Katya Malinova PRO

I am an Associate Professor, Mackenzie Investments Chair in Evidence-Based Investment Management at the DeGroote School of Business, McMaster University, Canada.

Payments Part II

Instructor: Katya Malinova

Lectures 6-7

Feb 13

barter

coins/commodity money

paper money

fiduciary money

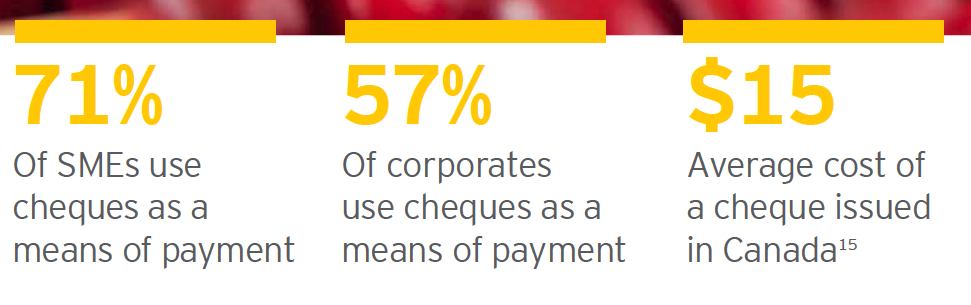

Time-consuming to move/process cheques

No immediate use of funds

Costly to process paper cheques

Cheques, Drafts ... "payment from an account"

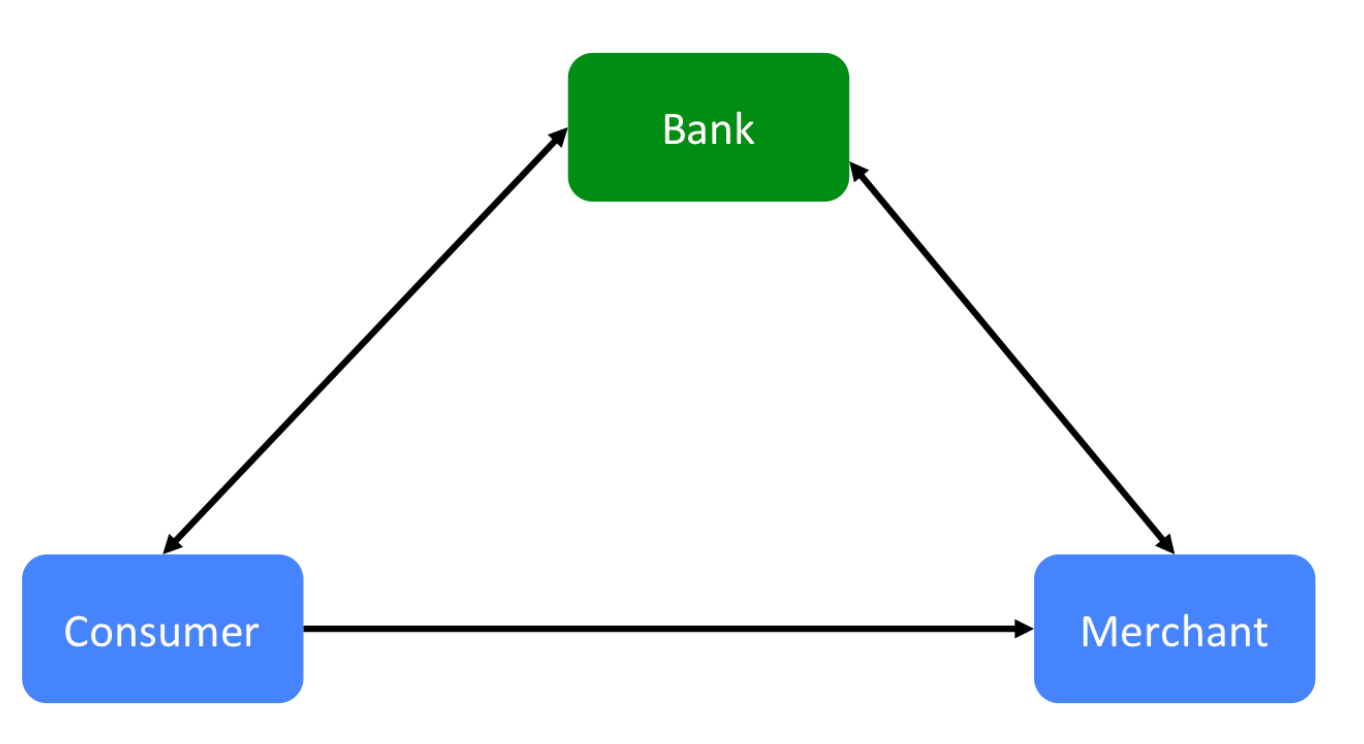

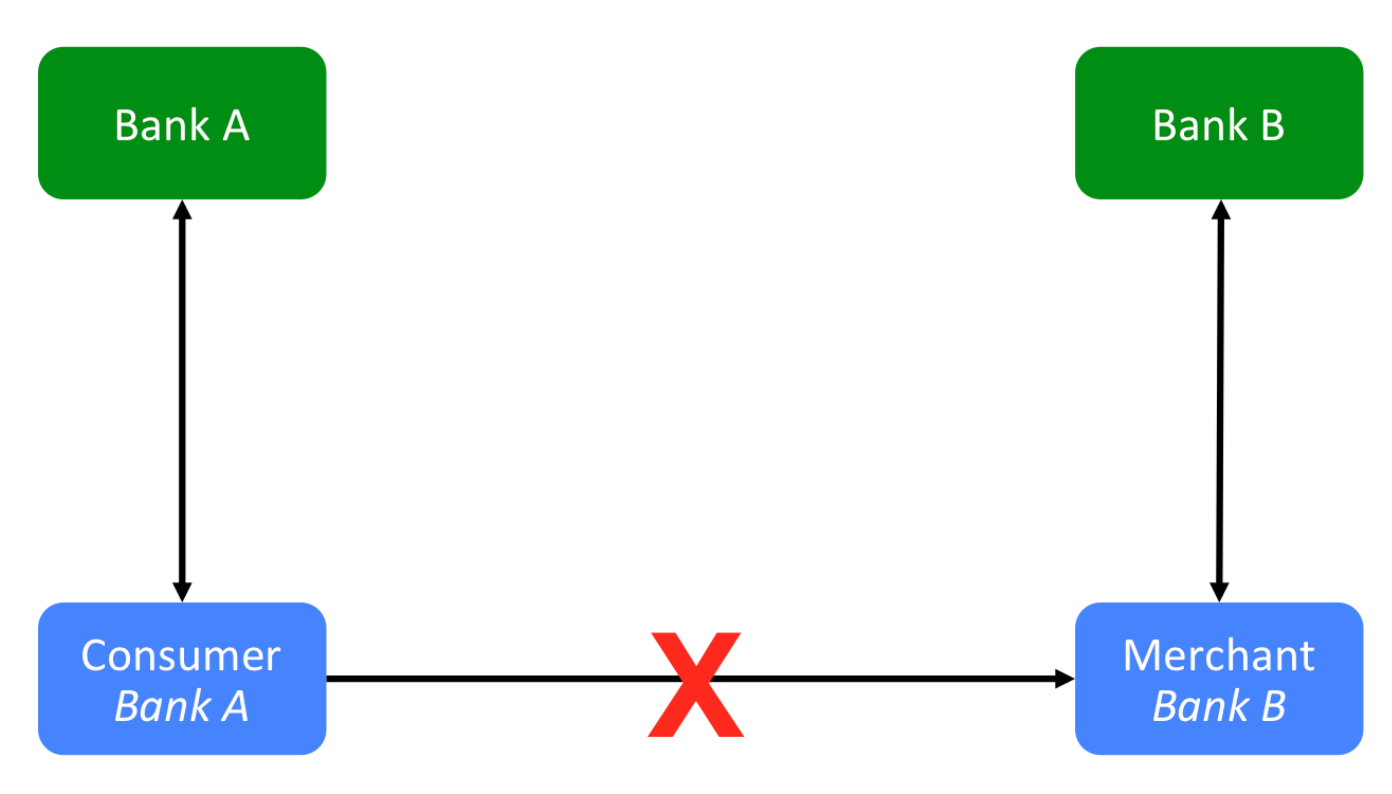

Imagine you run a bank

Wouldn’t it be great if your customers could go to local shops and “charge” their purchases to an account that you hold for them?

Make money offering credit to the customers and make some more money charging the merchants for providing this service.

https://gendal.me/tag/payments/

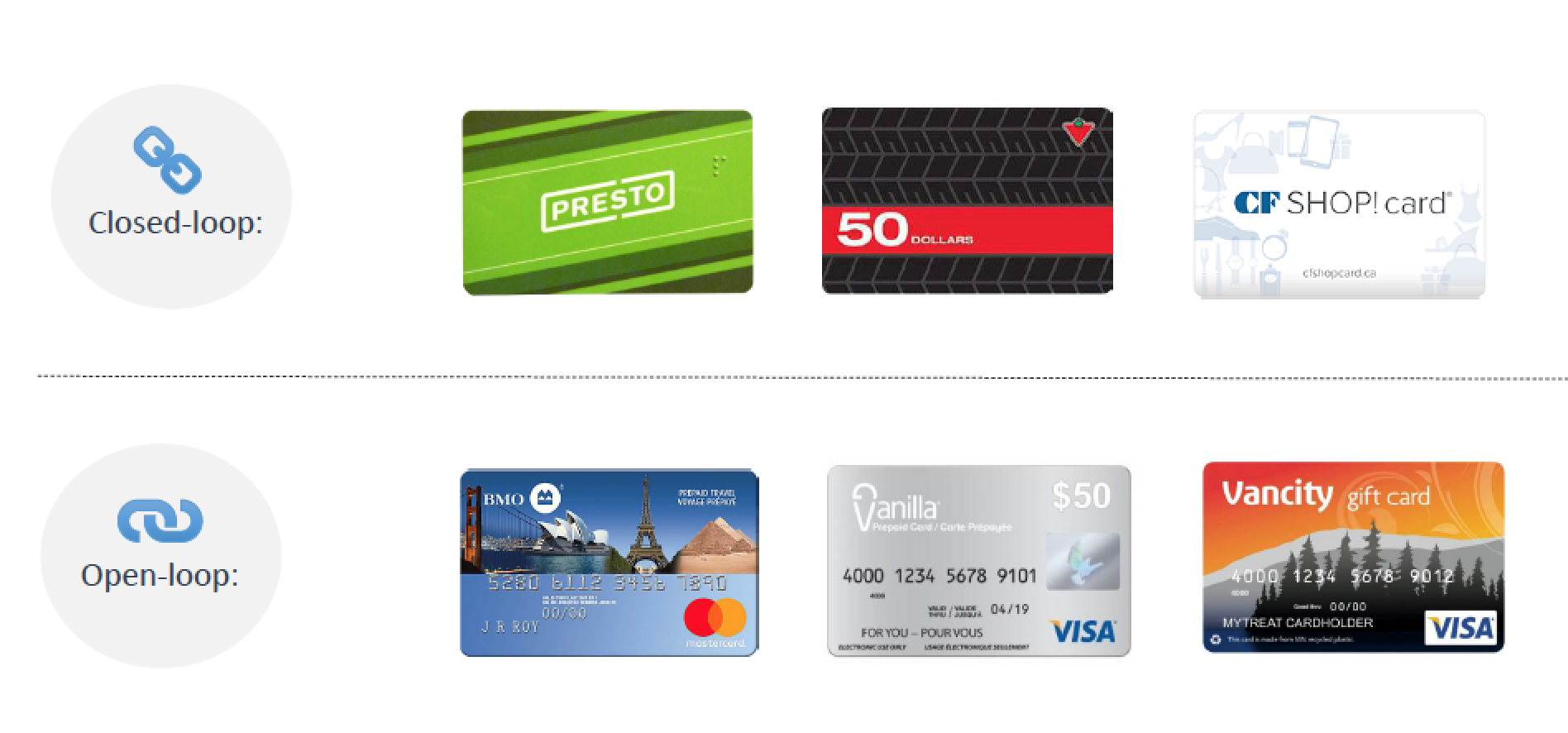

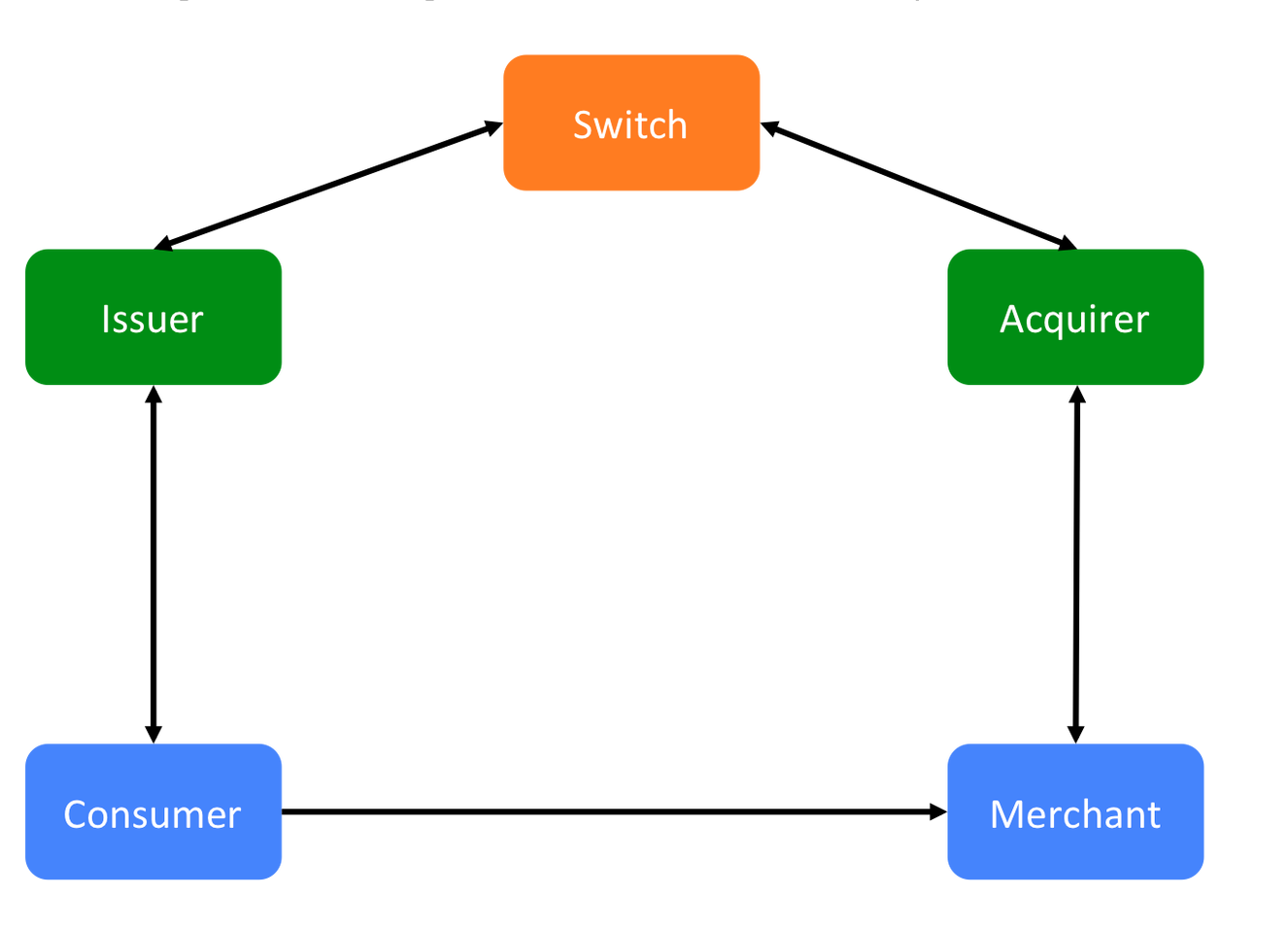

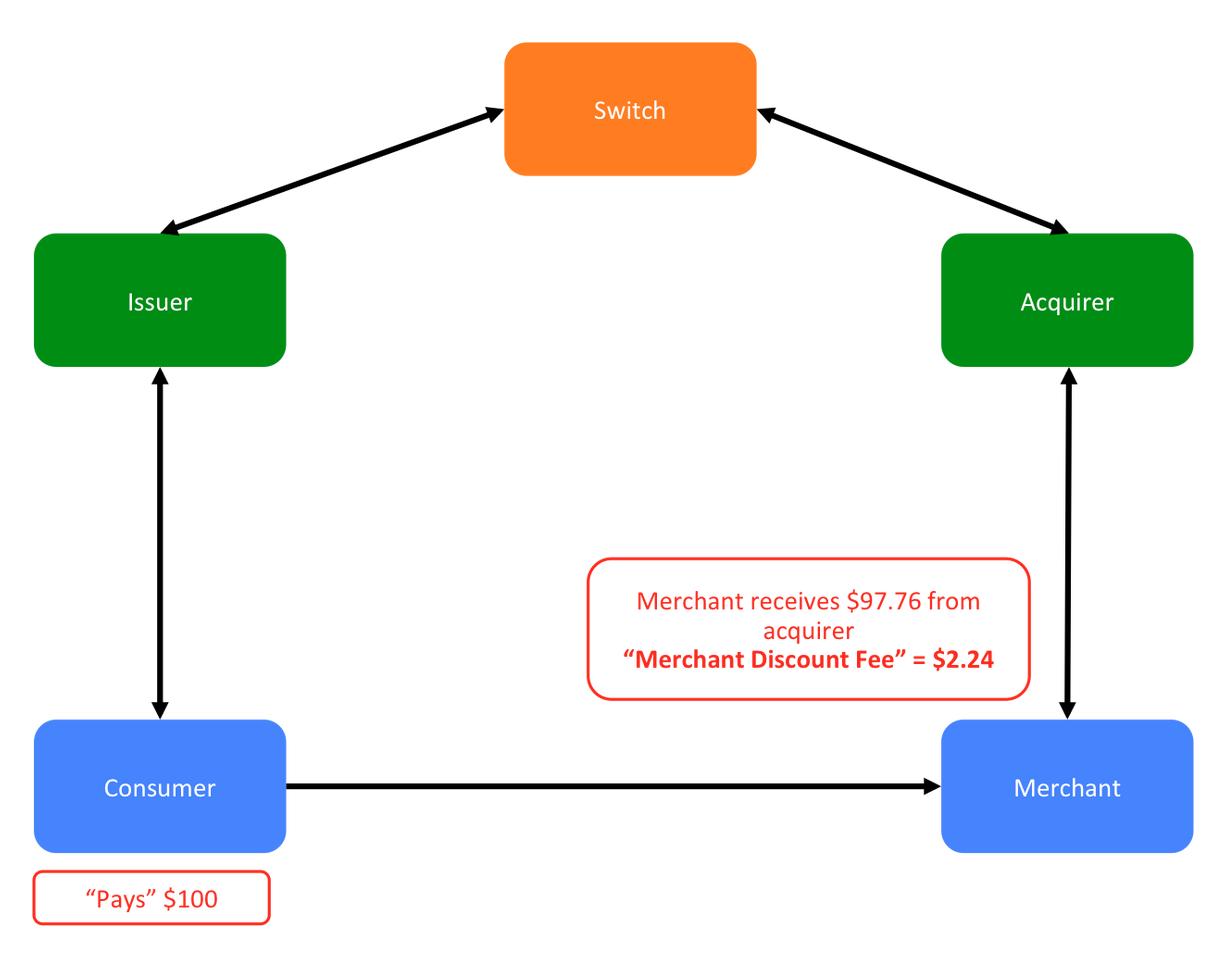

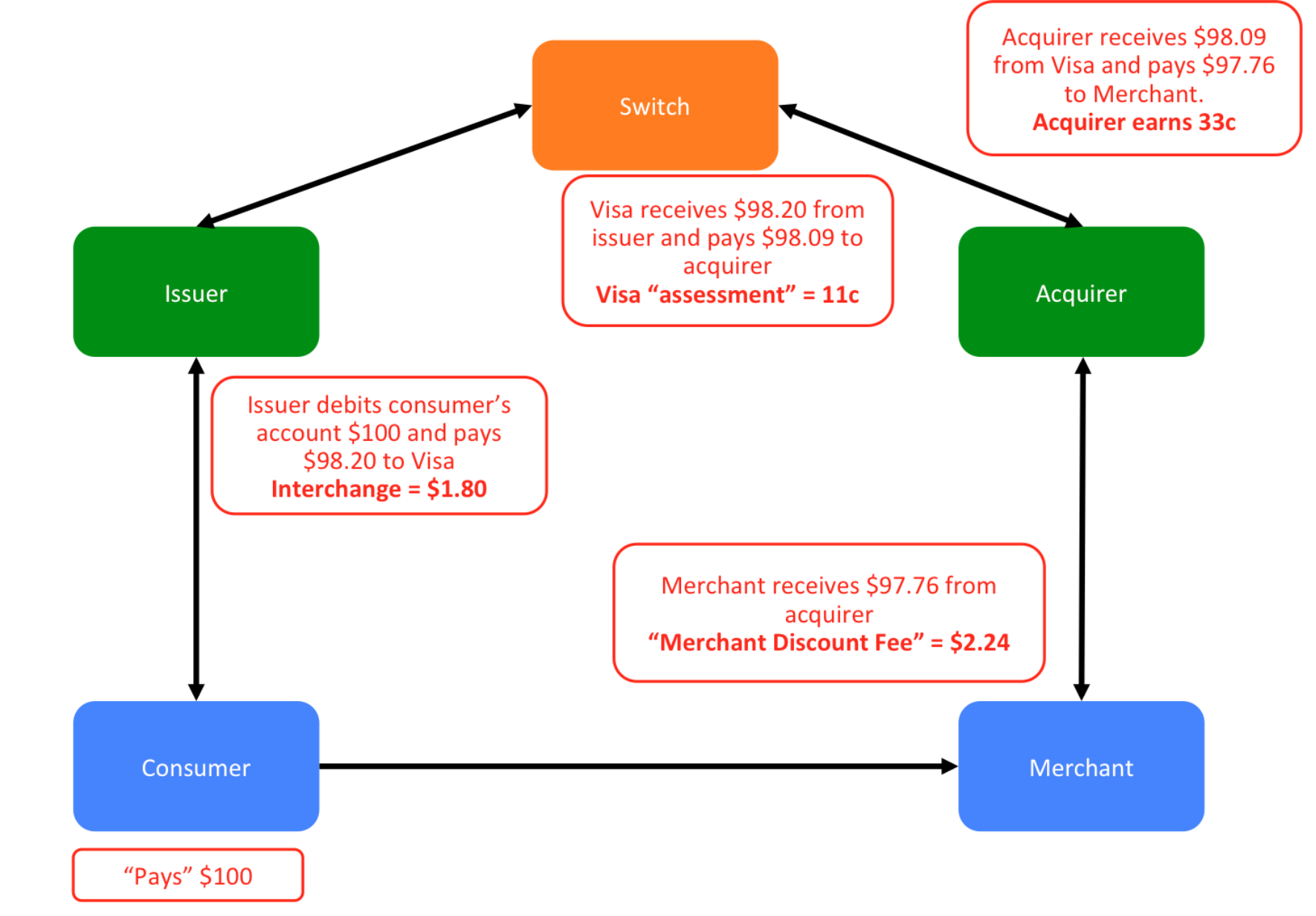

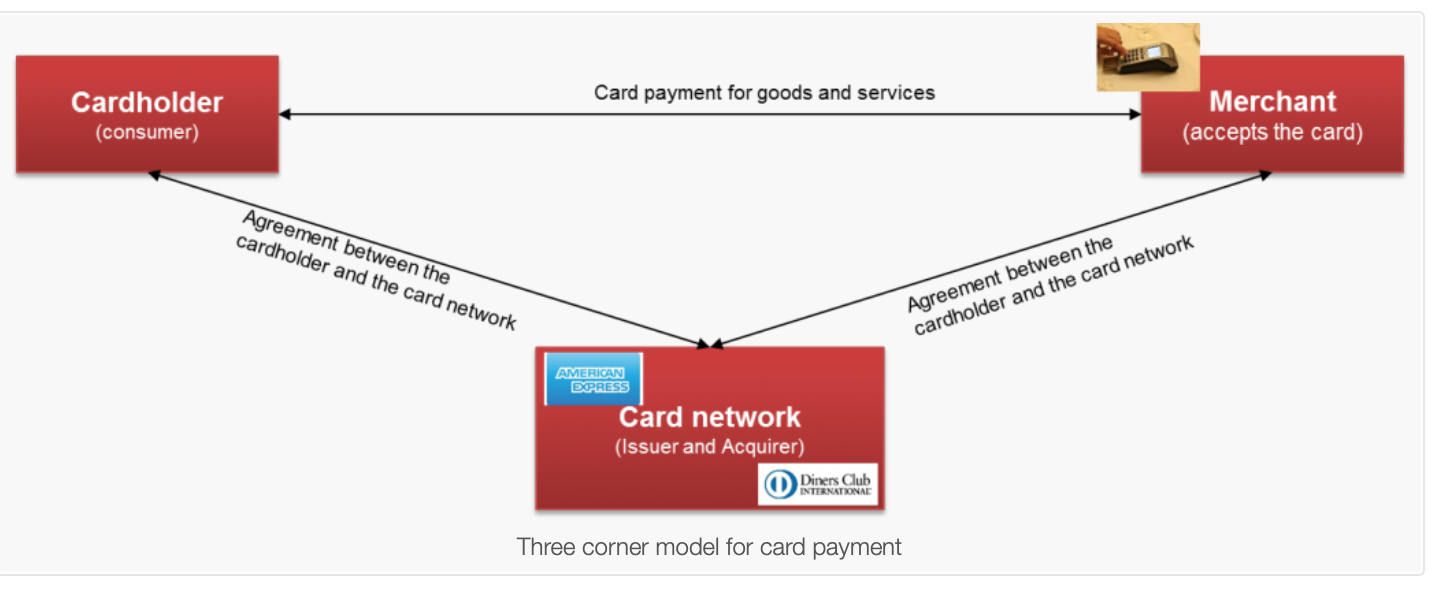

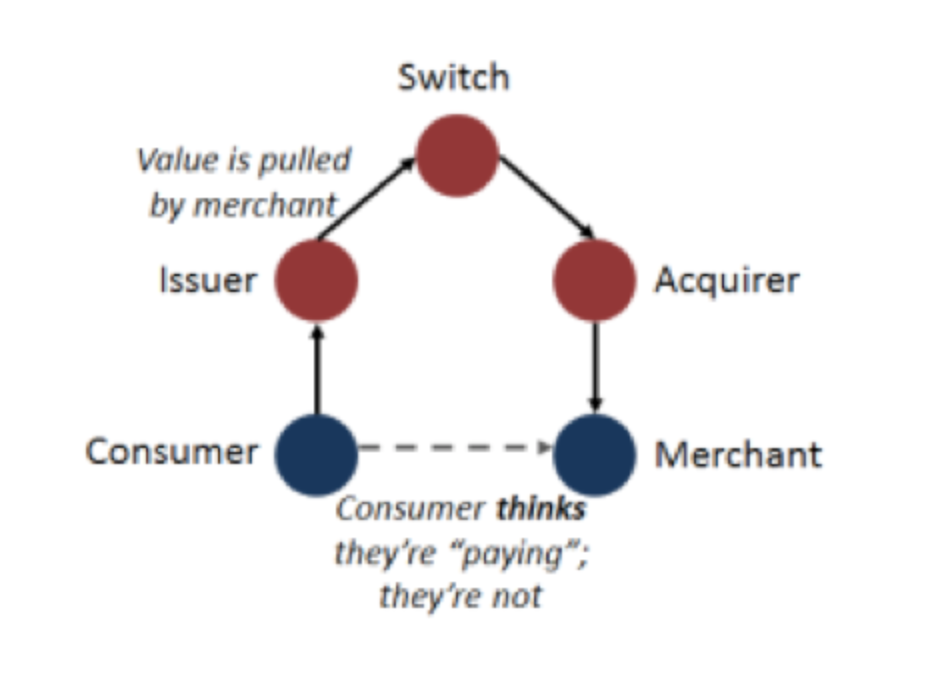

Cards "business"

= TWO businesses

Business #1: offering credit to customers & processing their payments

CARD ISSUING

Business #2: enabling merchants to accept card payments & to get reimbursed

MERCHANT ACQUIRING*

*The card payment = a receivable that the processor acquires from the merchant

Or: Payment Processor

Switch = set of rules + brand recognition for the merchants and customers that are members of this arrangement

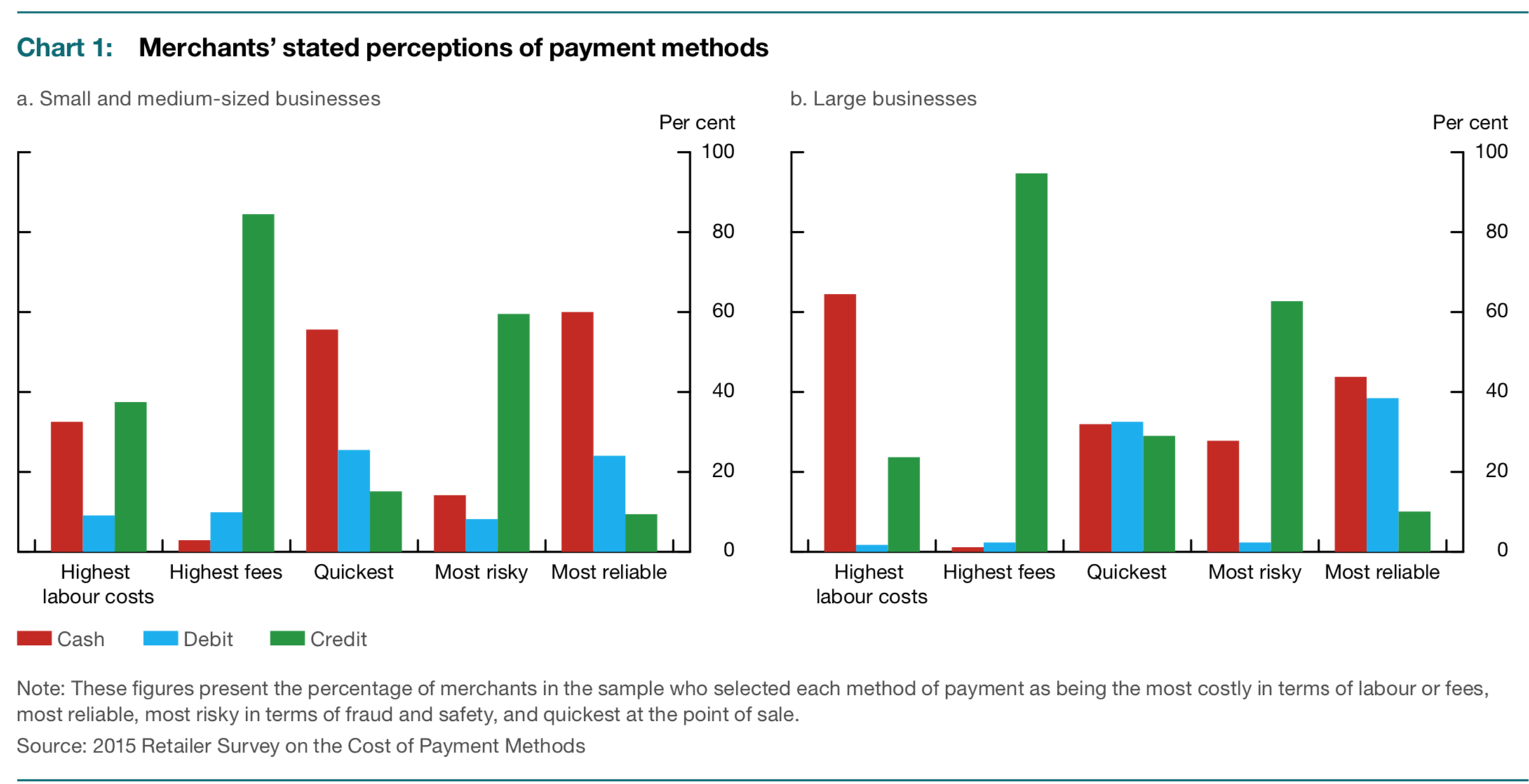

https://www.visa.ca/en_CA/support/small-business/interchange.html

https://www.cardfellow.com/blog/credit-card-processing-fees/

https://www.costcopaymentprocessing.ca/index.html

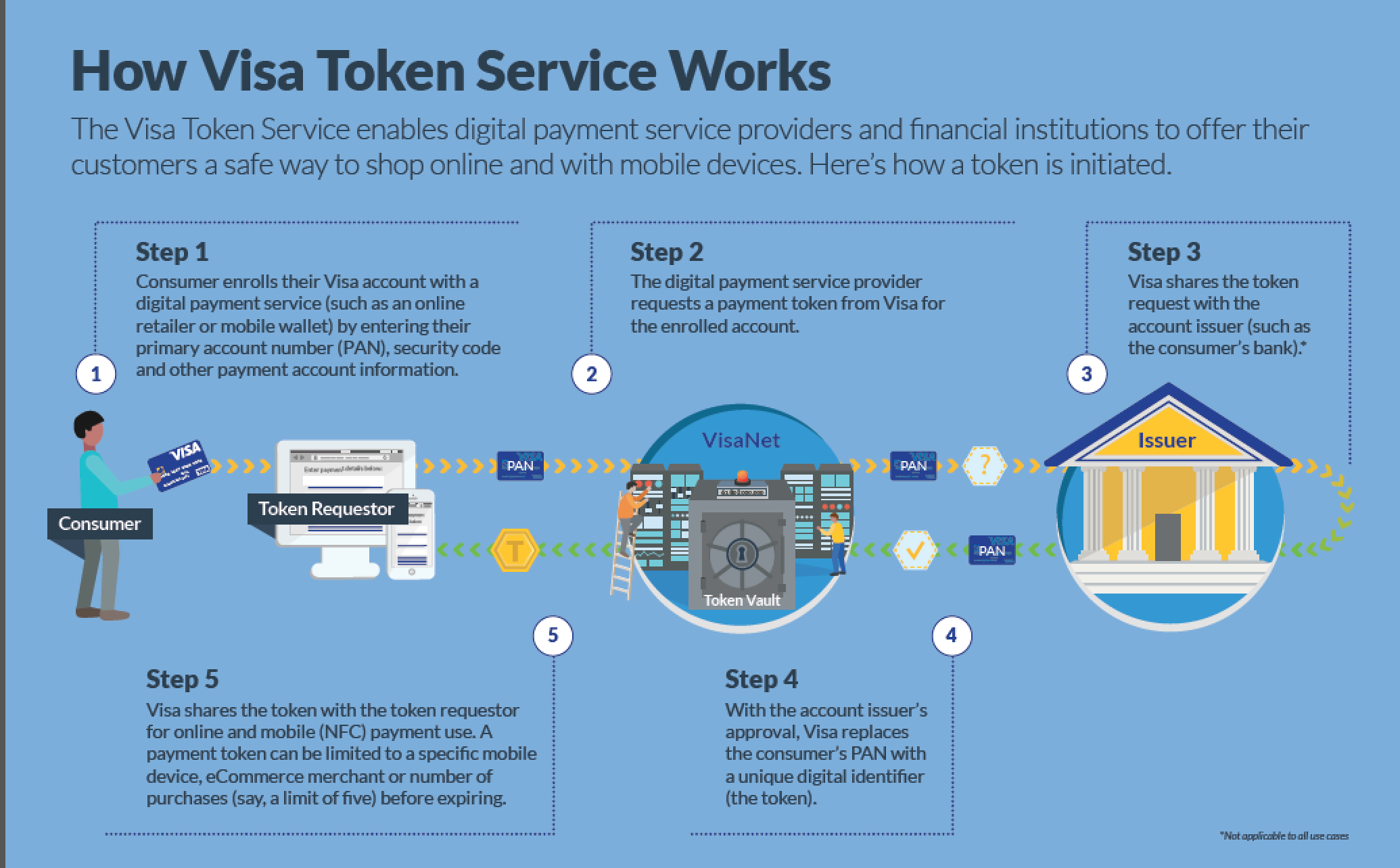

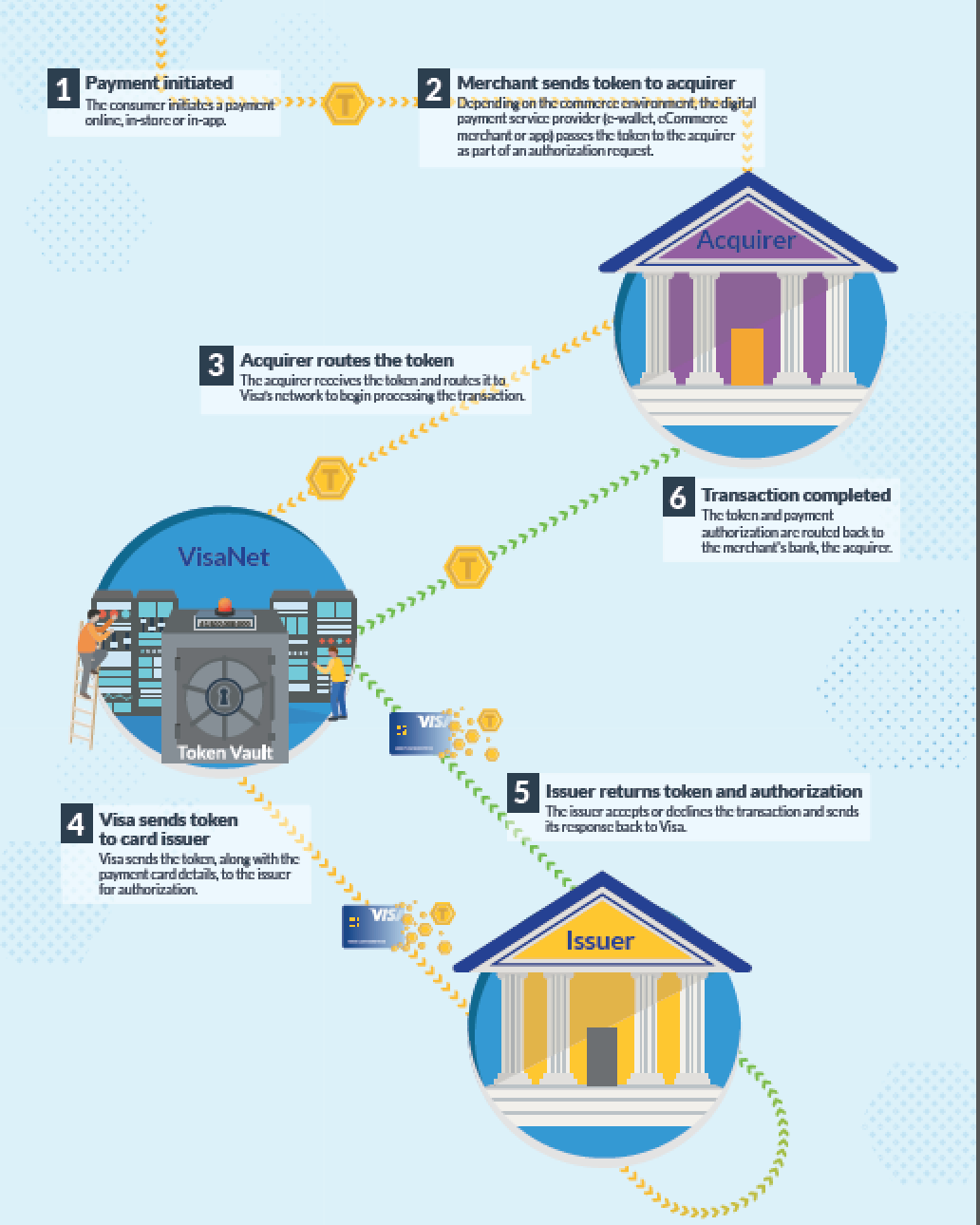

When you allow a merchant to store your credit card details on file, you must trust all these actors "not to mess up" ...

https://www.bhartipay.com/payment-tokenization-benefits

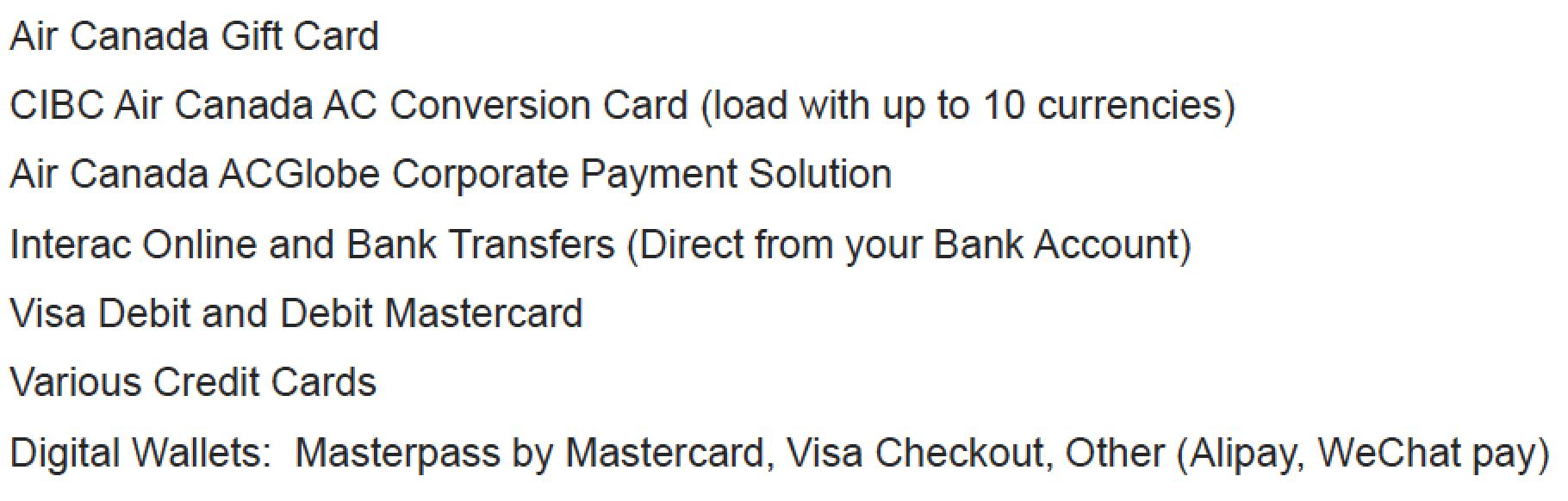

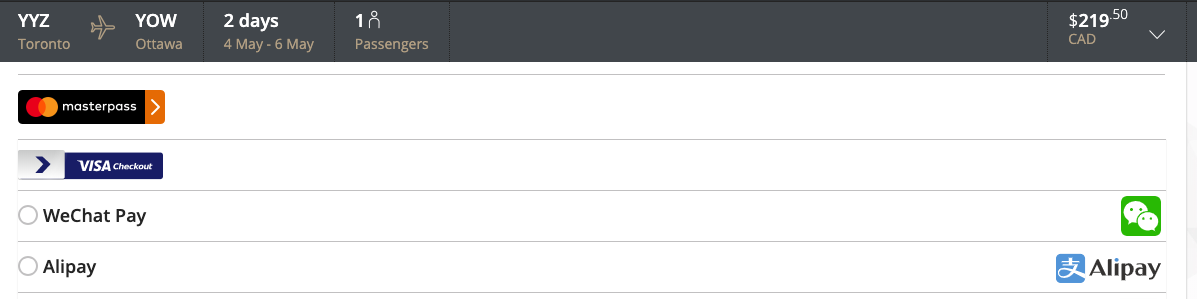

https://www.aircanada.com/ca/en/aco/home/book/payment-methods.html

80% of cocaine in the US

$14 billion in drug profits

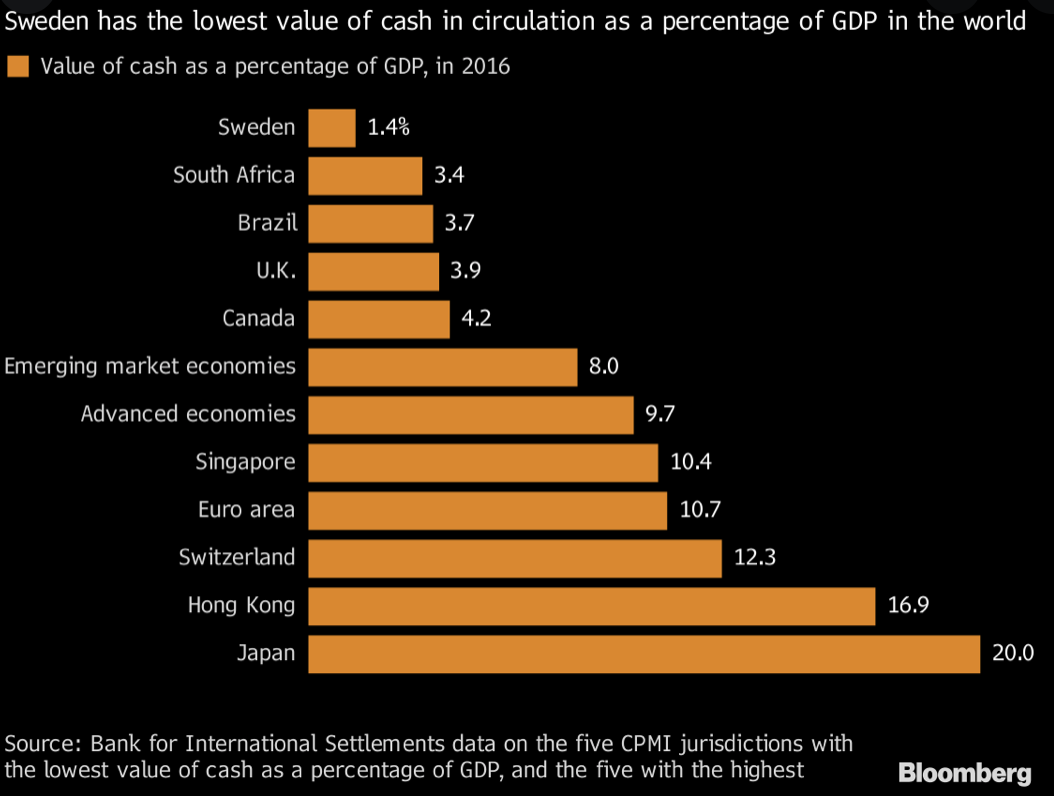

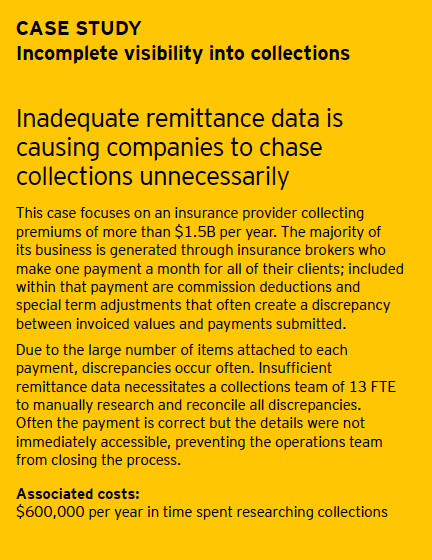

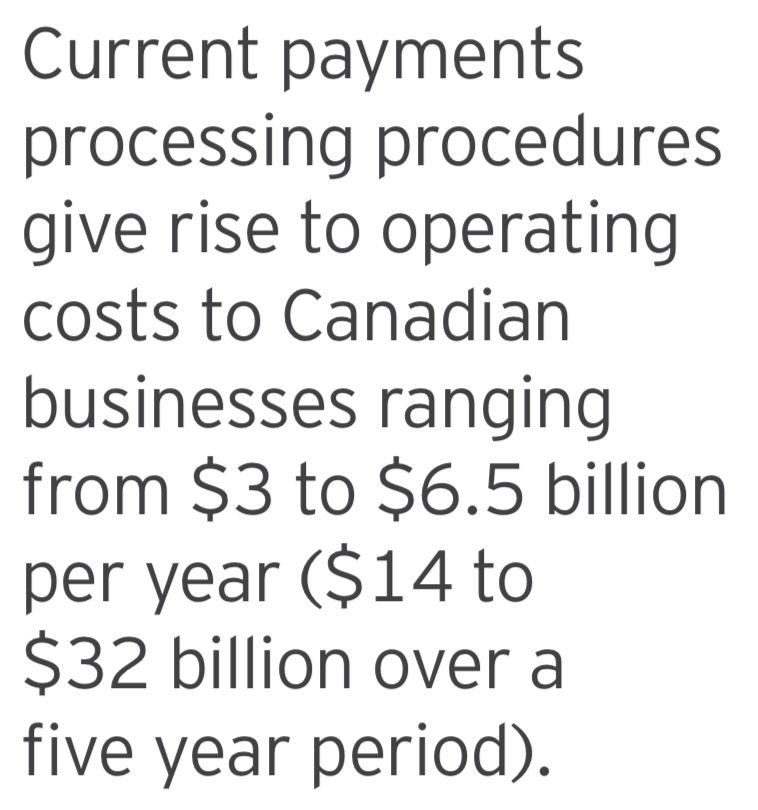

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

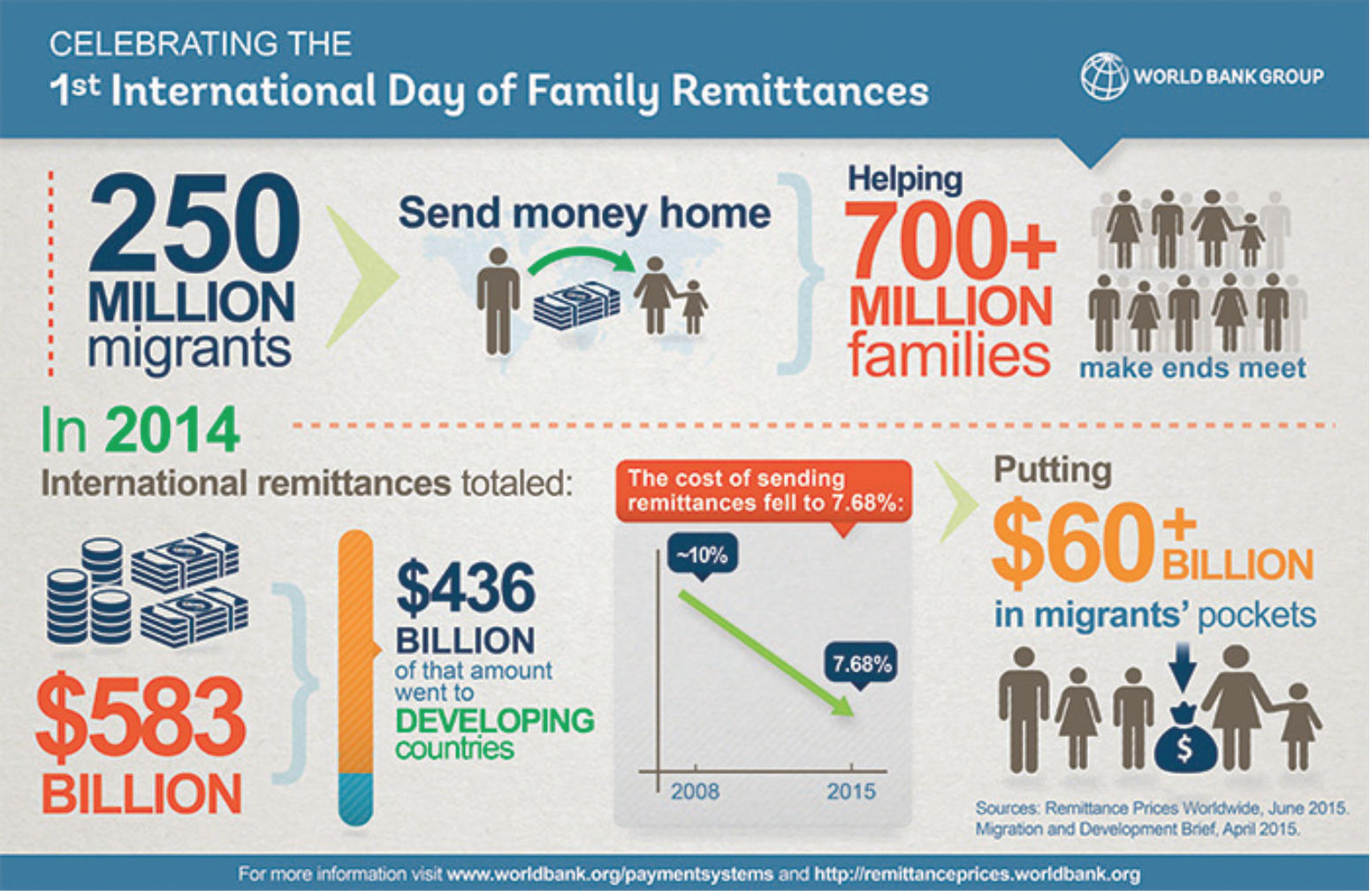

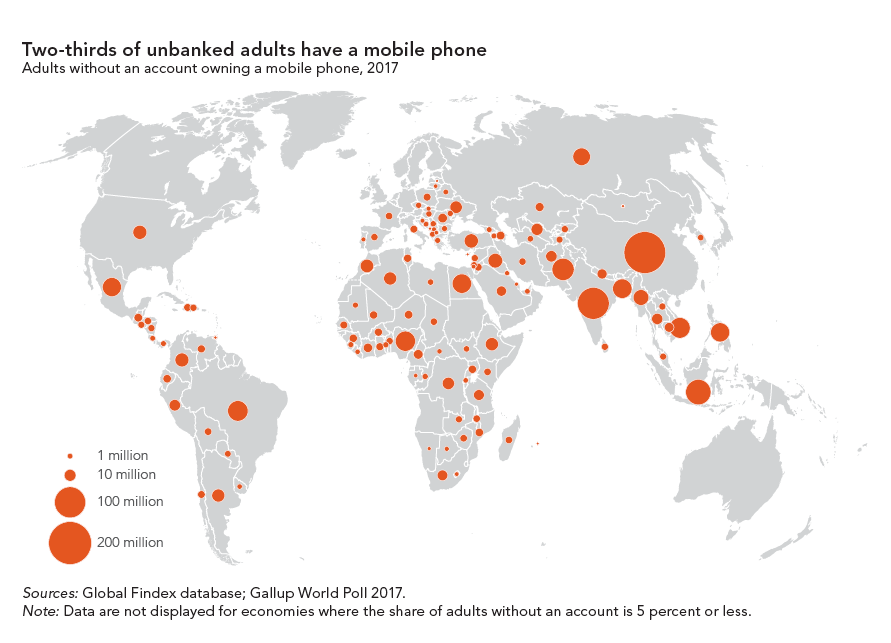

International remittances: $600B (U.S.) p.a.

all in: 10% fees

2015: 7.68% fees

2017: the total cost of sending remittances = $30 billion = total non-military foreign aid budget of the US!

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

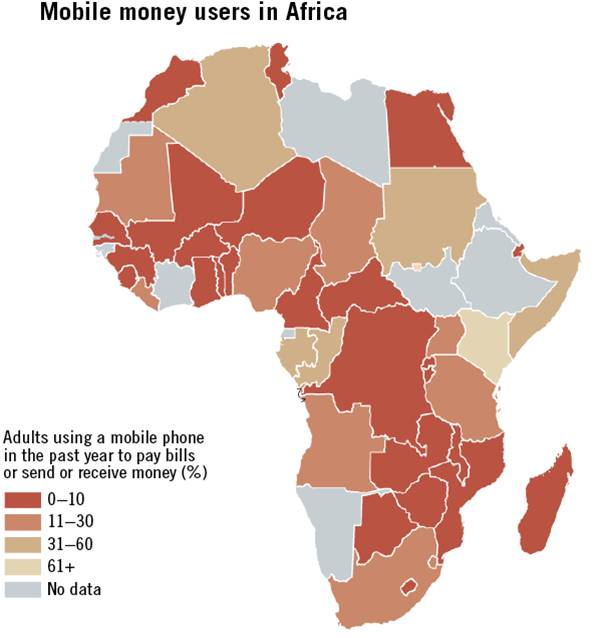

Cash-In

agent

Cash-Out

agent

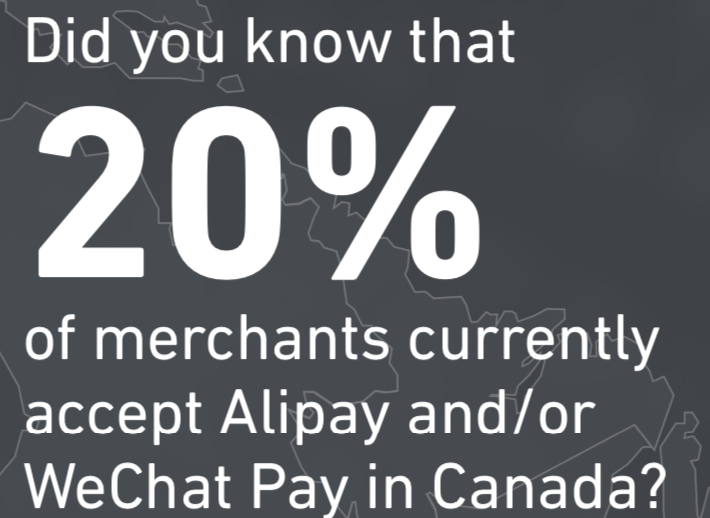

https://www.payments.ca/sites/default/files/canadianpaymentmethodsandtrendsreport_2019.pdf

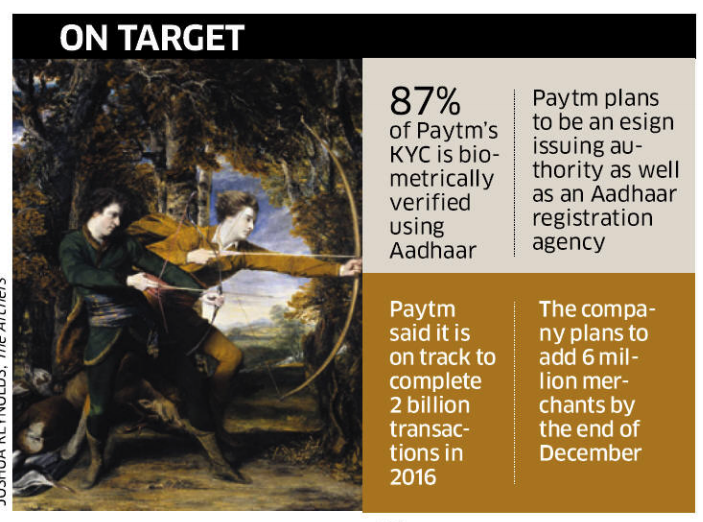

"To empower residents of India with a unique identity and a digital platform to authenticate anytime, anywhere."

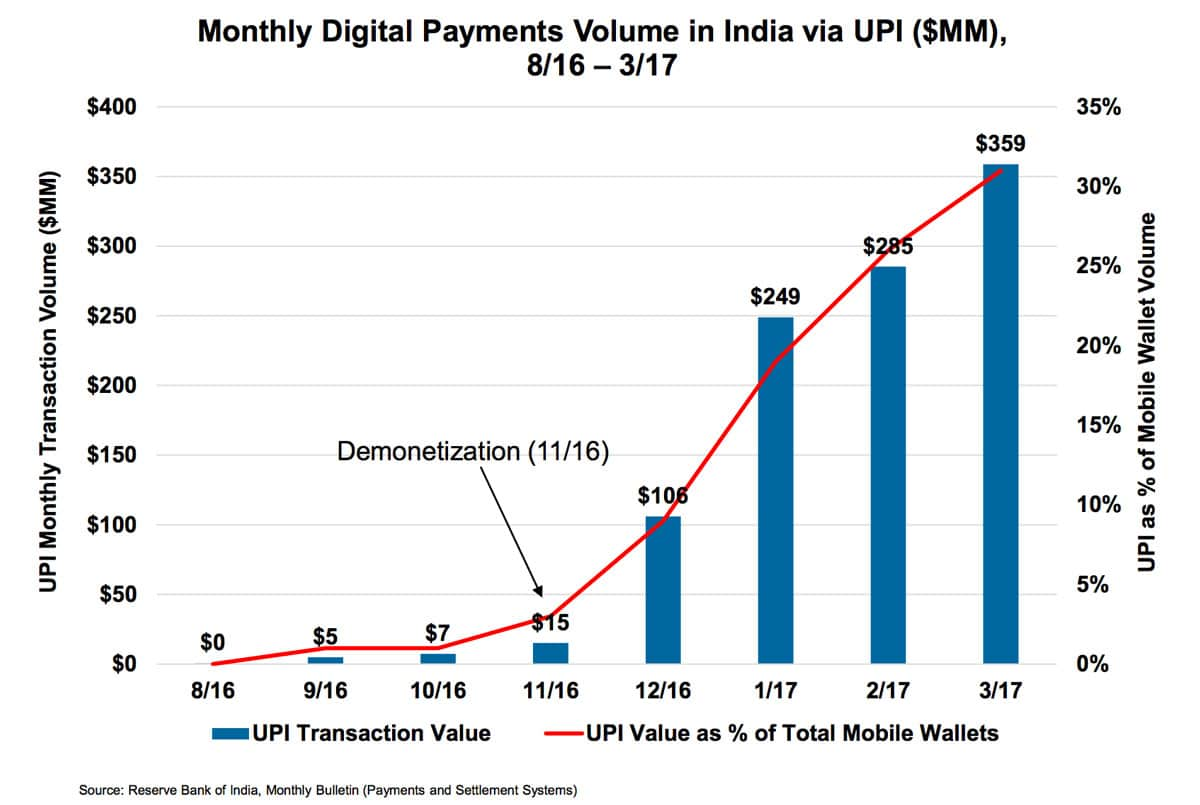

UPI puts multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments under one hood.

(Until just a over a week ago?), the largest money market fund in the world was ...

Remember our discussion on crypto-exchanges taking deposits .... ?

Chances are: they have ZERO interest in becoming a financial institution/bank

\(\rightarrow\) no expertise

\(\rightarrow\) competitive market

\(\rightarrow\) one of the most regulated business environments

They are trying to deal with frictions that impede their business

They aim to collect data which will vastly improve their business

How much money is coming into and out of the account each month

Spending habits: what you spend money on and where you spend it

Payment habits: Are you paying bills way ahead of deadline or tardy?

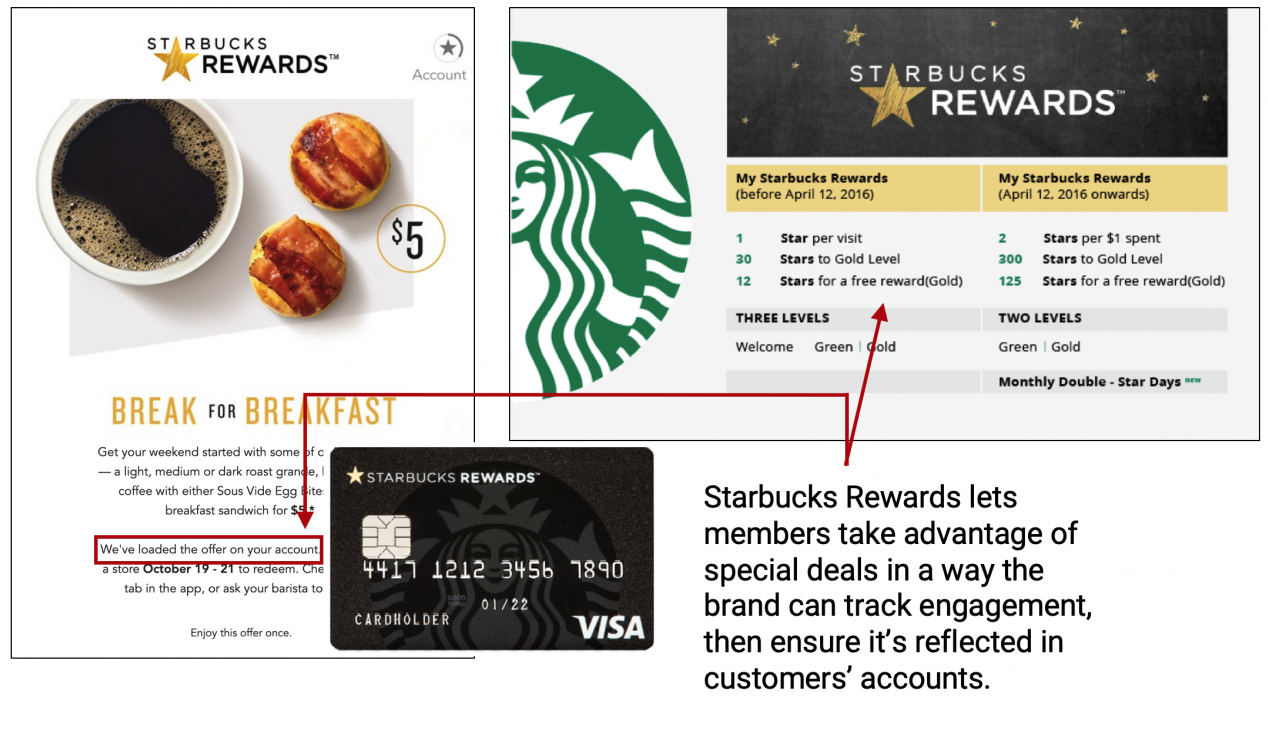

Loyalty rewards

is (mostly) not about rewarding loyalty.

It's DATA!

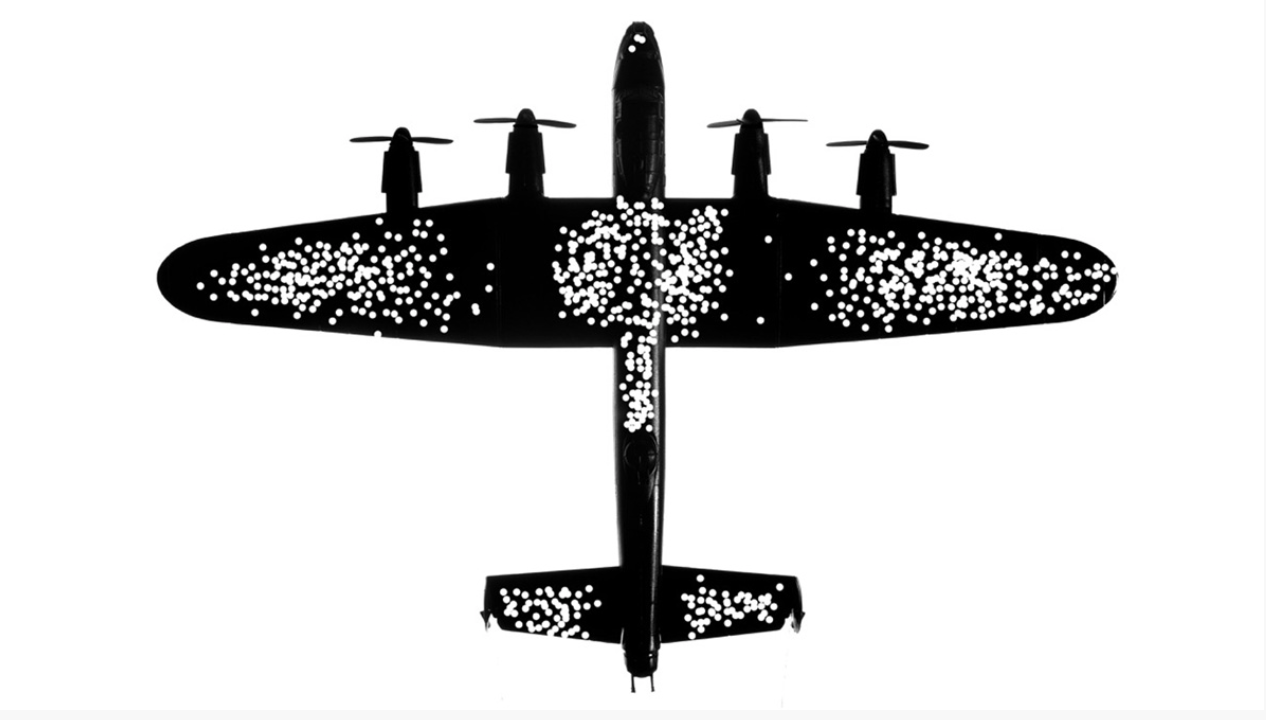

Abraham Wald: The armor should NOT go where the bullet holes are. It goes where the bullet holes aren’t!

Back during World War II, the RAF lost a lot of planes to German anti-aircraft fire. So they decided to armor them up. But where to put the armor?

Pilot programs with various tracking metrics and consequences for violations

By Katya Malinova

This is the second set of slides on payments for MBA F741