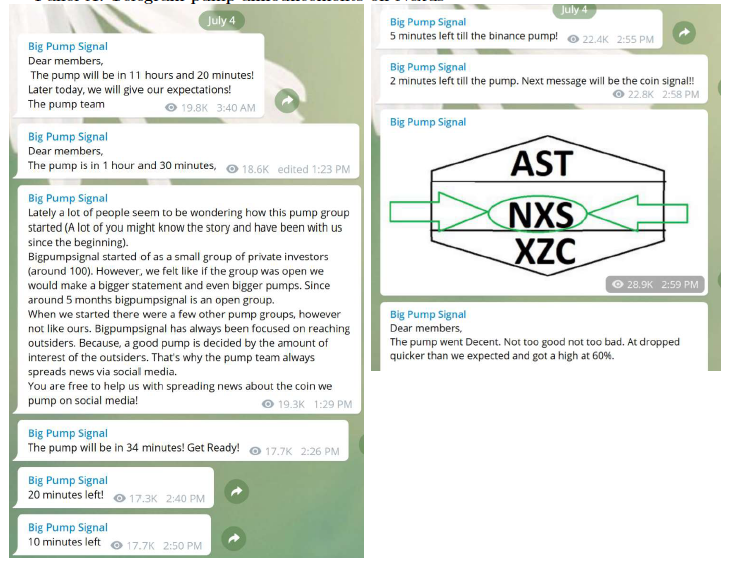

What is pump and dump?

arranged via Telegram Channels

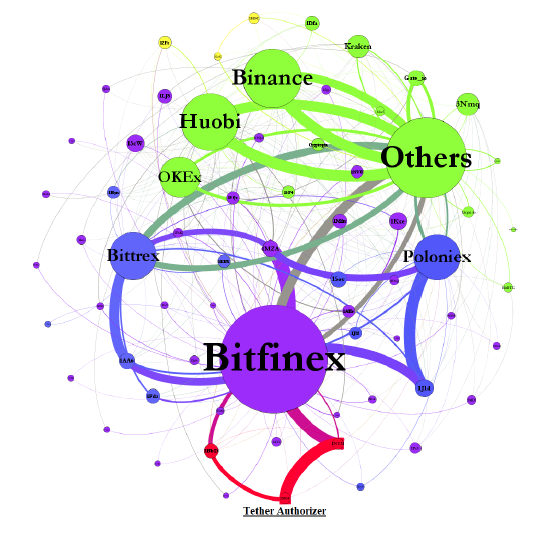

IS BITCOIN REALLY UN-TETHERED? JOHN M. GRIFFIN and AMIN SHAMS

Journal of Finance 2020

Figure 1. Aggregate Flow of Tether between Major Addresses

August 2016

Nov 8

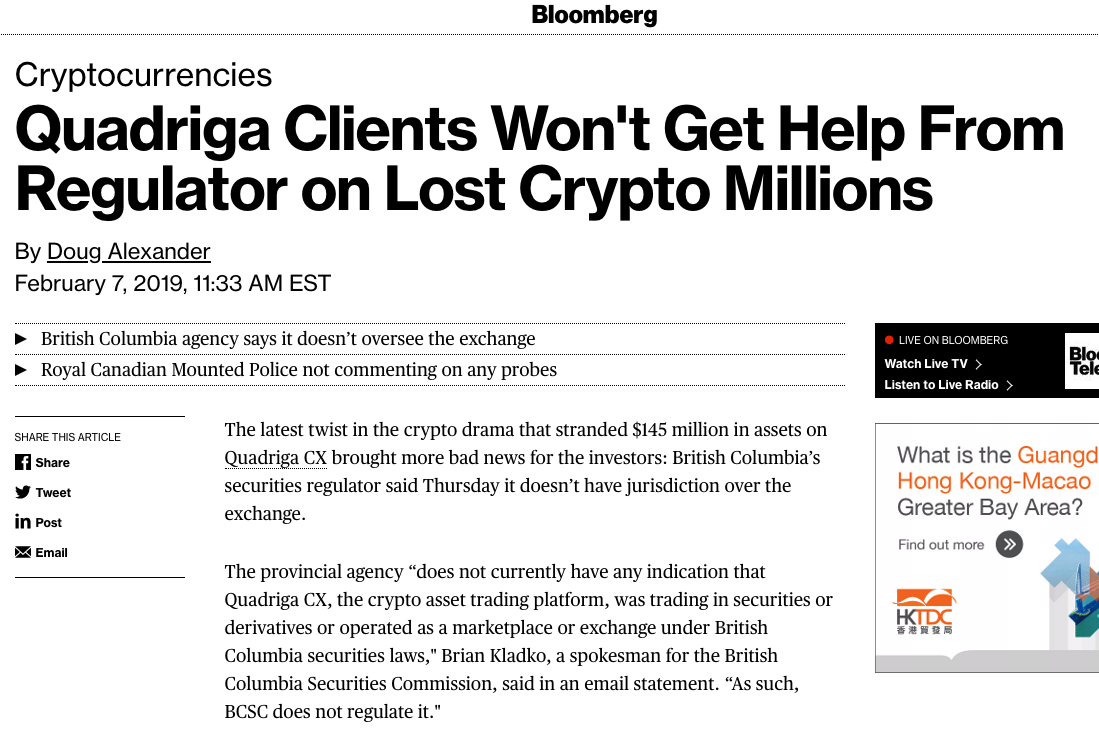

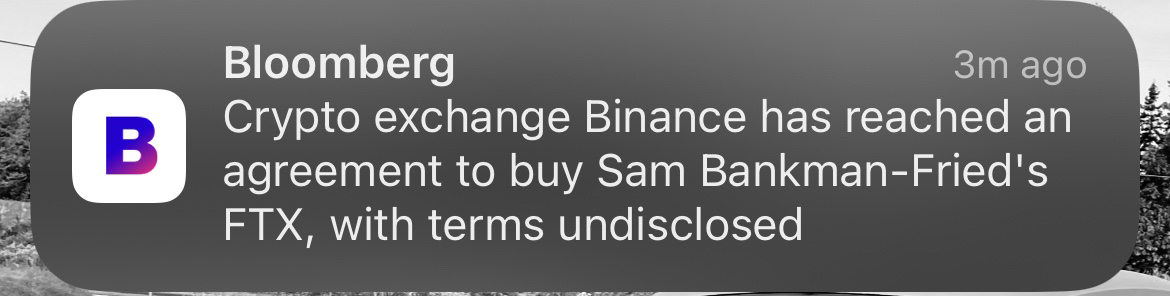

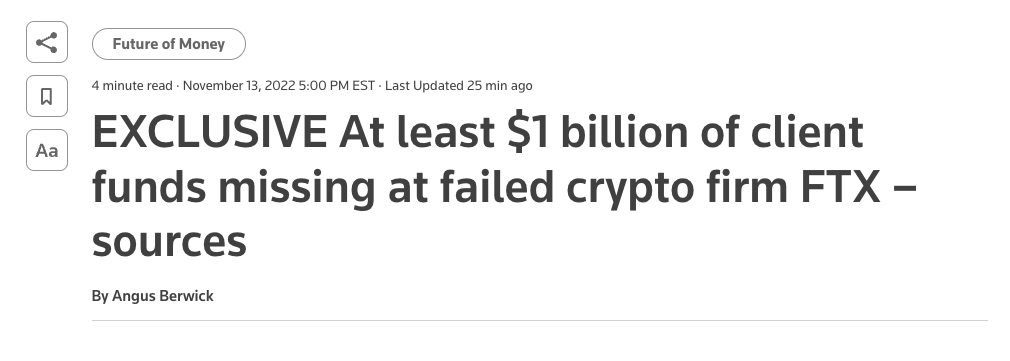

The FTX Implosion

Recurring Core problem

In a regulatory vaccum re: custody

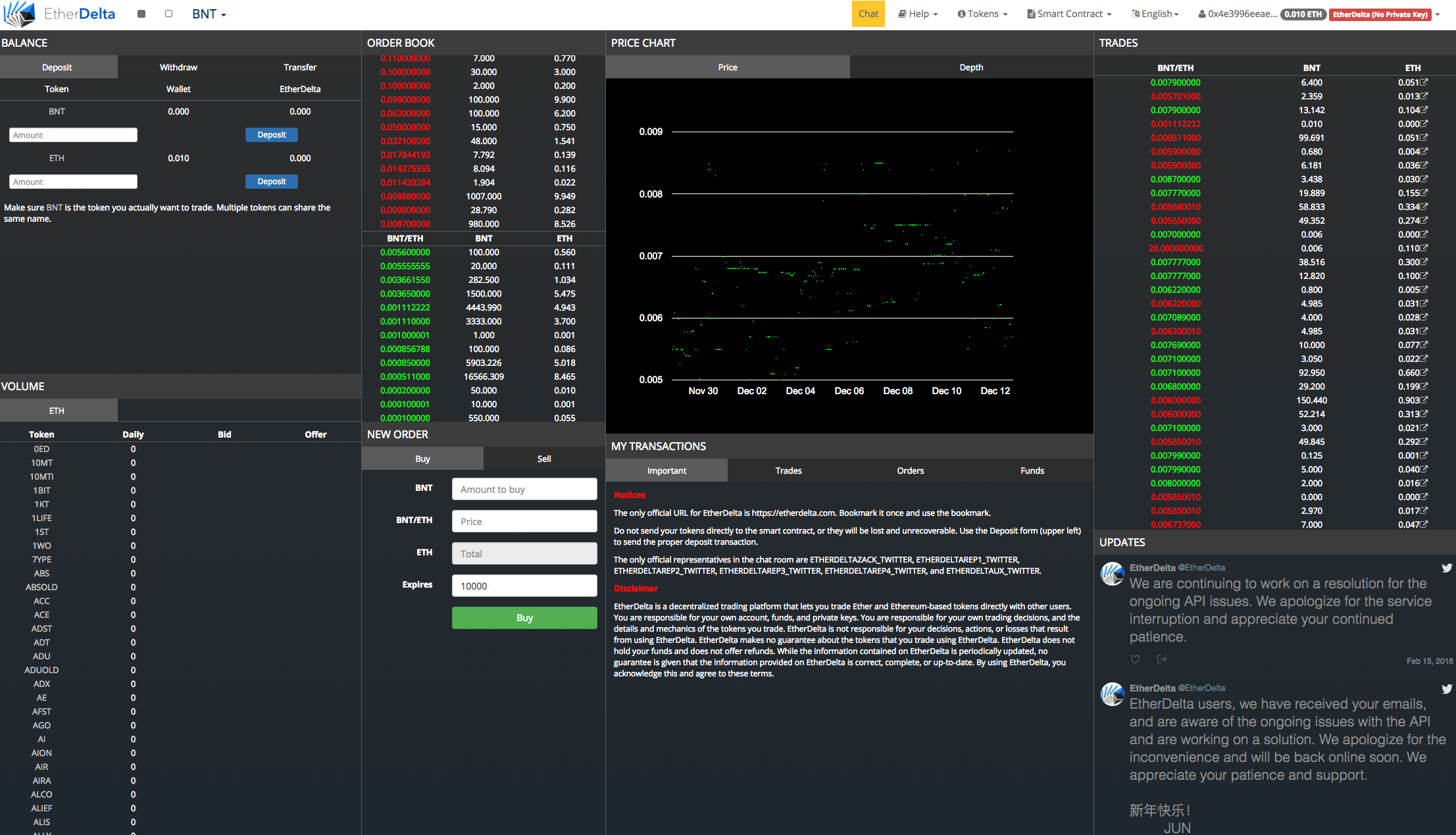

Decentralized Trading

Turns out ...

Decentralized Exchanges (DEX)

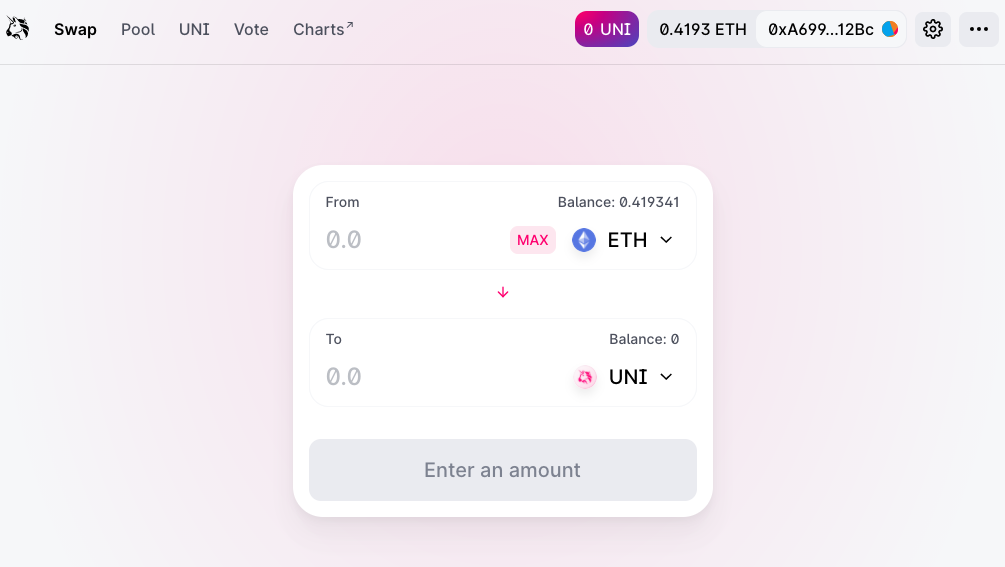

Idea:

\(\to\) simply connect with MetaMask (or similar wallet)

New institutions!

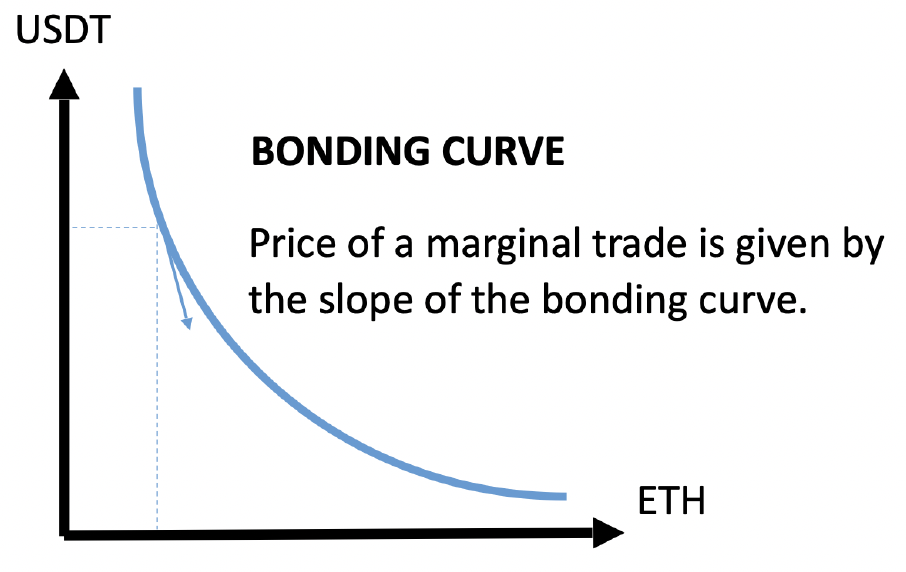

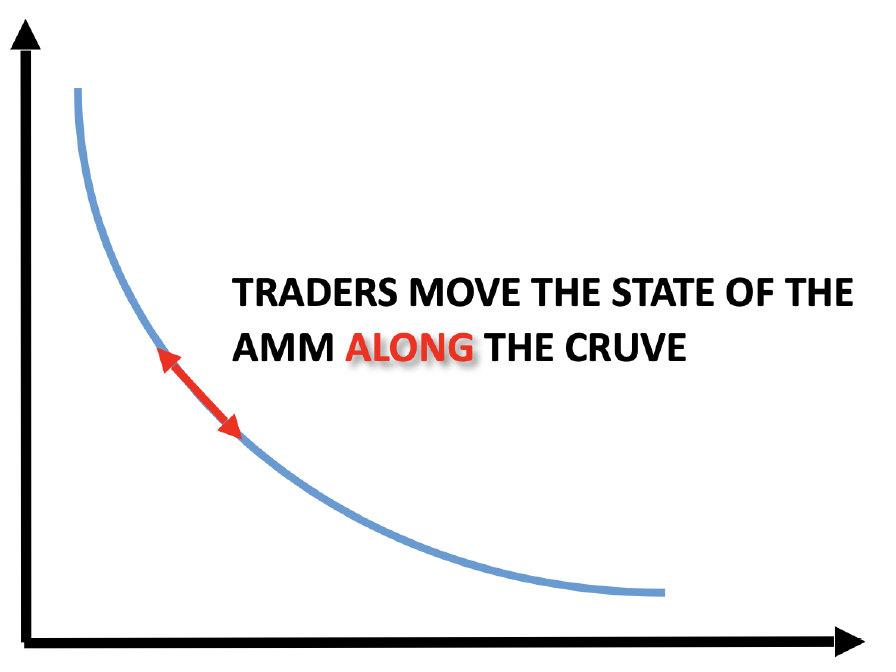

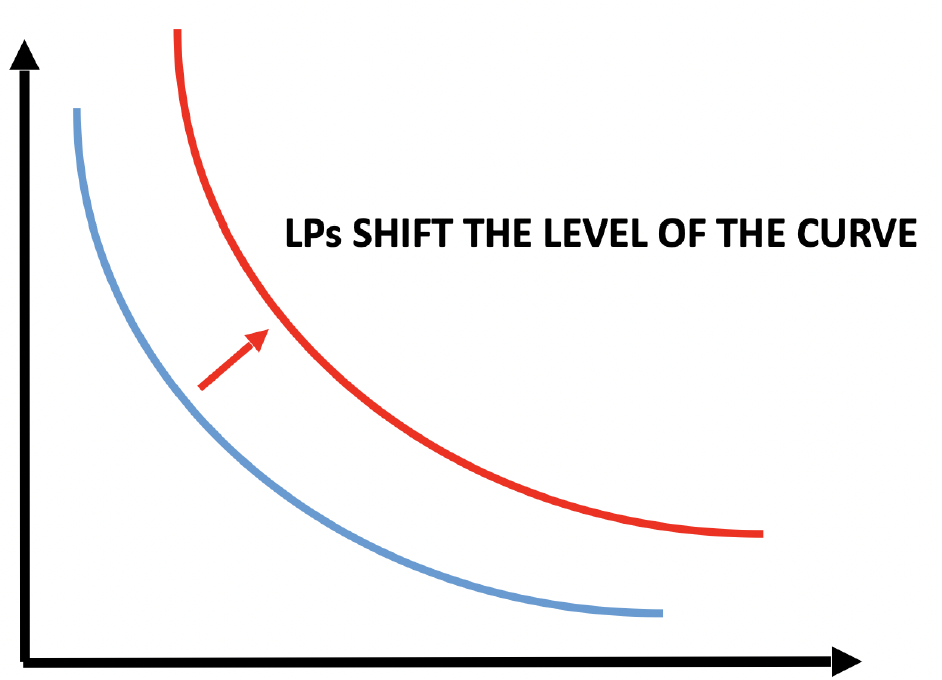

AMM Pricing

Key Components

\(X-Q\)

\(X\)

\(Y+P(Q))\)

\(Y\)

\(c=X\cdot Y\)

Price mechanism:

Prices

invariant \(k=4\times4=16\)

Instantaneous exchange rate:

1 = 1

Contract deposit:

sell 4 DAI for how many USDC?

1

0.5

=

invariant \(k=100\times100=10,000\)

Contract deposit:

Problem: large "slippage" (or price impact)

"Deep liquidity" helps minimize this.

\(100\times\)

\(100\times\)

sell 4 DAI for how many USDC?

\(100\times\)

\(100\times\)

\(3.85\times\)

\(-3.85\times\)

1

0.9625

=

\(\to\) the more money is in the contracts, the lower the price impact

front-running

transactions enter mem-pool

\(\to\) all visible there

arbitrageur make instant-swap trade at higher gas price

\(\to\) trade instead of original trade

"fix" (not a proper solution): set a max slippage (a range of prices that willing to trade at)

Uniswap V3

Stopped here in lecture 3

DEX: Quick Recap

Liquidity providers

Liquidity demander

Liquidity Pool

AMM pricing is mechanical:

USDC

Quiz: Quick Recap

Consider a DEX (decentralized exchange) that prices securities according to the constant product rule discussed in lecture. The initial deposits in the liquidity pool are 200 ETH and 300,000 USDC. You want to buy ETH.

Note: buy ETH = sell USDC

After you buy 1 ETH in exchange for y USDC, the pool will have

\(\Rightarrow 200 \times 300,000= (300,000 + y) \times (200-1) \)

\(\to y = 1,508\)

Quiz: Quick Recap

After you buy 10 ETH and sell y USDC, the pool will have

\(\Rightarrow 200 \times 300,000= (300,000 + y) \times (200-10) \)

\(\to y = 15,789\) -- cost of 10 ETH!

\(\to 1,578.9\) per 1 ETH

front-running

transactions enter mem-pool

\(\to\) all visible there

arbitrageur make instant-swap trade at higher gas price

\(\to\) trade instead of original trade

"fix" (not a proper solution): set a max slippage (a range of prices that willing to trade at)

Uniswap V3

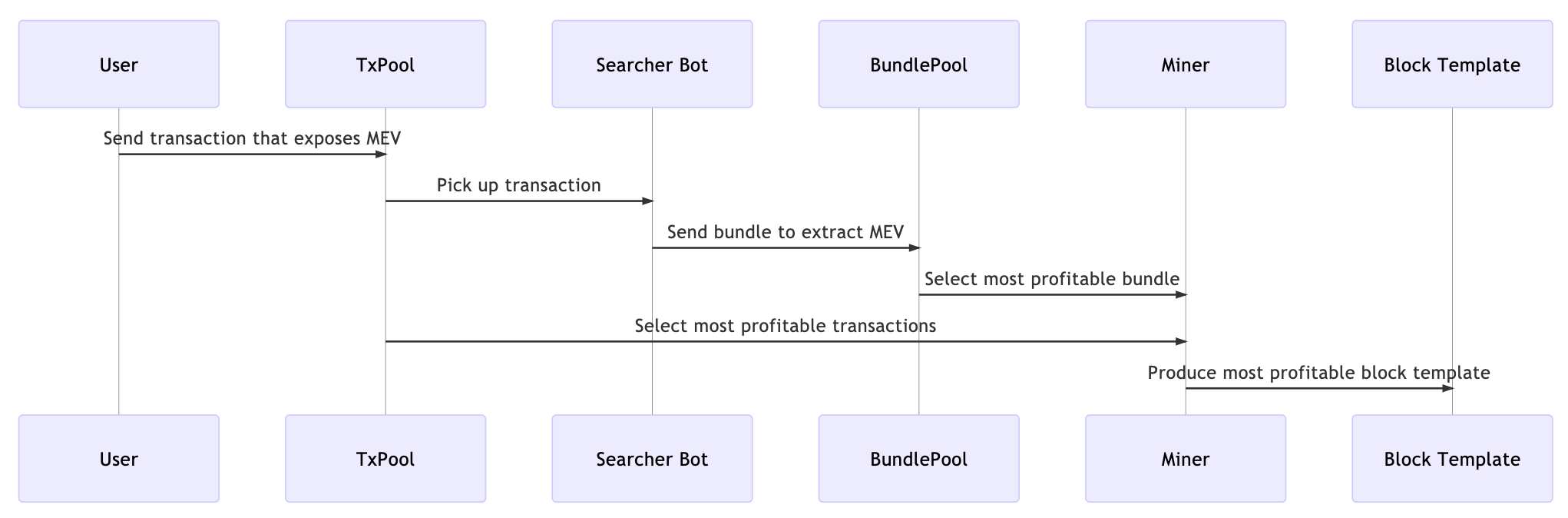

Transaction Processing in DeFi

Transaction Visualization

transactions

decentralized applications

tokens

The

"Mem-Pool"

a

b

c

d

e

f

g

A Simple Overview

a

b

c

d

e

f

g

The reality is more complicated

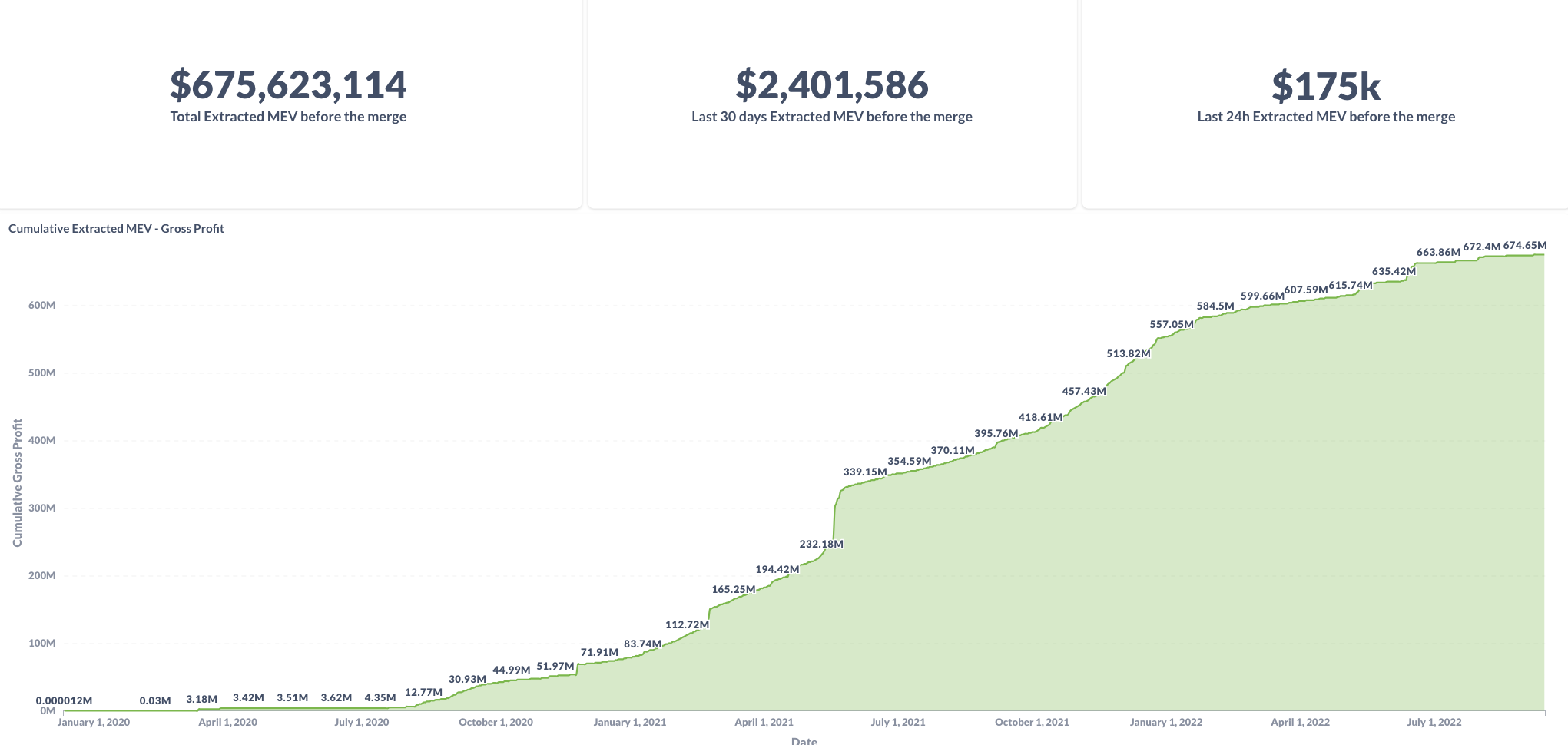

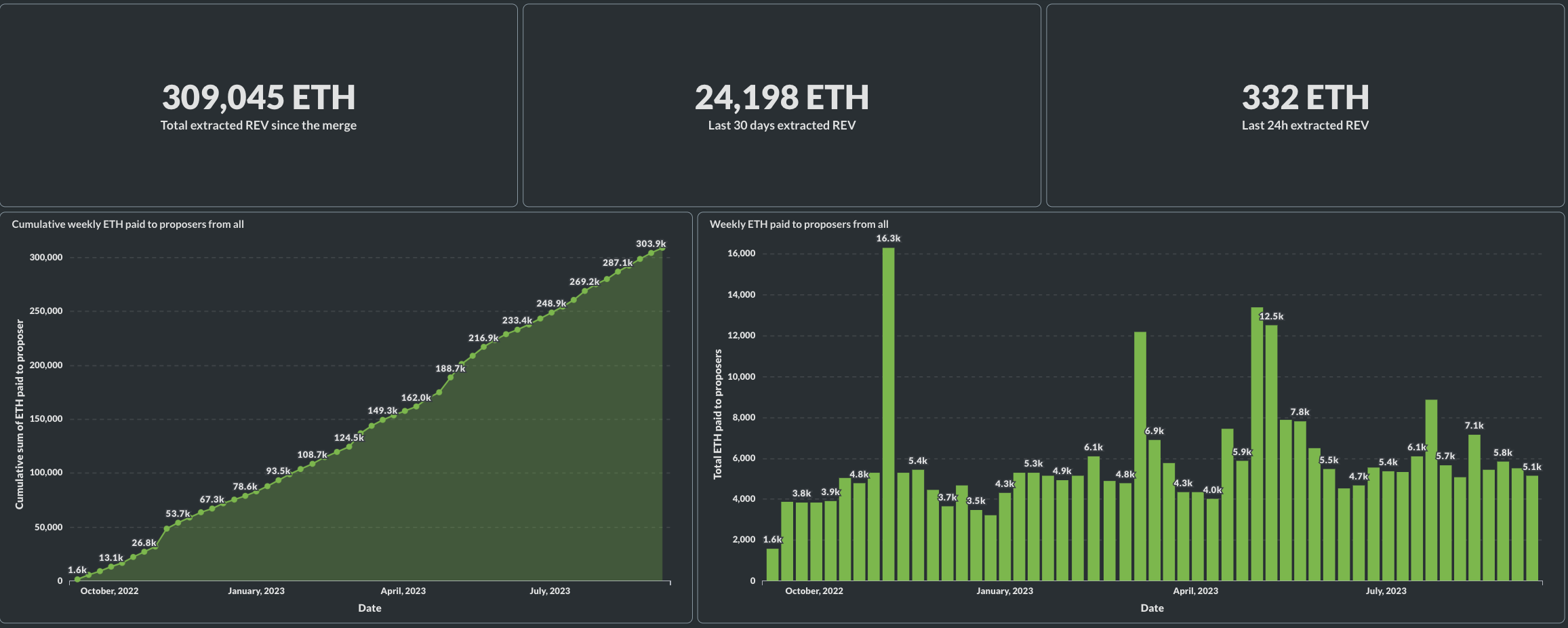

Consequence 1: Extract Value from Users

"Ethereum is a Dark Forest"

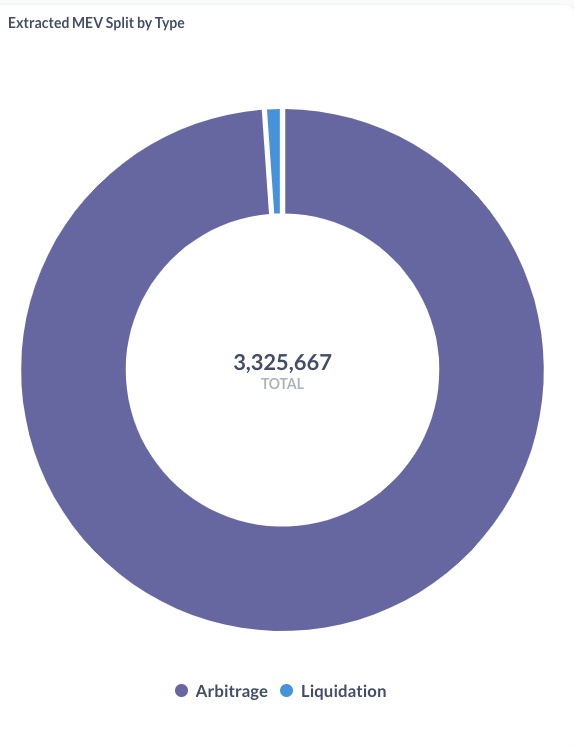

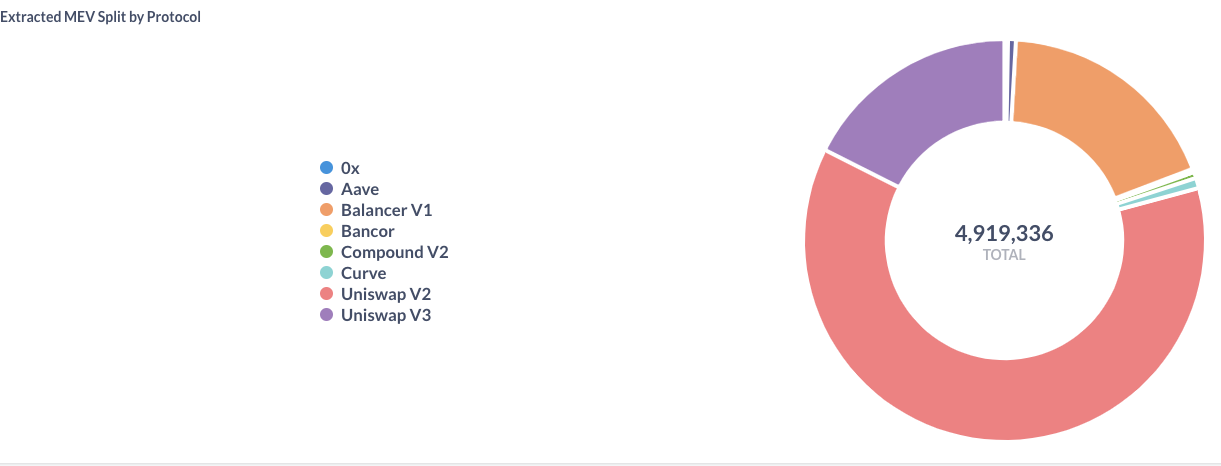

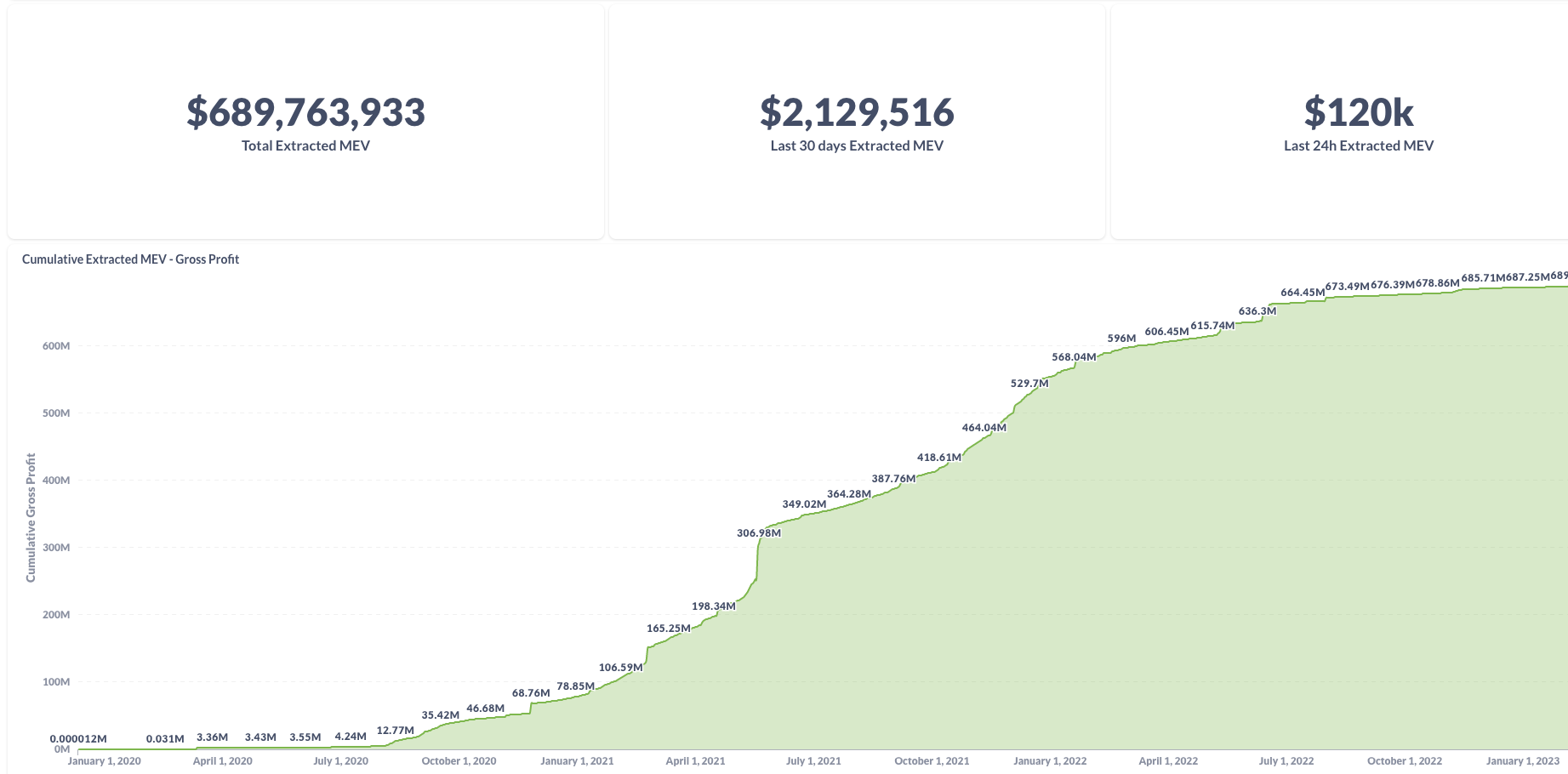

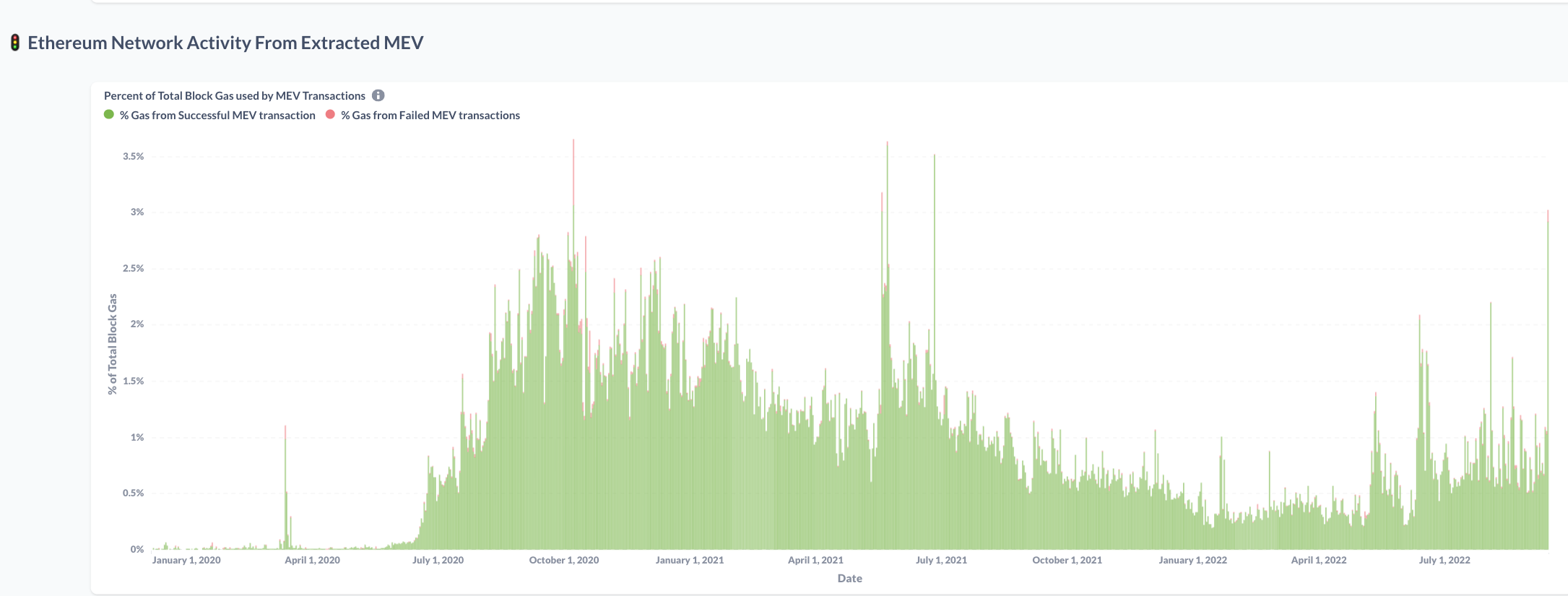

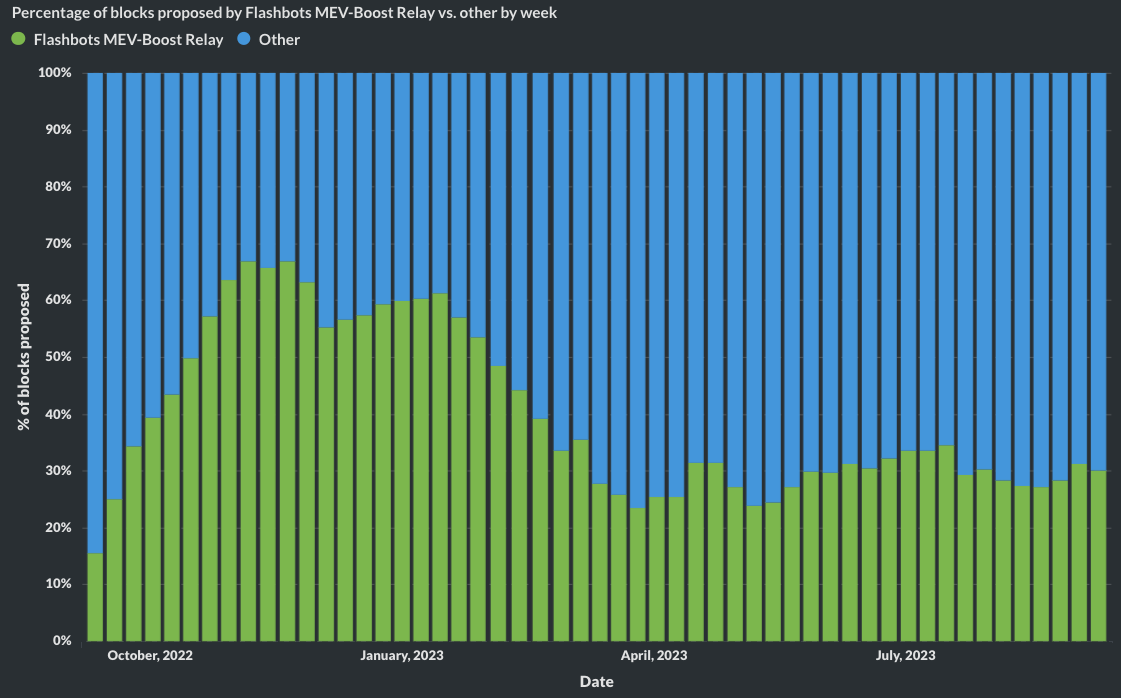

The charts are for pre-merge, see https://transparency.flashbots.net for post-merge stats

Consequence 2: Excess Gas Prices ("Priority Gas Auctions")

One resolution:

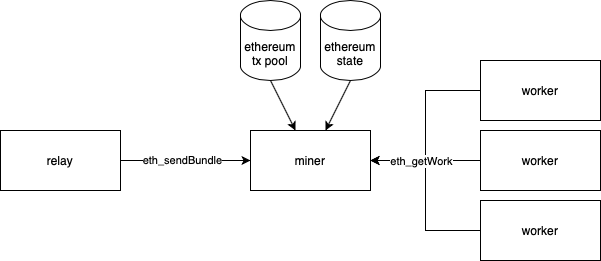

Flashbots Protocol

Idea of Flashbots

Flashbots does not prevent MEV!

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

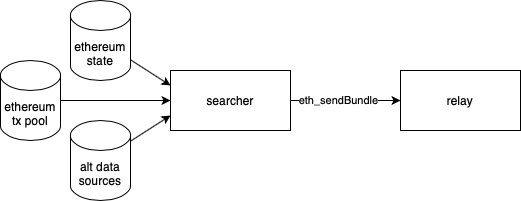

Illustration

Transactions Send to Searchers

NB: the relay is a security measure: it has high capacity and can distinguish garbage from real transactions

Bundles come to Miners

NB: miners could still manipulate, front-run etc, but Flashbots monitors them and would cut them off if they misbehave

Is it used?

81% of validators have signed on with Flashbots (>880,000 total)

Does Flashbots Prevent MEV? No!

Does Flashbots Prevent MEV?

Flashbot 3.0 Transaction Privacy

By Katya Malinova

This is an intro to DeFi and Trading for F741 in the Fall of 2023.