Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Workshop on Frontier Areas in Financial Analytics

May 2019

The Fields Institute

Katya Malinova and Andreas Park

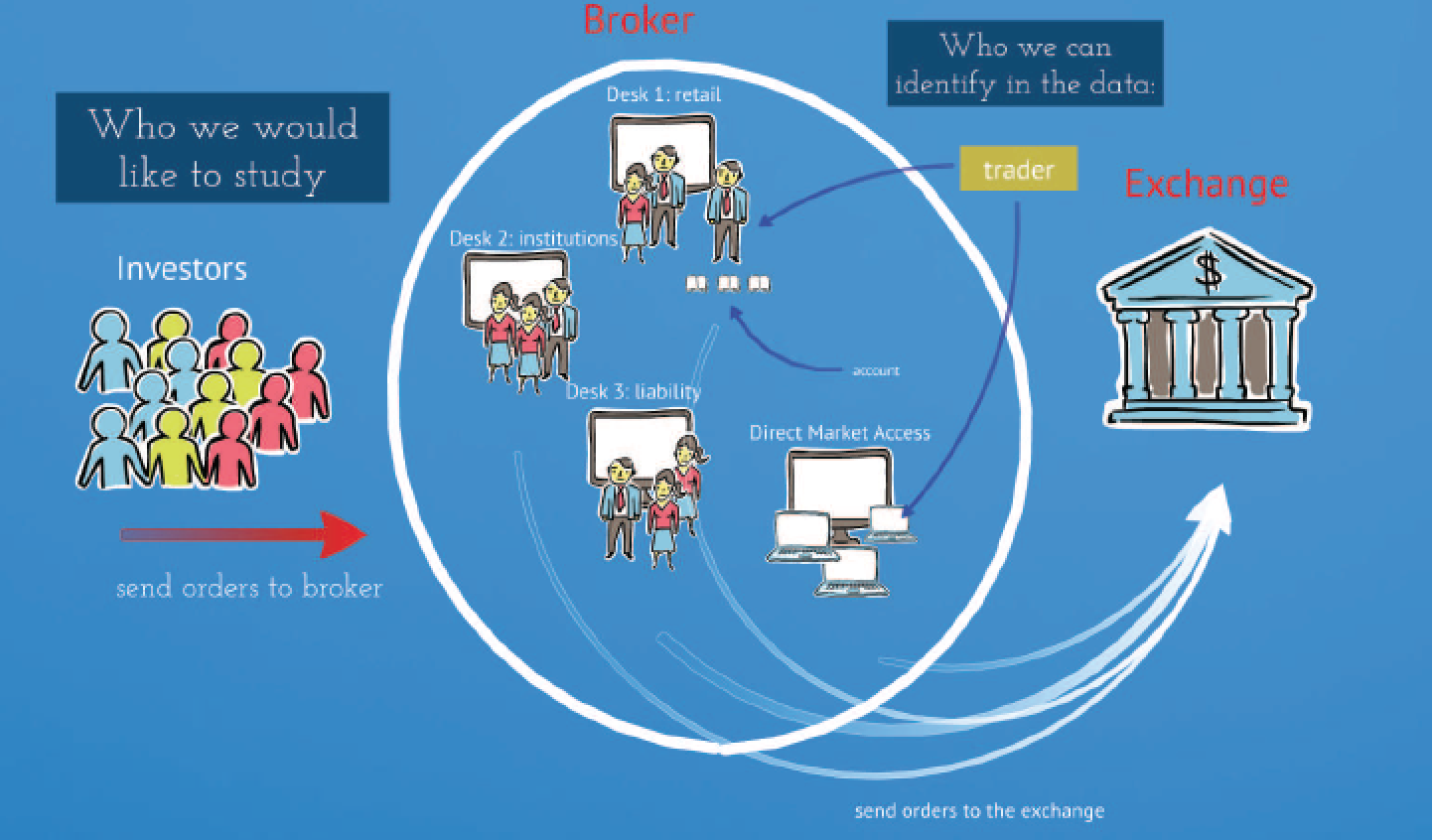

traders report that after they submit orders, all hell breaks loose:

quotes "fade"/"slide" on other venues

"others" get to trade on other venues before them

=> HFTs and fragmented markets are at fault

What do HFTs do after trades?

1,000

Shares at Canadian Offer

300

400

Regular Joe sends buy order to broker

buy 1,500 shares

no trade through => broker must split among three venues

Shares

1-tick off

400

100

2,000

1,000:

Shares at Canadian Offer

300:

400:

100

100

100

100

100

100

100

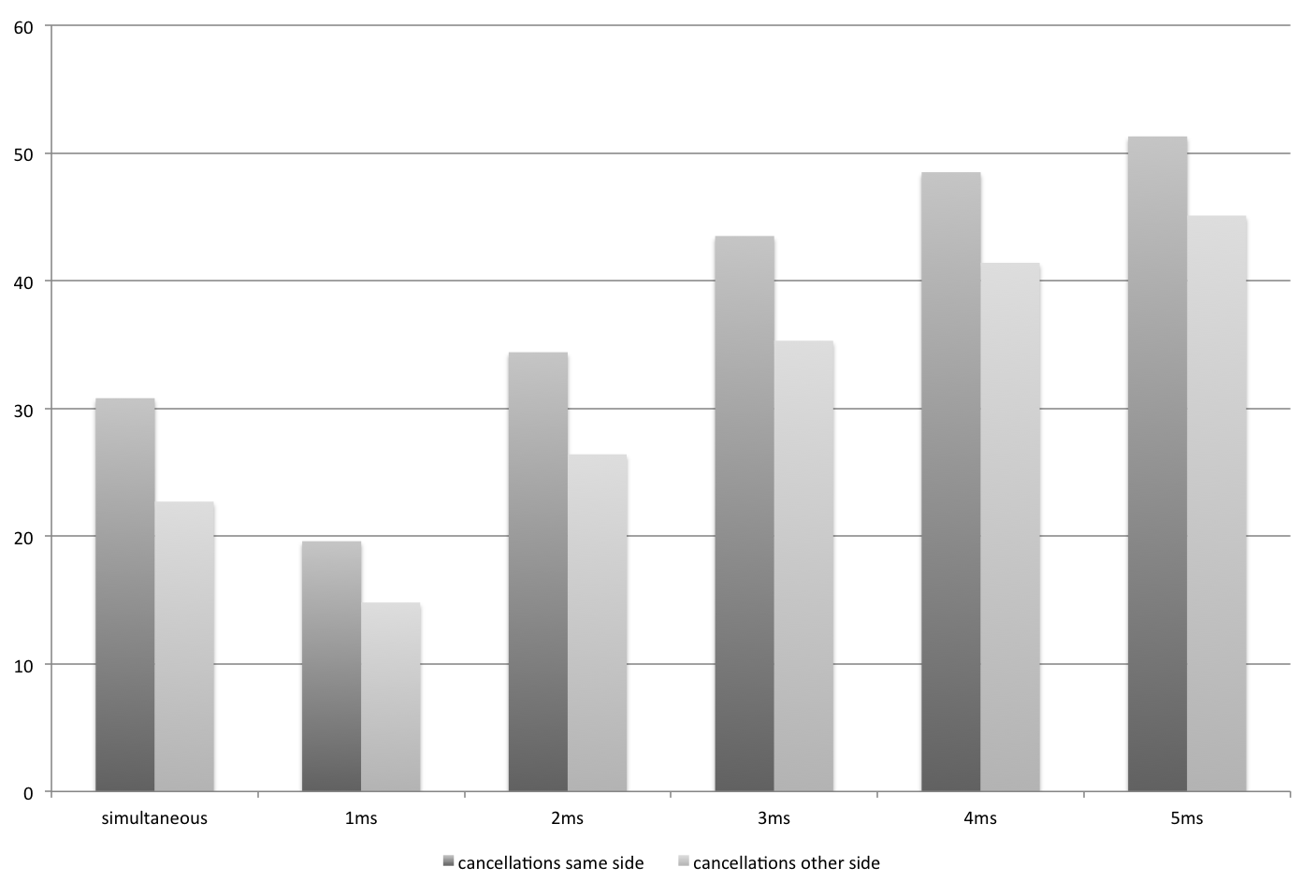

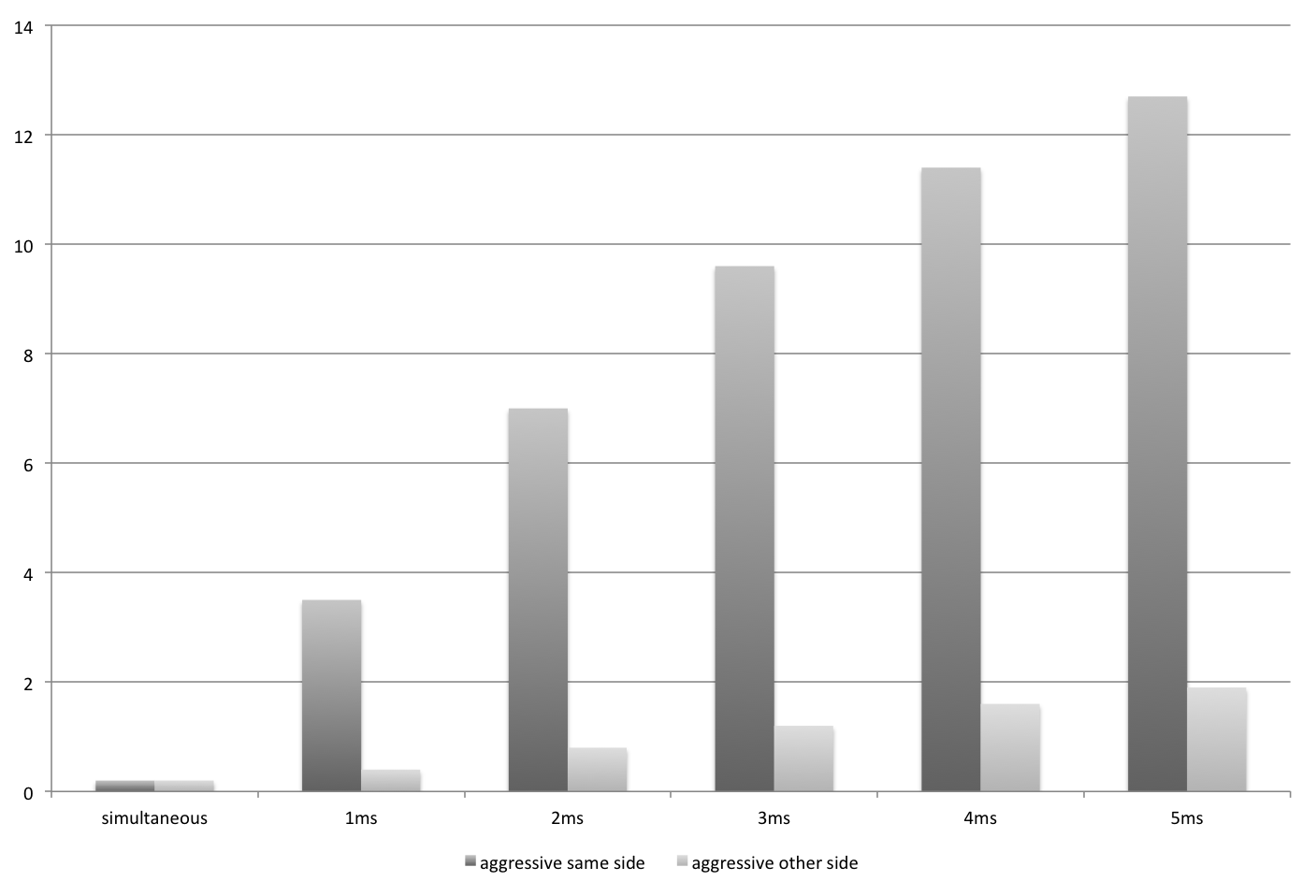

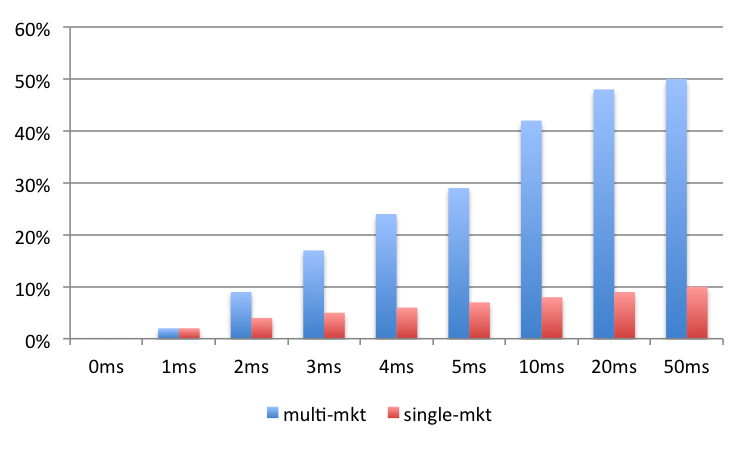

50% of trades -- by a non-HFT -- are quickly followed by a cancellation -- by an HFT -- on a different venue within 5ms of the trade

Within 50ms: about 70% of trades followed by cancels

13% of trades -- by a non-HFT -- are followed by an aggressive trade -- by an HFT -- on another venue in the direction of the original trade within 5ms

Within 50ms, 29% of trades are followed

Step 1: Characterize/describe fast (HFT) traders’ reaction to trades:

size?

type of trader?

information?

Our focus:

HFTs in regulation-mandated integrated mkts

proprietary masked trader-level data for all Canadian equity markets (provided by IIROC, the Canadian regulator)

use 30 most frequently traded non-crosslisted stocks, March - May, 2013.

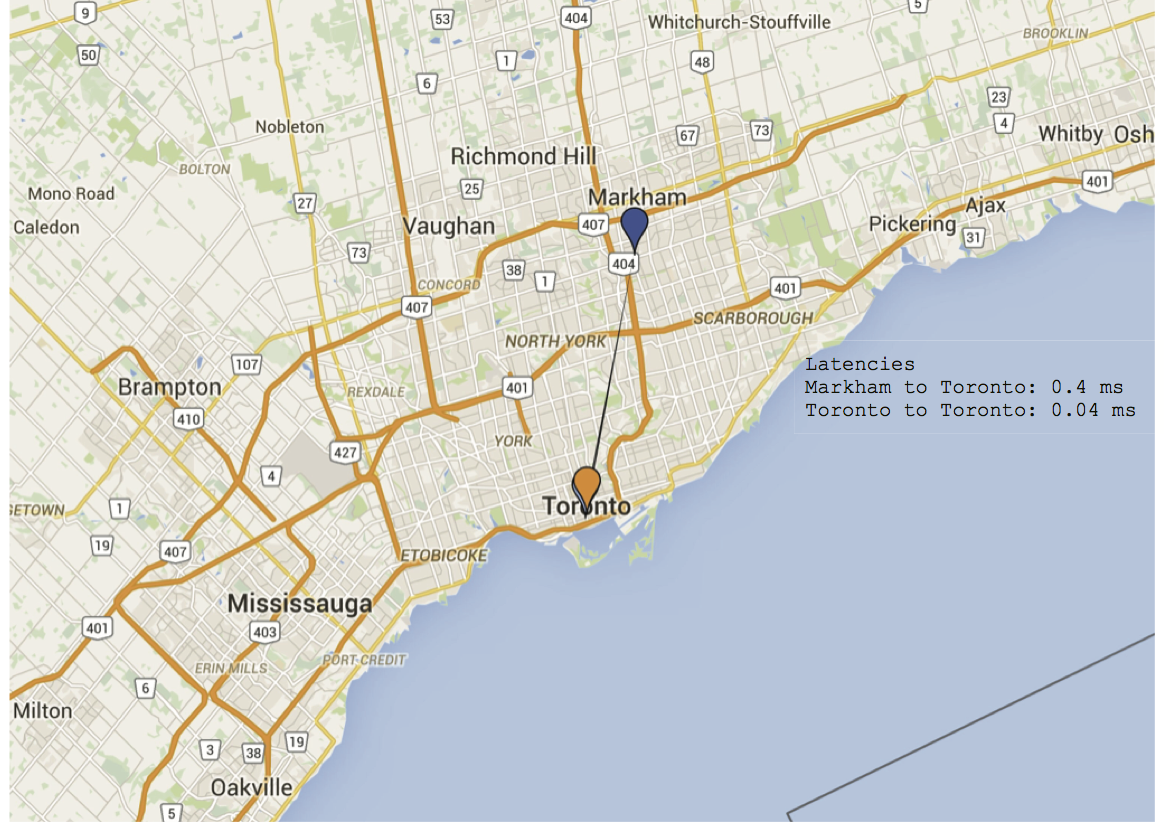

a critical market-organization change that eliminated latency between two of the three main markets (markets A and B) on April 29, 2013 => identification

Similar to Comerton-Forde, Malinova, Park (2018)

Fast traders: Use three criteria (across many securities on many days: 307 securities, Jan& Feb, 2013)

regularly submit and cancel orders very quickly

median submit-to-cancel times < 250ms.

submit/cancel most orders very quickly subsequent to someone else’s activity

85% of activity within 1ms of someone else.

react quickly (500ms) to a particular, regular, market-wide news announcement (the market-on-close imbalance).

classified: ~82 (out of ~4,900)

post on multiple venues => cancel to avoid overtrading

learn new info => cancel/reprice existing quotes + "backrunning"

accumulate inventory => revert (=trade aggressive with trade)

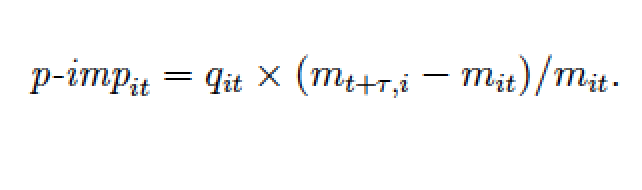

Trades = information.

Naive conclusion: multi-market trades have higher price impact, therefore they are more informed

Consistent with Baldauf & Mollner and van Kervel:

multi-market = smarter

HFTs must react stronger!

End of story?

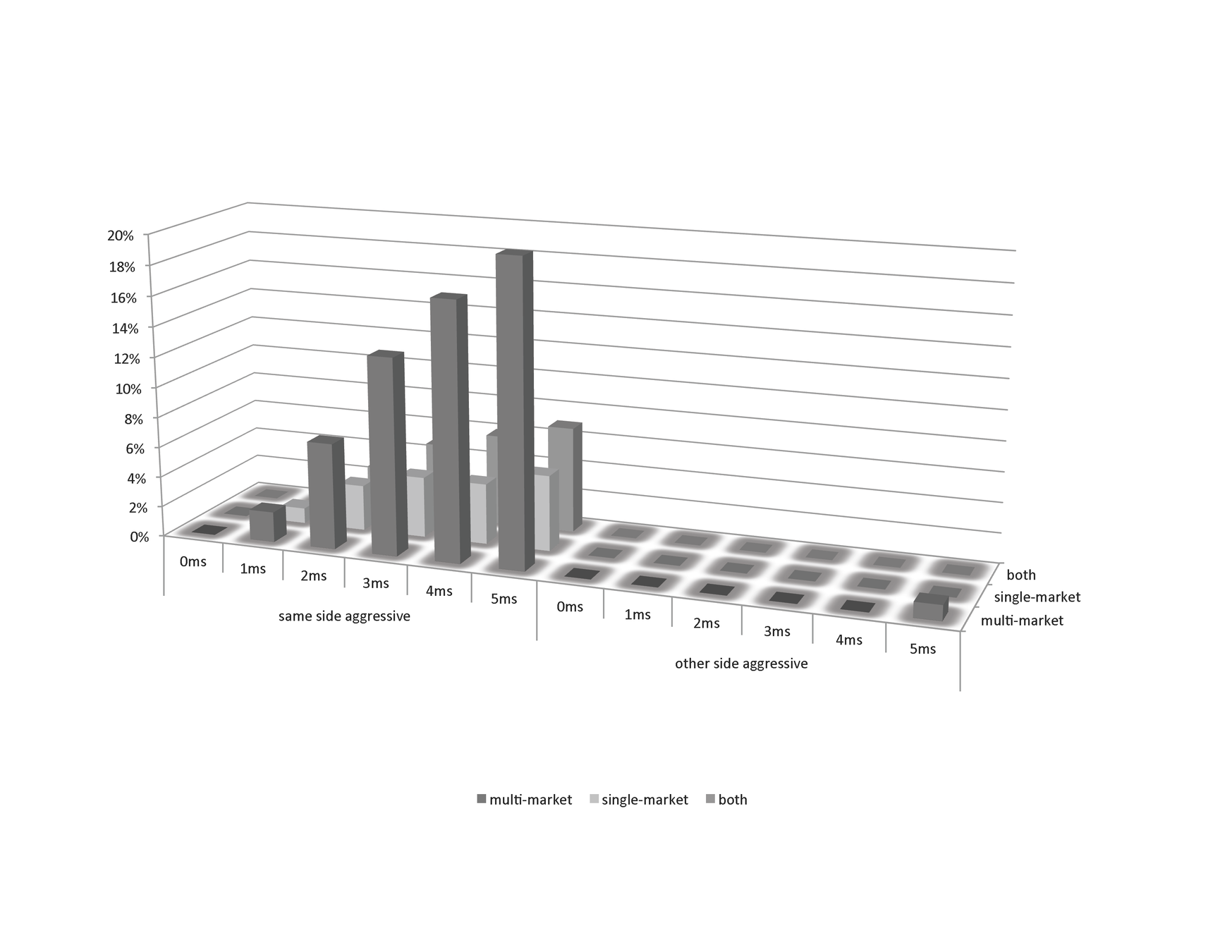

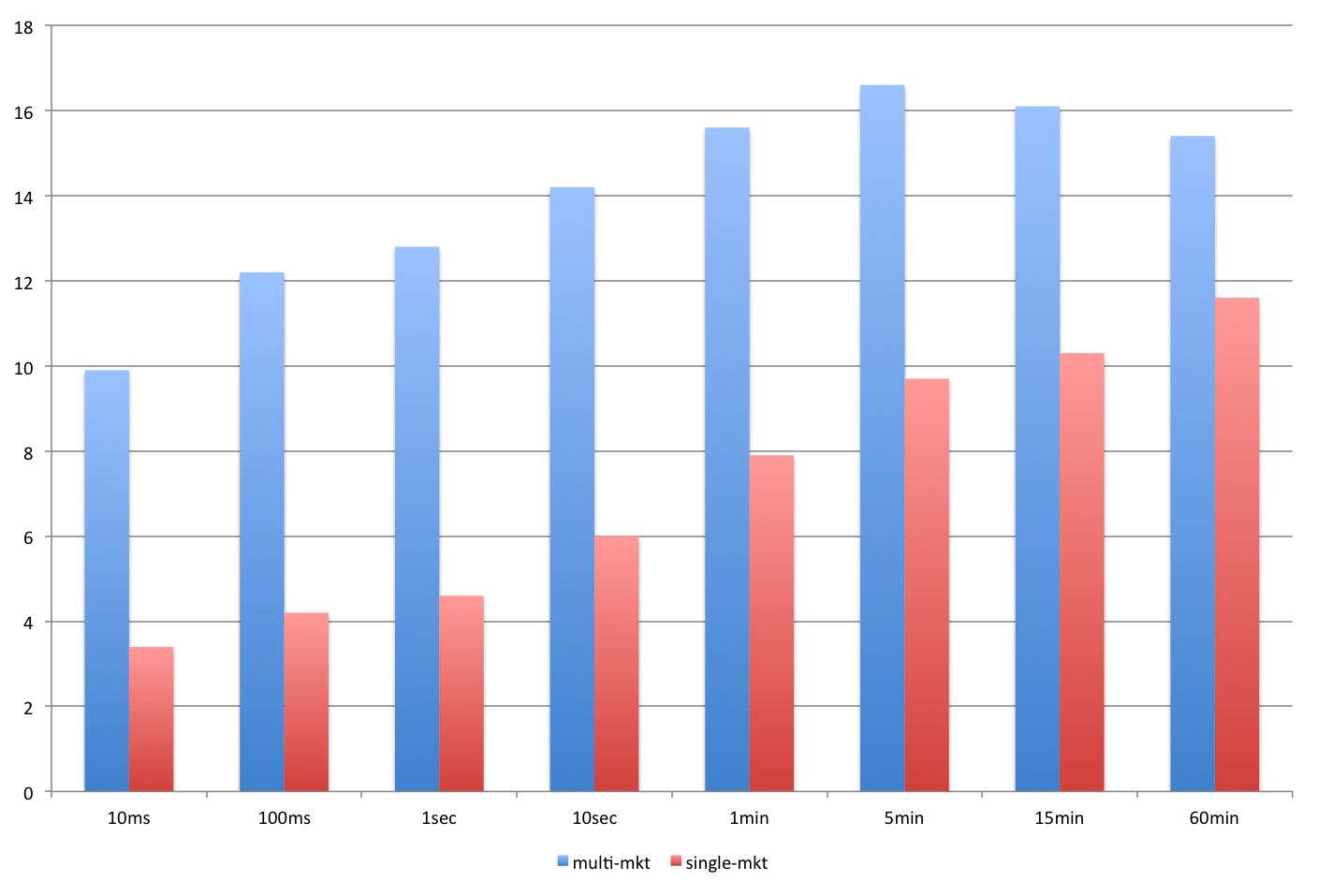

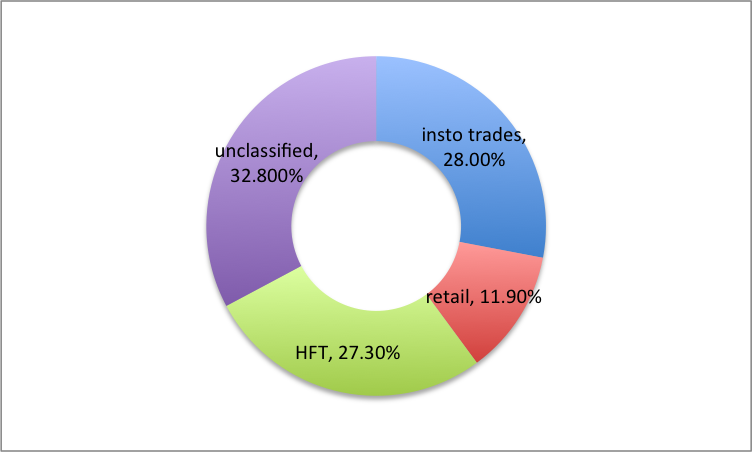

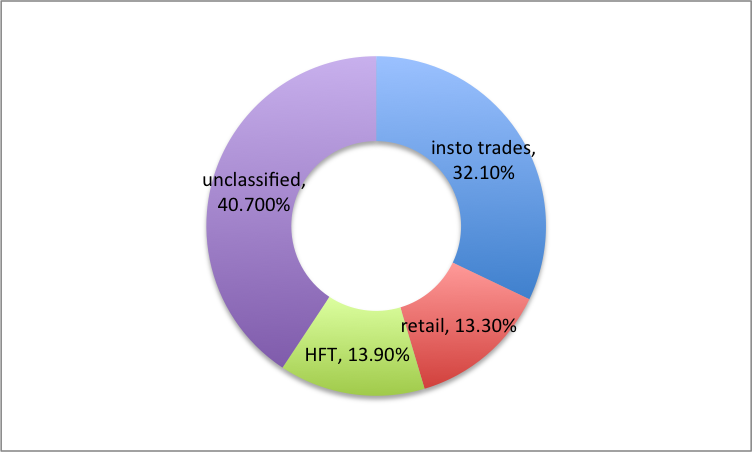

All trades

Multi-market trades

Multi-market trades:

\(\approx\) 32% of total $-value

Conclusion: If we believe that retail orders are not informed, then the price impacts for single vs. multi-market orders shouldn't look this different.

Reminder:

Multi-Market

Single Market

vs.

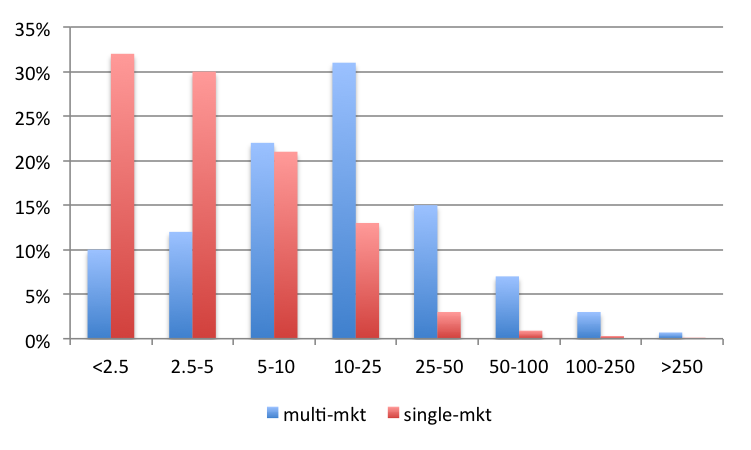

| trade size | % of all value | % of multimarket value |

|---|---|---|

| 100-200 | 23 | 3 |

| 201-500 | 17 | 11 |

| 501-1,000 | 15 | 15 |

| 1,001 -- 5,000 | 25 | 36 |

| >5,000 | 19 | 36 |

$ value of trades per bucket

$ value of all trades

$ value of multi-mkt trades per bucket

$ value of all multi-mkt trades

Conclusion: multi-mkt orders are larger

Is it size?

Single Market

Multi-Market

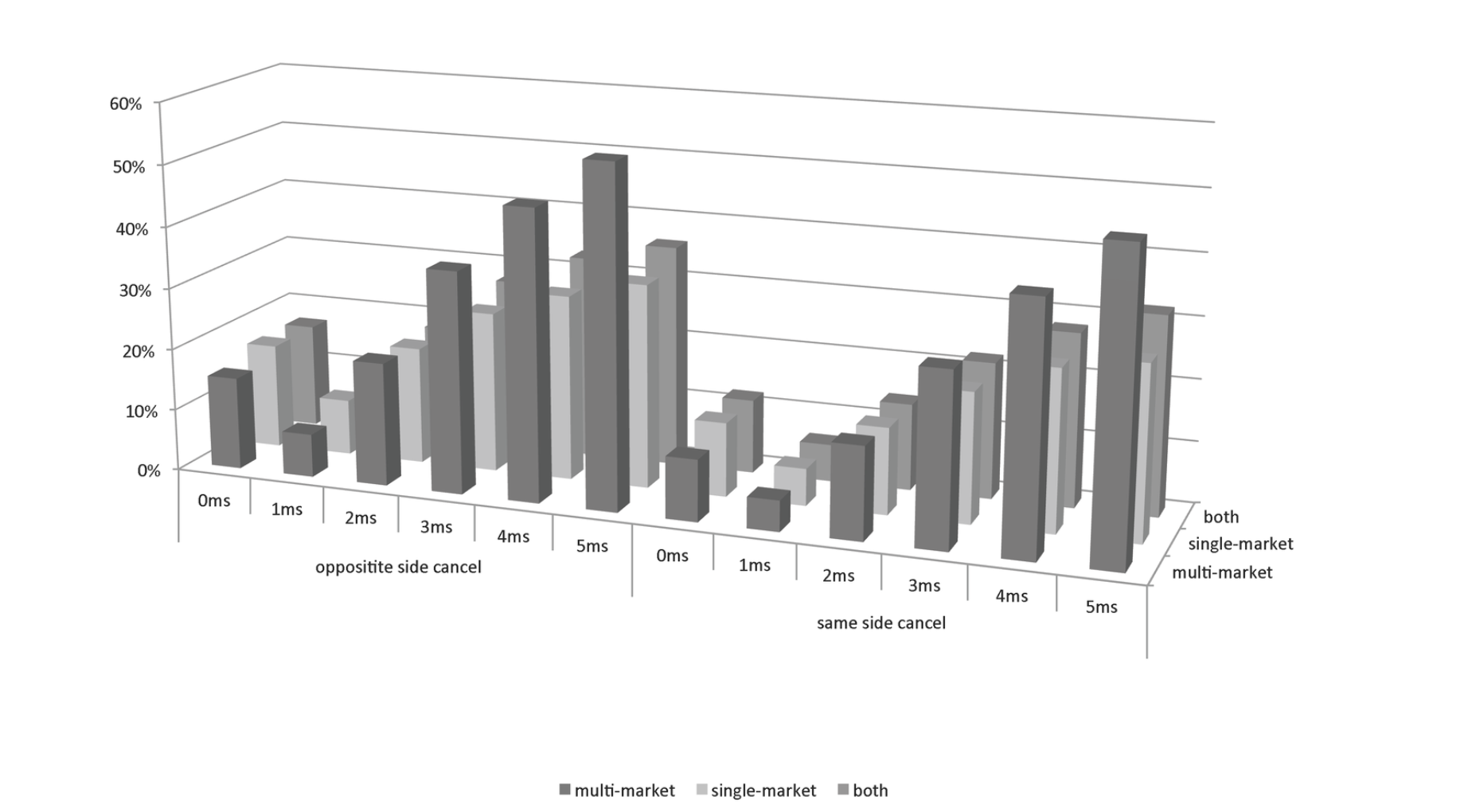

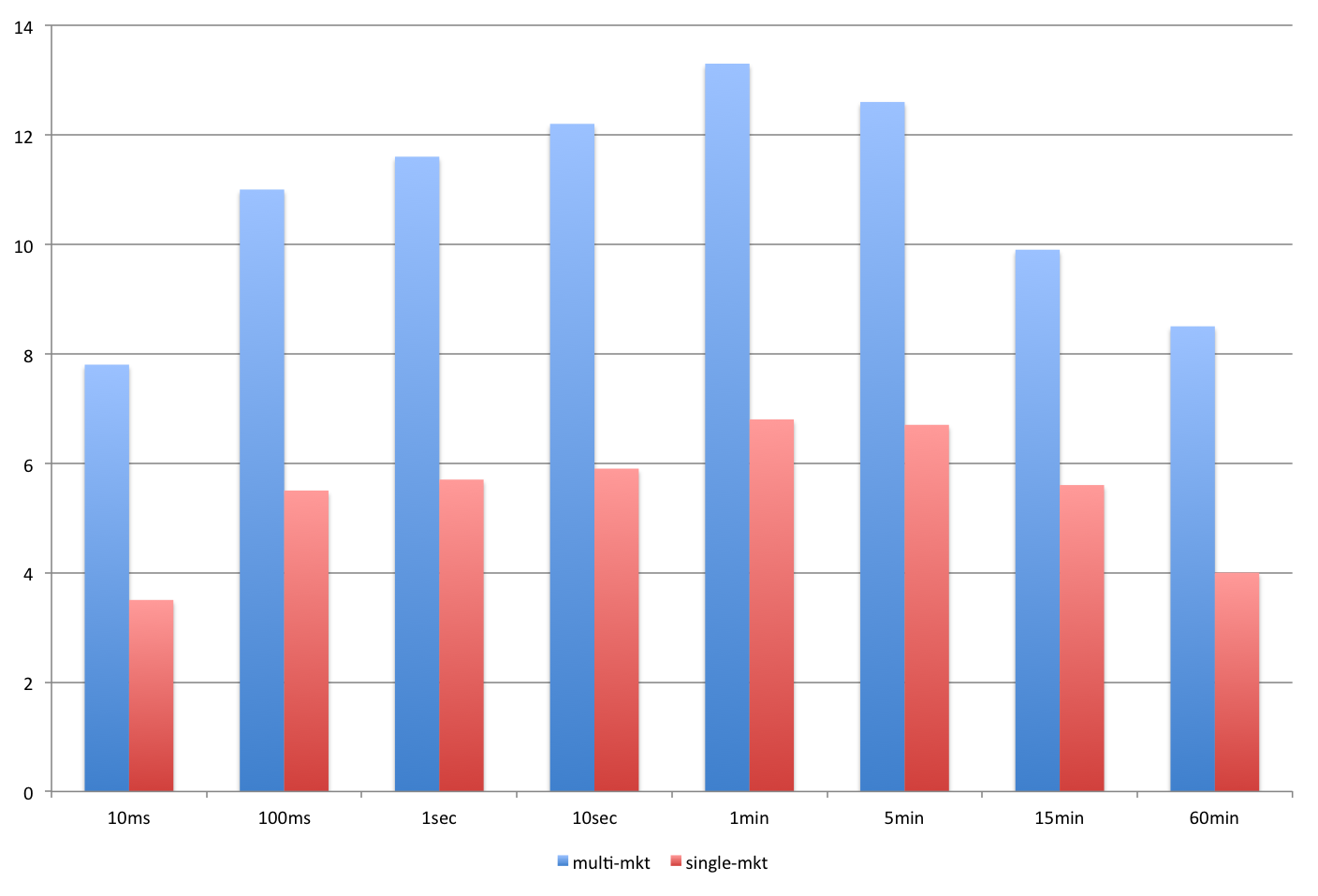

Plotting: price impact multi-mkt minus single-mkt

Conclusion: even for similar size, price impact of multi-market orders is larger.

Is it size?

Plotting: price impact with HFT reaction minus price impact without HFT reaction

reaction = cancellations

Reaction= trades

fast aggressive orders(same direction minus opposite direction)

total number of transactions

Conclusion: HFT reaction looks like there is much more activity than warranted by the original trade

Multi-Market

Single Market

| Single Trader | Multi Trader | |

| Single Mkt | ||

| Multi Mkt |

| Dummy | Coeff controlling for the vol of the first trade | Coeff controlling for the aggregate cluster volume |

|---|---|---|

| MultiMkt-SingleTrader | 0.645*** | 0.605*** |

| SingleMkt-MultiTrader | 1.919*** | 1.132*** |

| MultiMkt-MultiTrader | 2.095*** | 1.137*** |

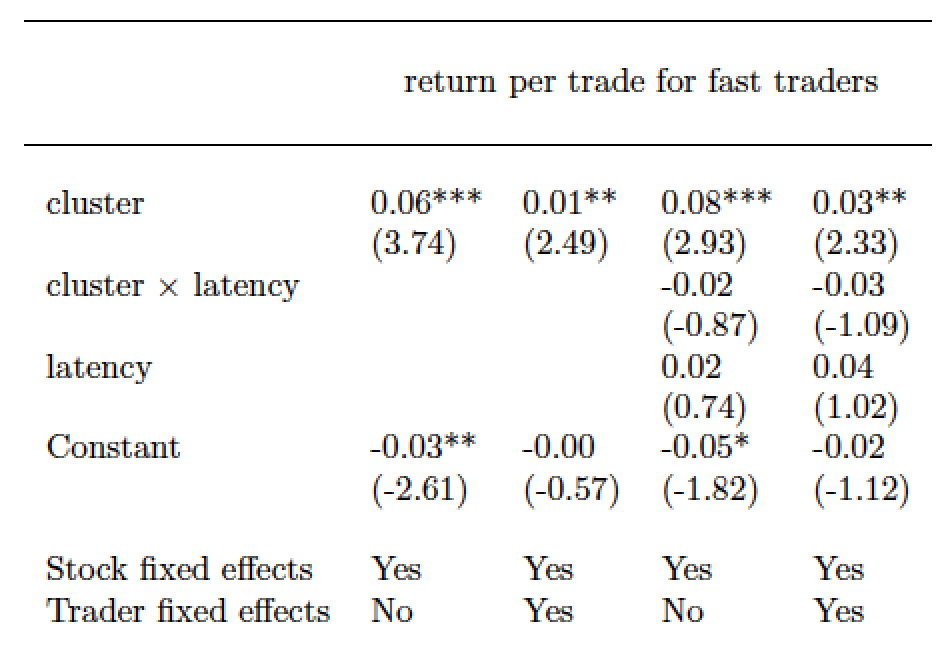

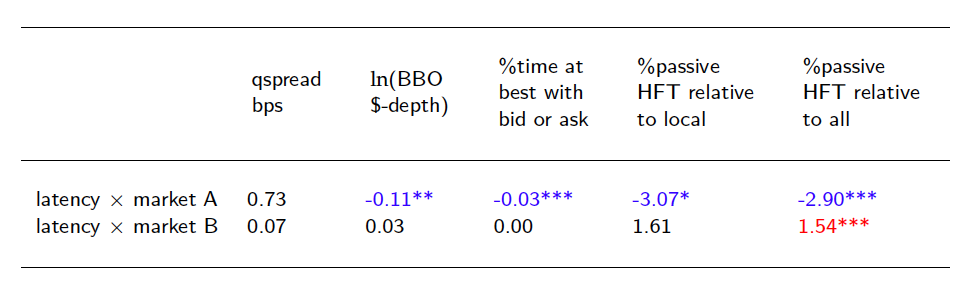

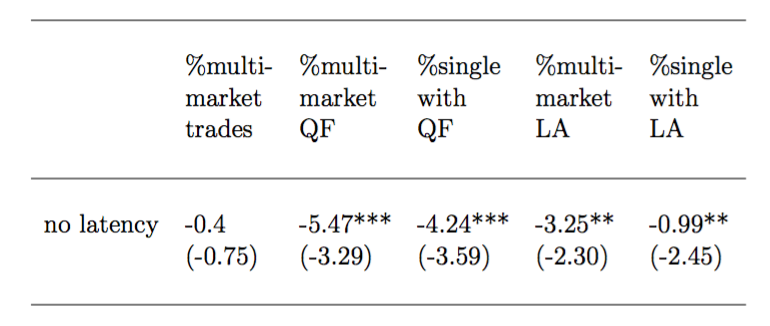

Market A and B move to the same data centre: April 29, 2013

Examine changes in market quality and trader behavior

(no)

Untabulated: no significant changes in size or usage of multi-mkt trades

Bottom line: price impacts of multi-market orders decline

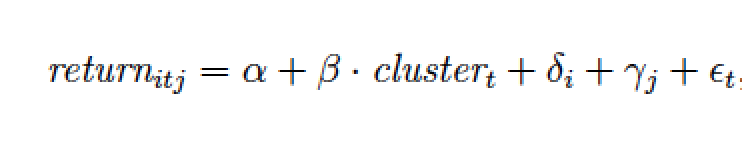

Difference in differences of multi- vs. single-mkt orders before vs after

By Katya Malinova

This is a deck that I used for a presentation at the Fields Workshop in May 2019