Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Instructor: Katya Malinova

This slide deck was developed in collaboration with Andreas Park (University of Toronto)

Finance

+

Technology

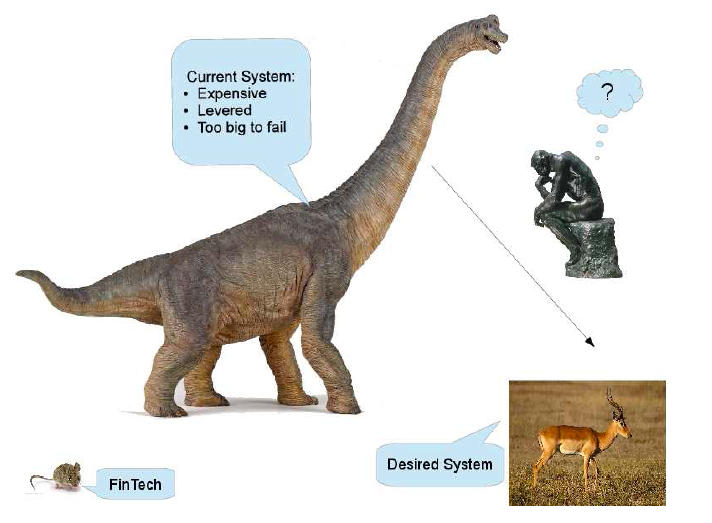

usually post 2008

outside of traditional financial institutions

goal: disrupt existing FIs

this is really squishy ...

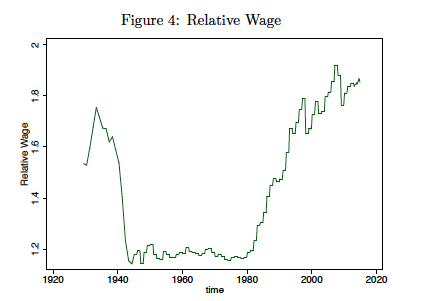

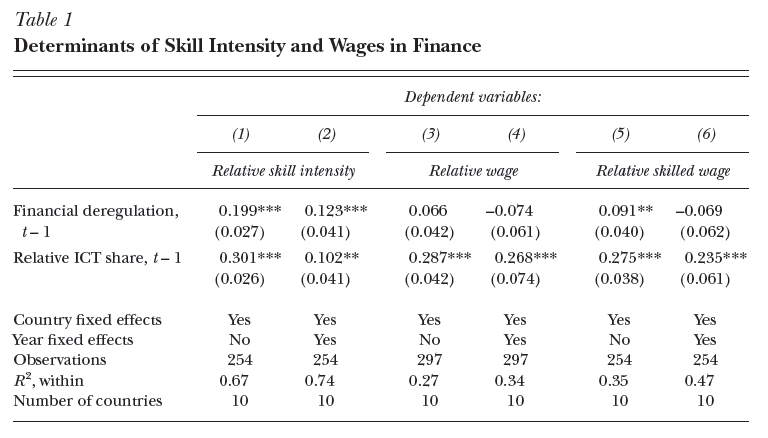

relative wage=avg wage in finance/avg rest of economy

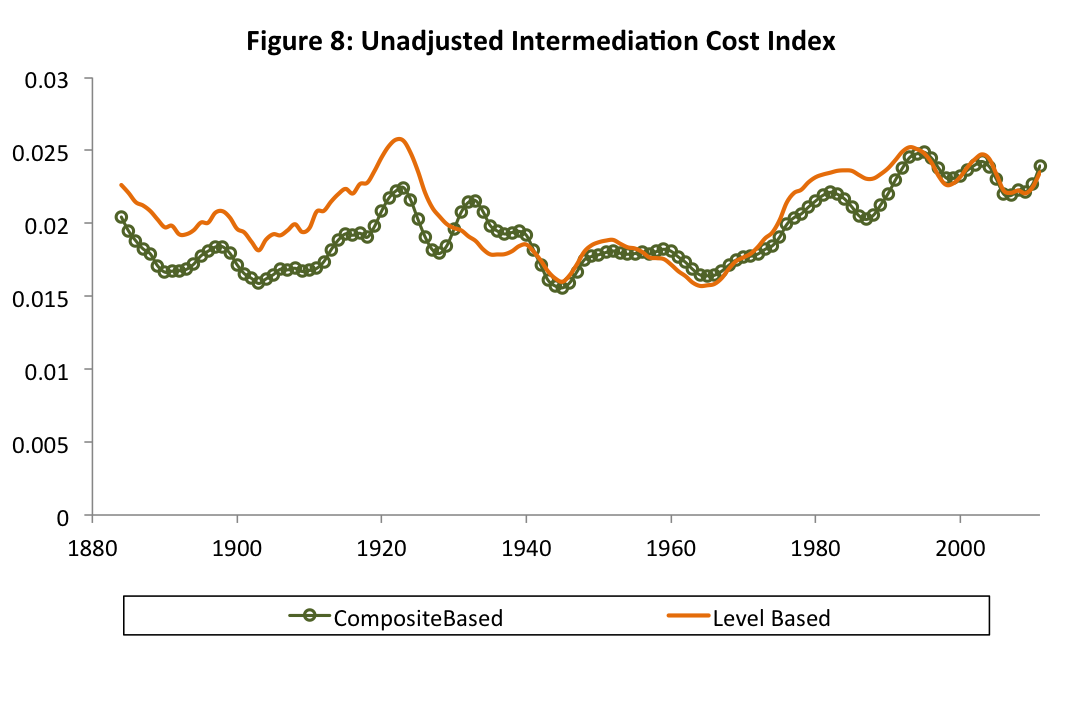

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

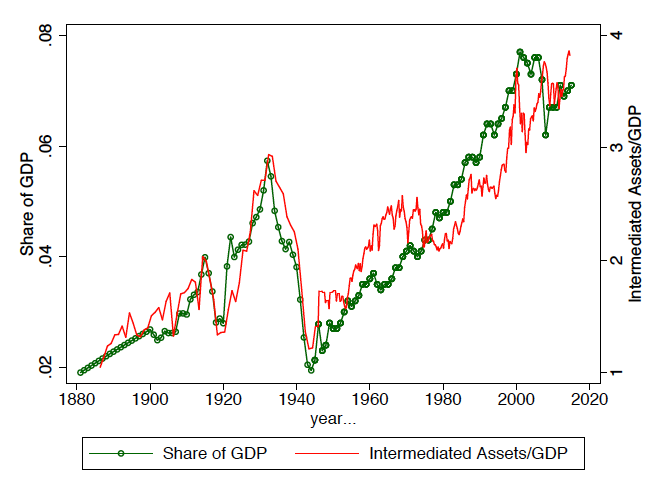

Ratio of the income of financial intermediaries to the quantity of intermediated assets

Source: Philippon & Reshef (JEP 2013)

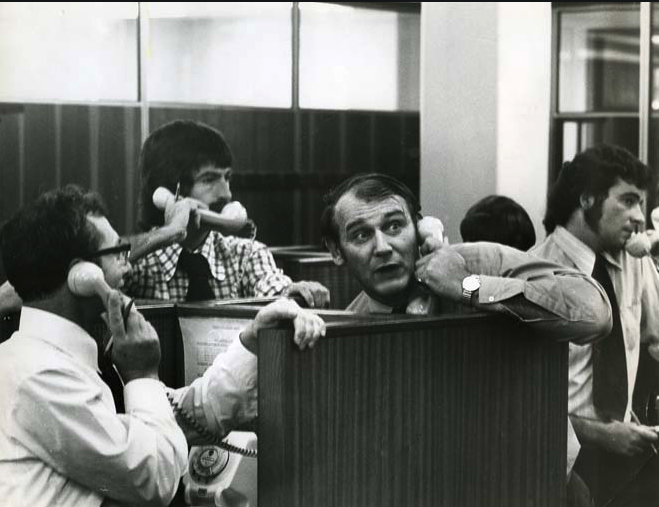

Example: One of the first segments that were disrupted from the outside: equity trading

Source: Bloomberg News, Feb 20, 2015

Note: The biggest disruptors (the HFTs) came from the outside of the traditional system (kinda).

entire career streams disappear

MIT Technology Review, Feb 07, 2017

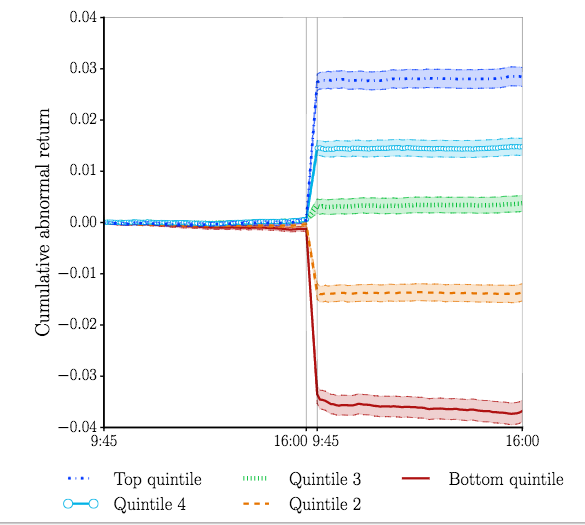

Markets get better: the post earnings announcement drift had been a long-standing puzzle in finance. ... It's gone.

Source: Martineau (UofT) (WP2017)

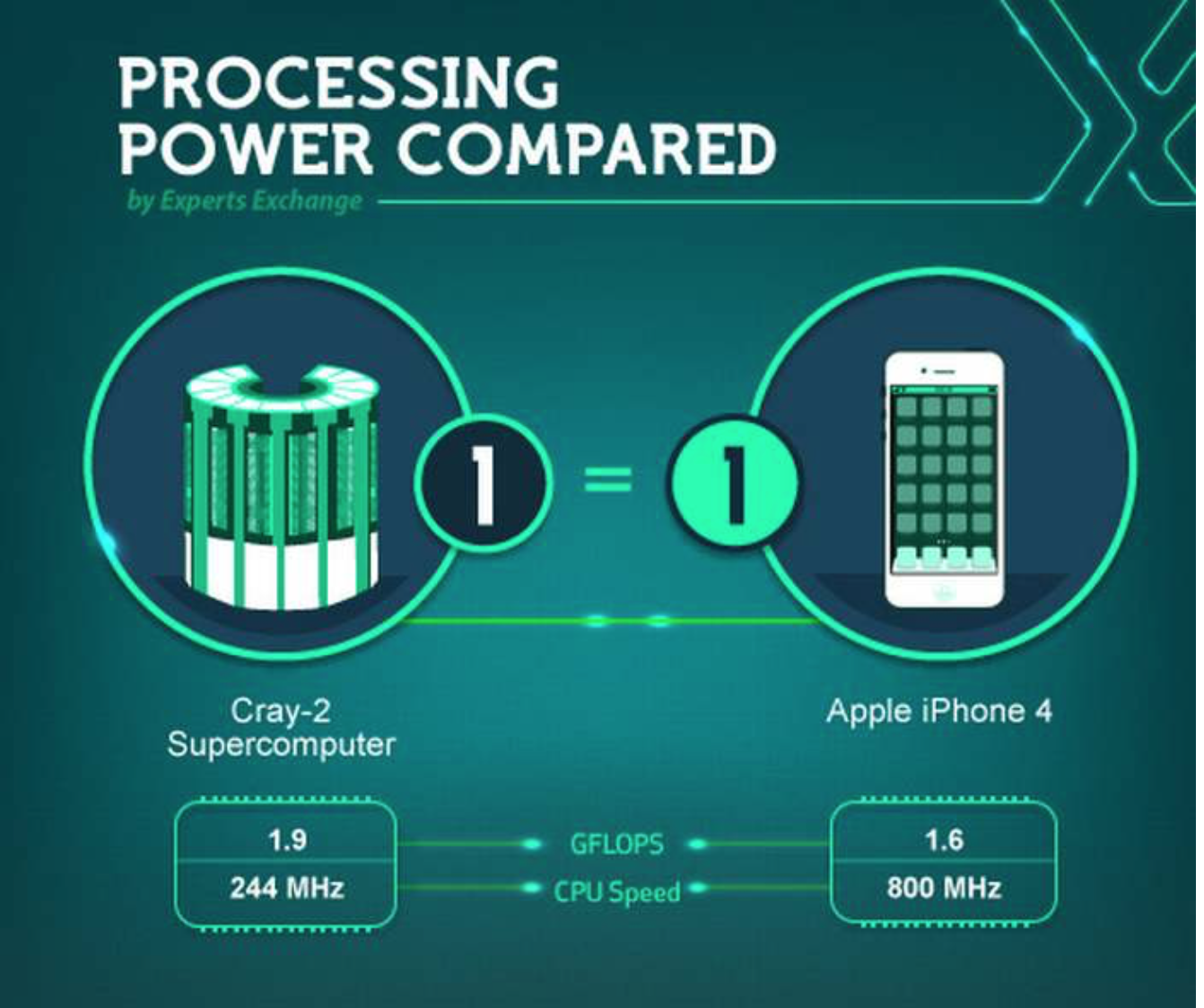

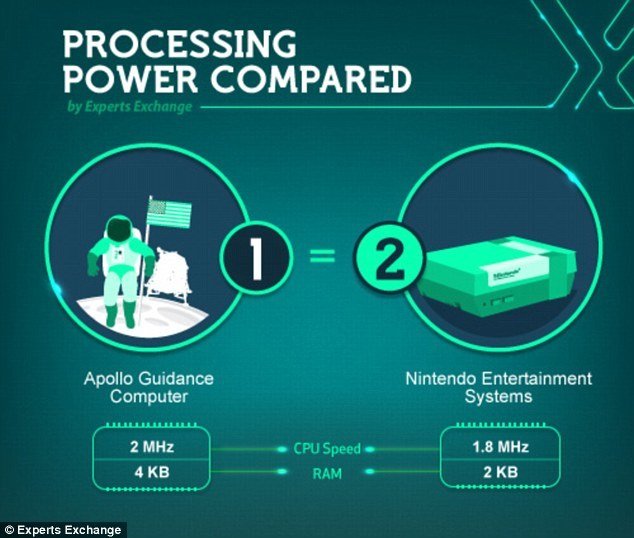

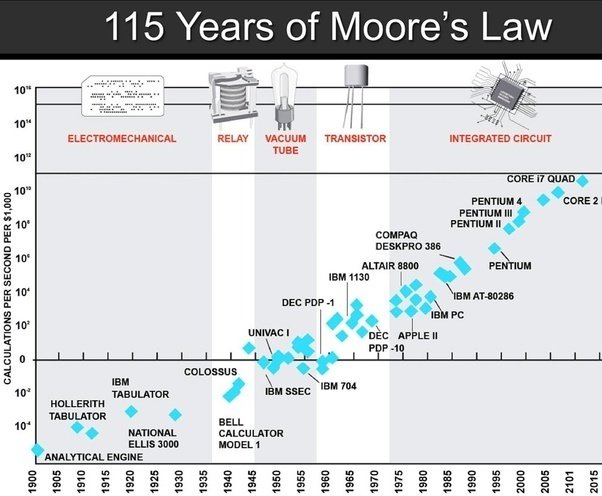

Fastest Computer in 1985!

"the number of transistors per square inch on integrated circuits had doubled every year since their invention."

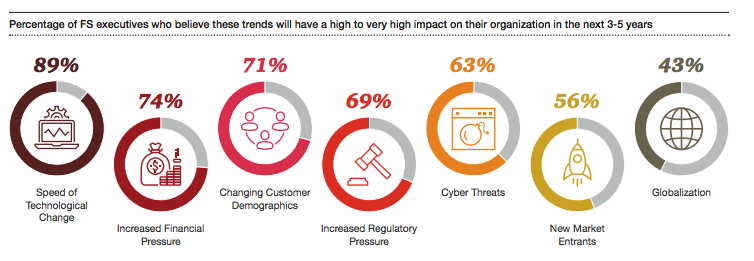

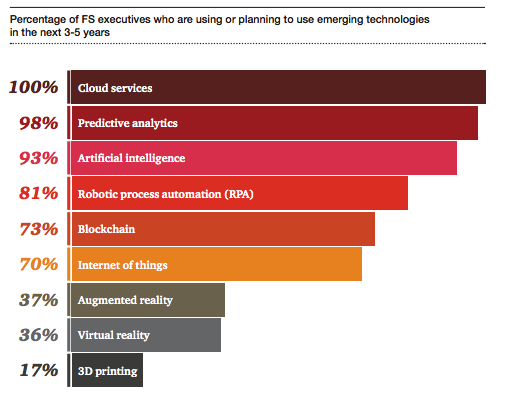

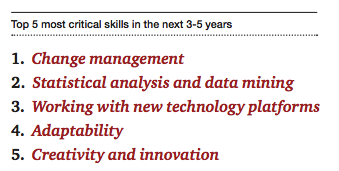

Source: "Unlocking the human opportunity: Future-proof skills to move financial services forward"; PwC report for the Toronto Financial Services Alliance, April 2018

Key features

Approach: Propositions that are

based on EY 2017 FinTech report

Impact on incumbents: struggle to deliver the seamless and personalized user experience.

Consequence: ripple effect

based on EY 2017 FinTech report

Problem for incumbents

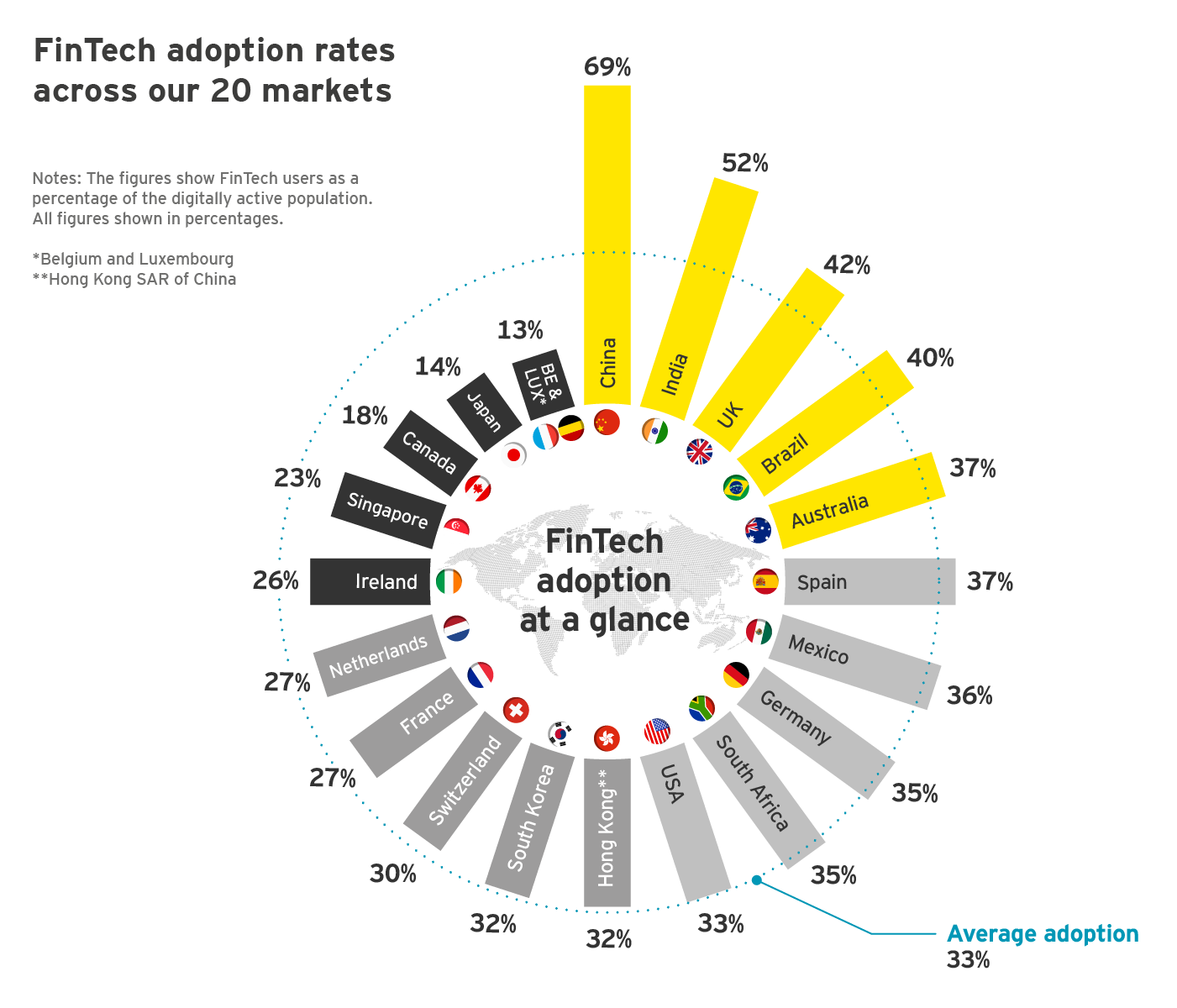

Source: EY FinTech Adoption Index 2017

18%

Source: Philippon (2017)

Clayton Christensen: customers don’t buy products; instead, they hire a solution to help them complete a specific job at a specific time.

https://youtu.be/sfGtw2C95Ms

4. Big Tech Firms

3. Those that work to replace or change the financial system as we know it.

Lending and Borrowing

Wealth Management

Payments

Investment Banking Services

Payments

5% to cab firm and 10-day delay

International remittances: $600B (U.S.) p.a.

all in: 10% fees

Payments

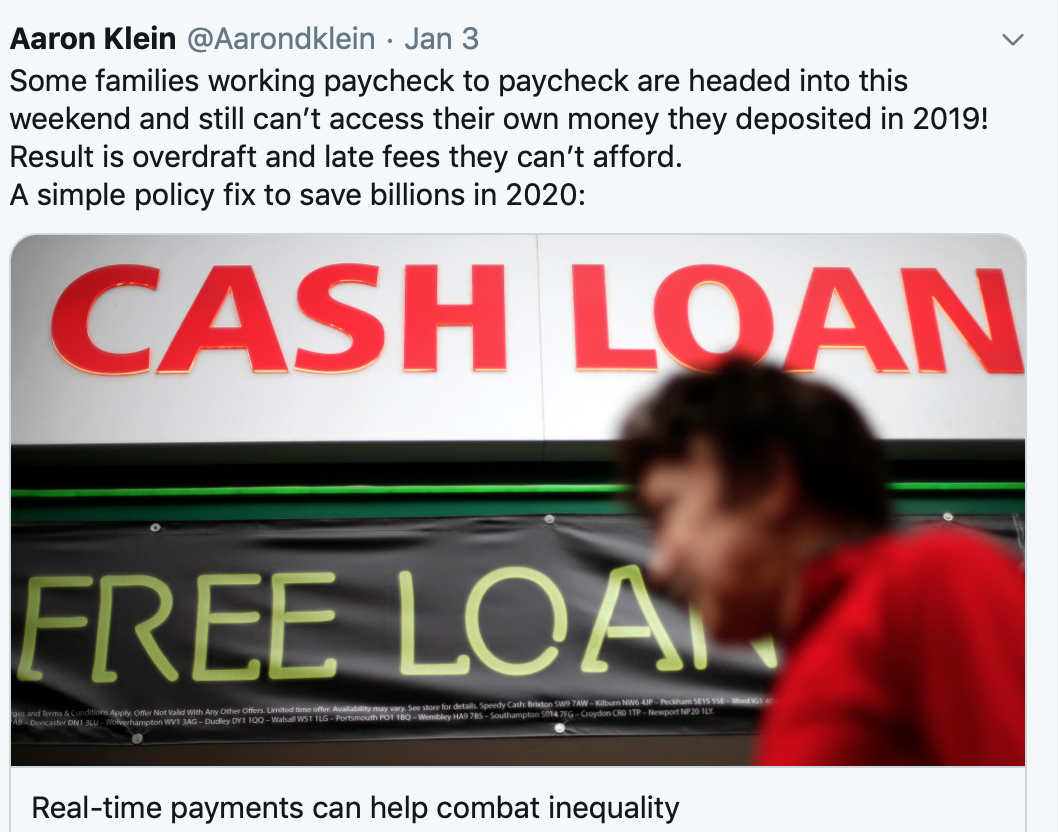

https://www.brookings.edu/opinions/real-time-payments-can-help-combat-inequality/

Importance of Real-Time Payments

Text

https://www.brookings.edu/opinions/real-time-payments-can-help-combat-inequality/

Payments

500M users in India

free international transfers at Interbank rates

used by >60% of total population in Denmark

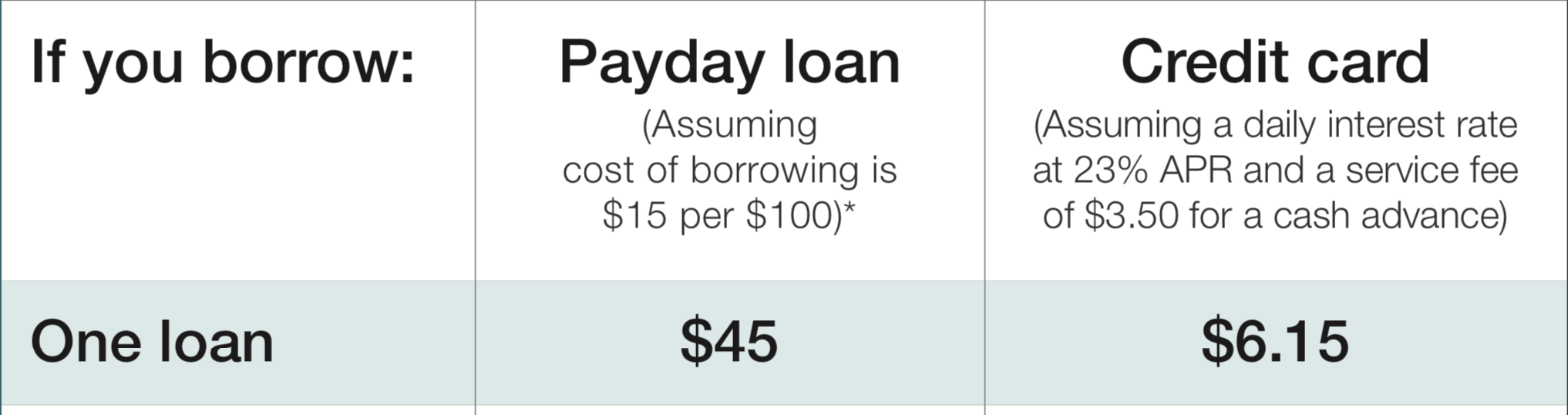

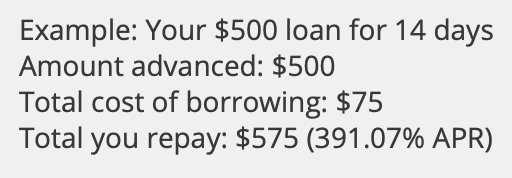

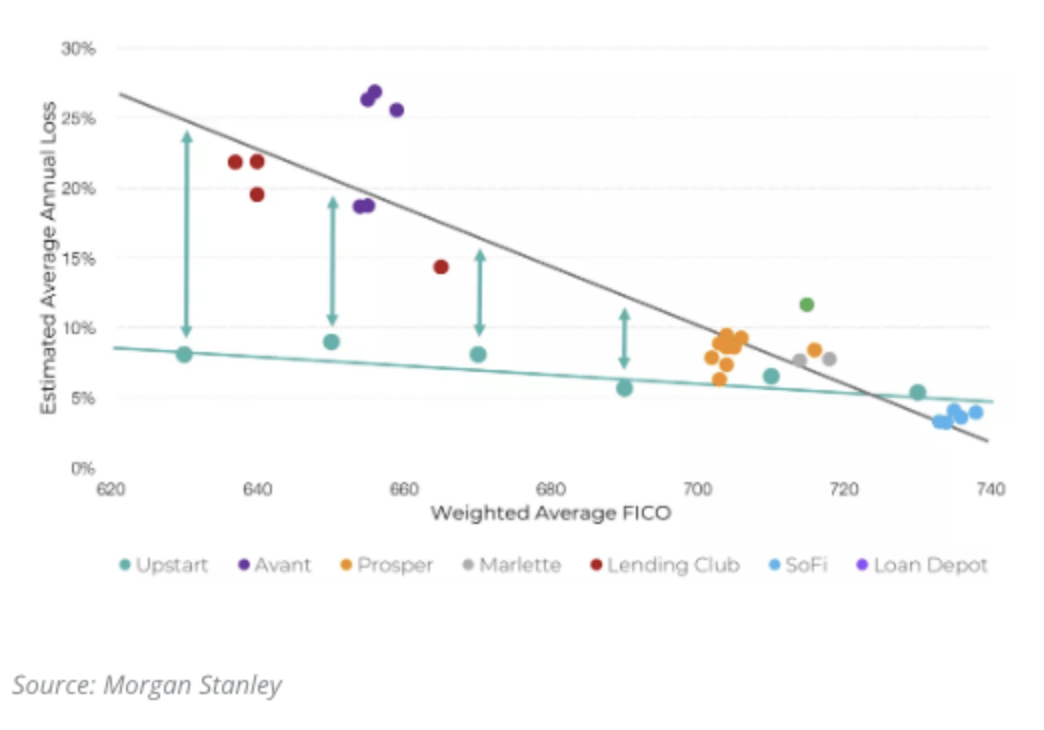

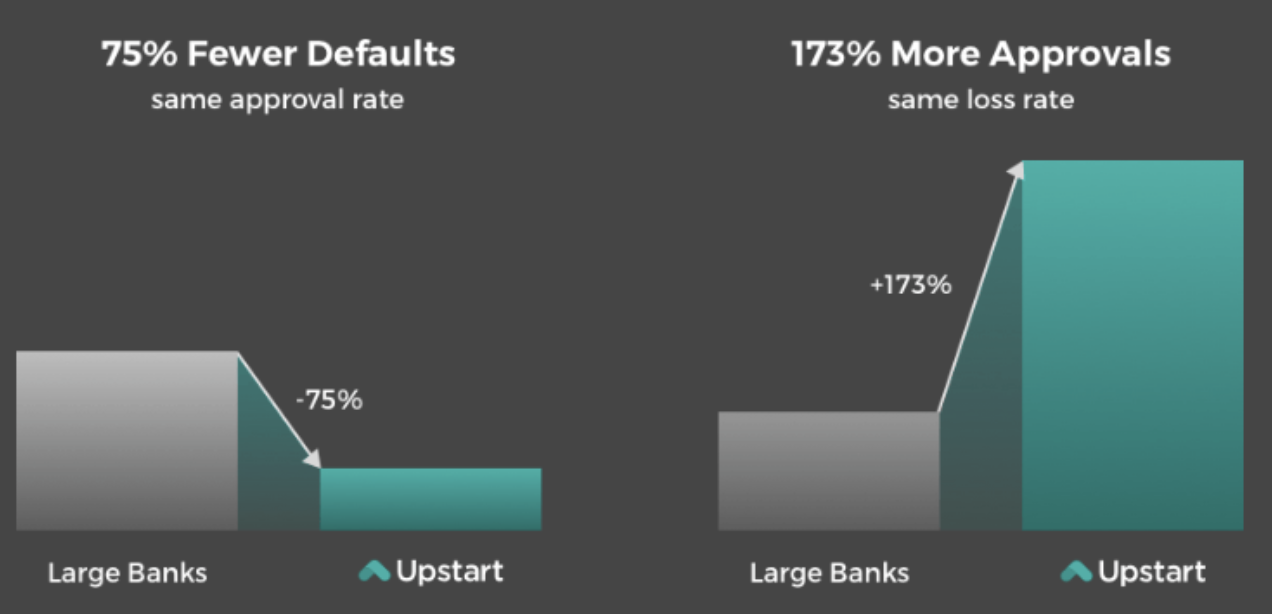

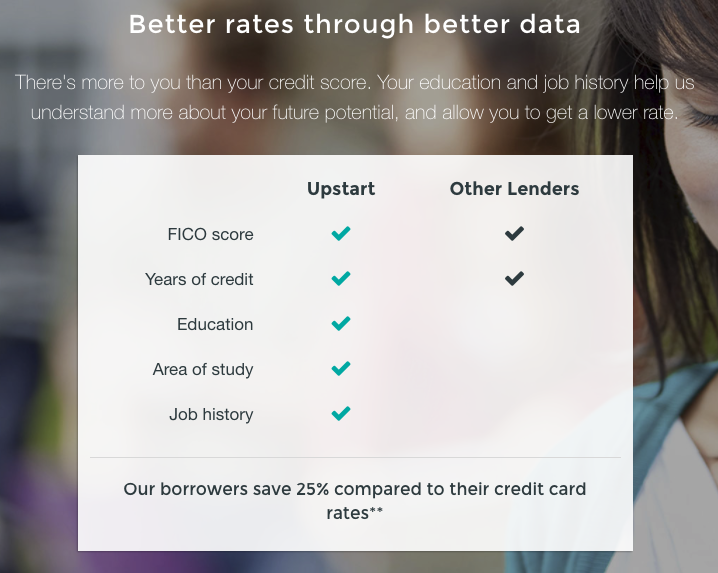

Lending and Borrowing

price for loan

effort required to get loan

Lower losses than competitors

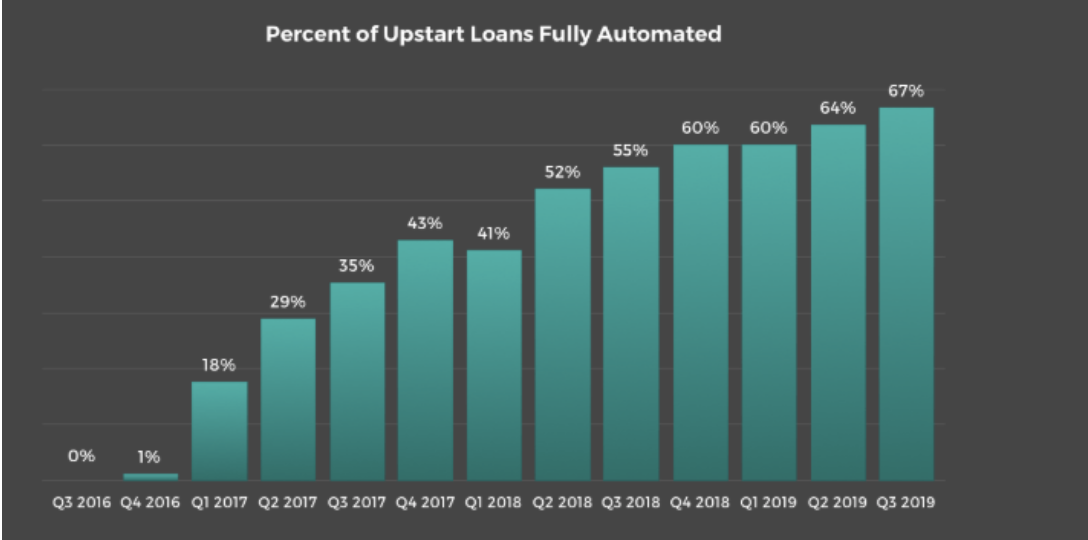

Example: Upstart

Tools?

AI& Machine Learning

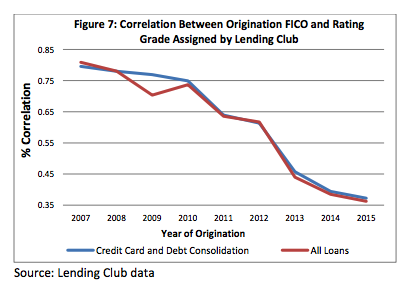

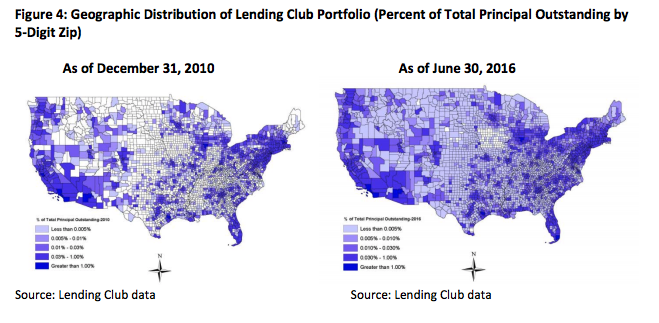

Example: Lending Club

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Future: Scalability

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

some key changes in recent years:

Nokia's market shares for devices:

What did they pay for?

What do people value?

As banks move data into "the cloud," why do we need banks?

By Katya Malinova

This deck is for the first lecture of F741 'Intro to FinTech". The slides are organized in a 2x2 array. It is intended to be viewed "column by column" (i.e., go "down"first and then "right").