Sarah Dean PRO

asst prof in CS at Cornell

Lydia T. Liu, Sarah Dean, Esther Rolf, Max Simchowitz, and Moritz Hardt

University of California, Berkeley

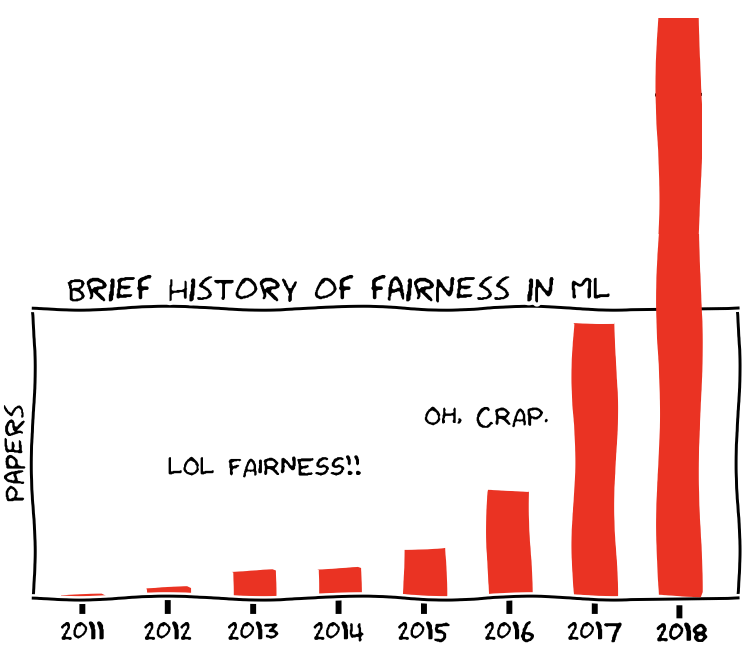

“21 definitions of fairness” [Narayanan 2018]

. . .

?

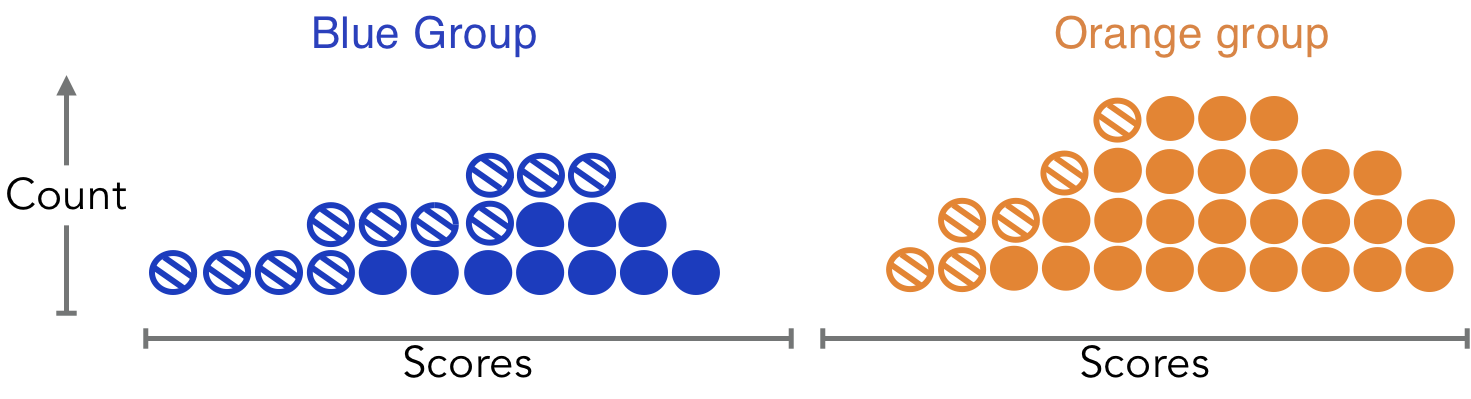

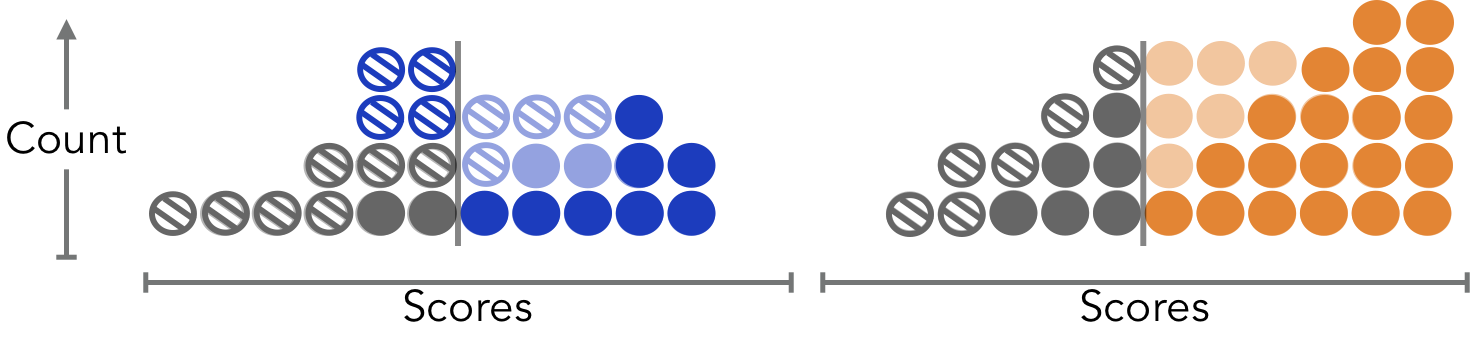

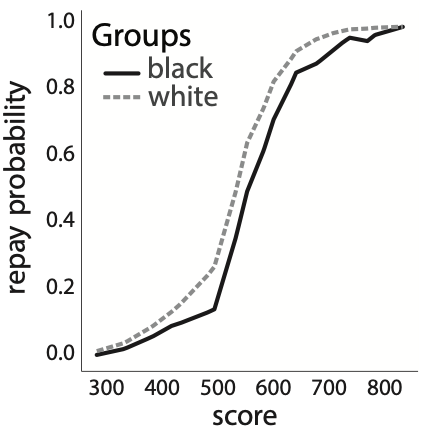

Two groups with different score distributions (e.g. credit scores)

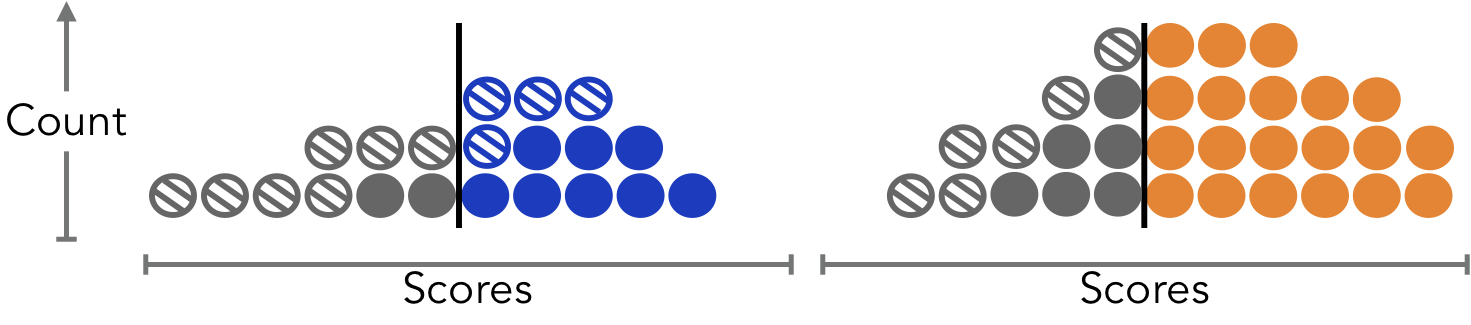

Approve loans according to Demographic Parity.

Credit scores change with repayment (+) or default (-).

Harm!

Fairness criteria didn’t seem to help the protected group,

once we considered the impact of loans on scores.

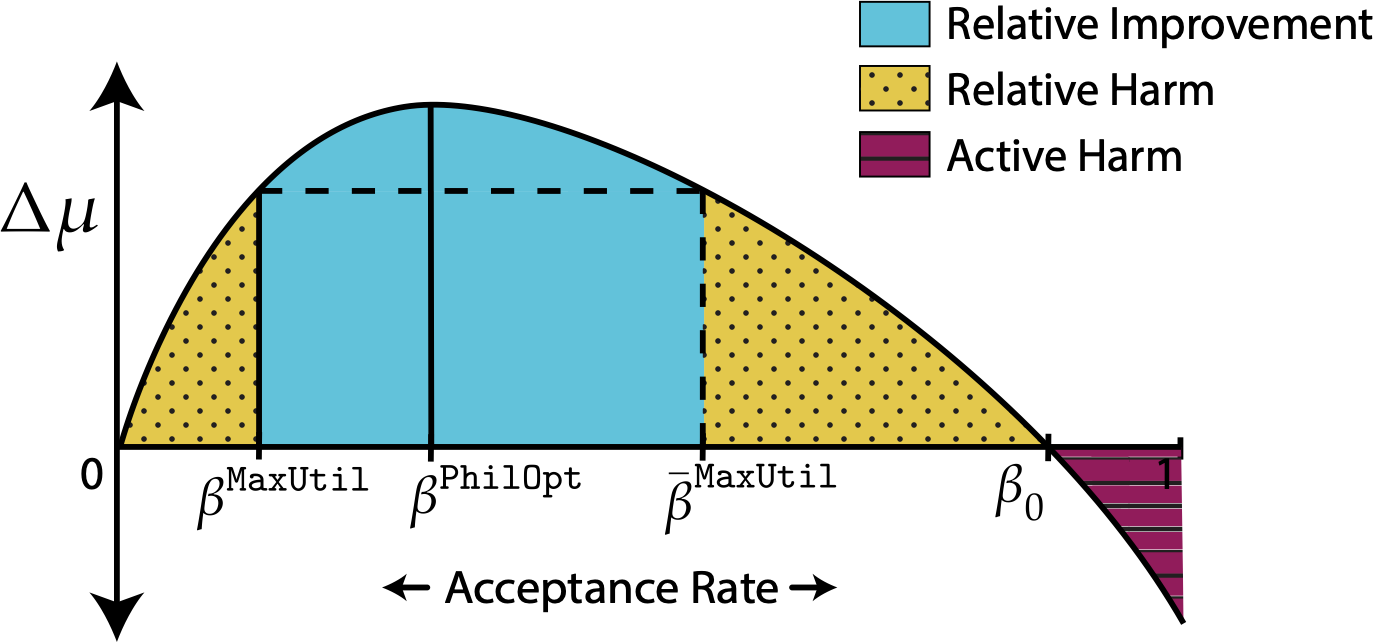

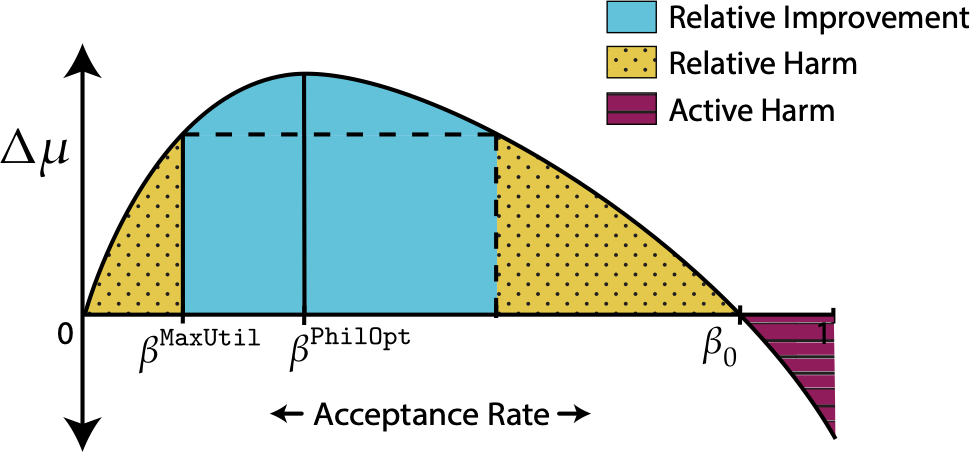

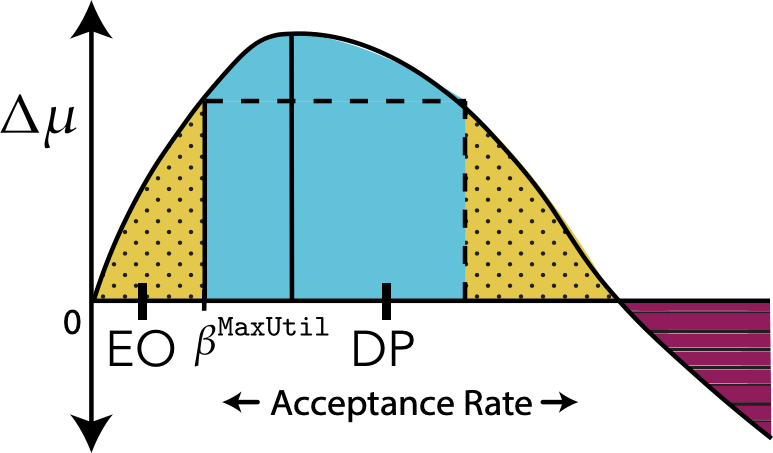

Lemma: \(\Delta\mu\) is a concave function of acceptance rate \(\beta\) under mild assumptions.

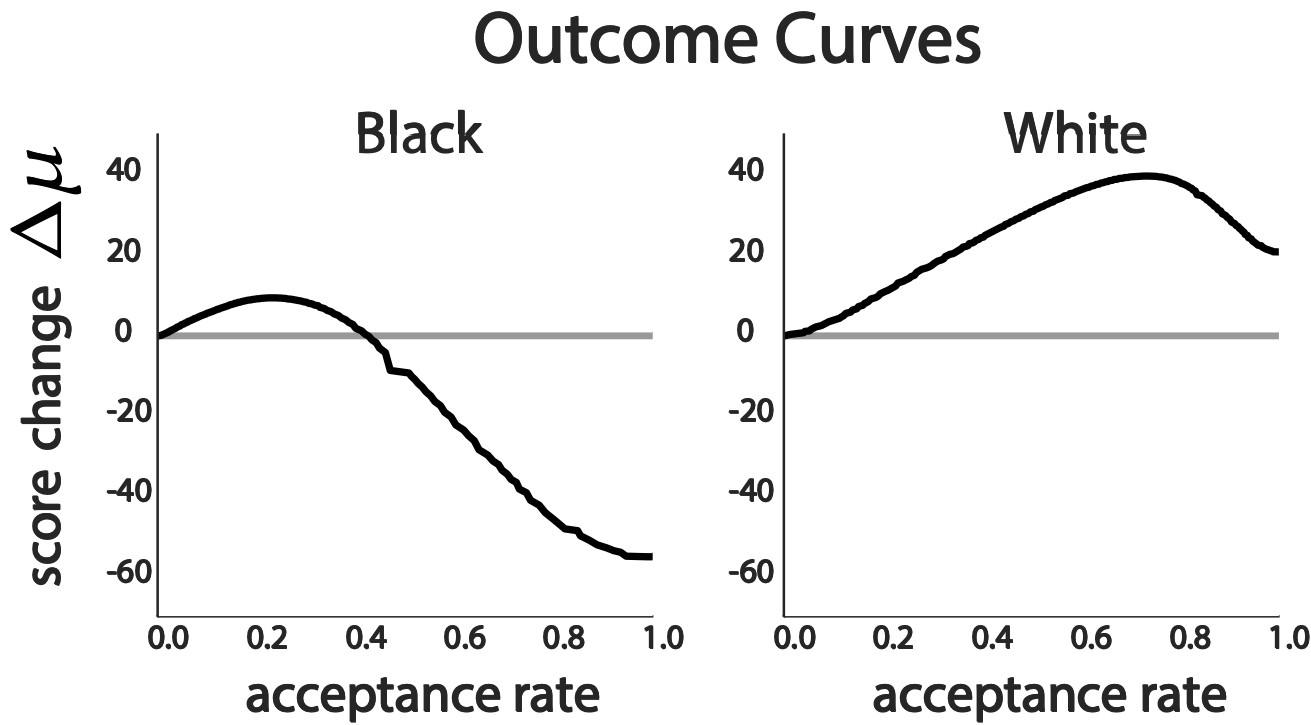

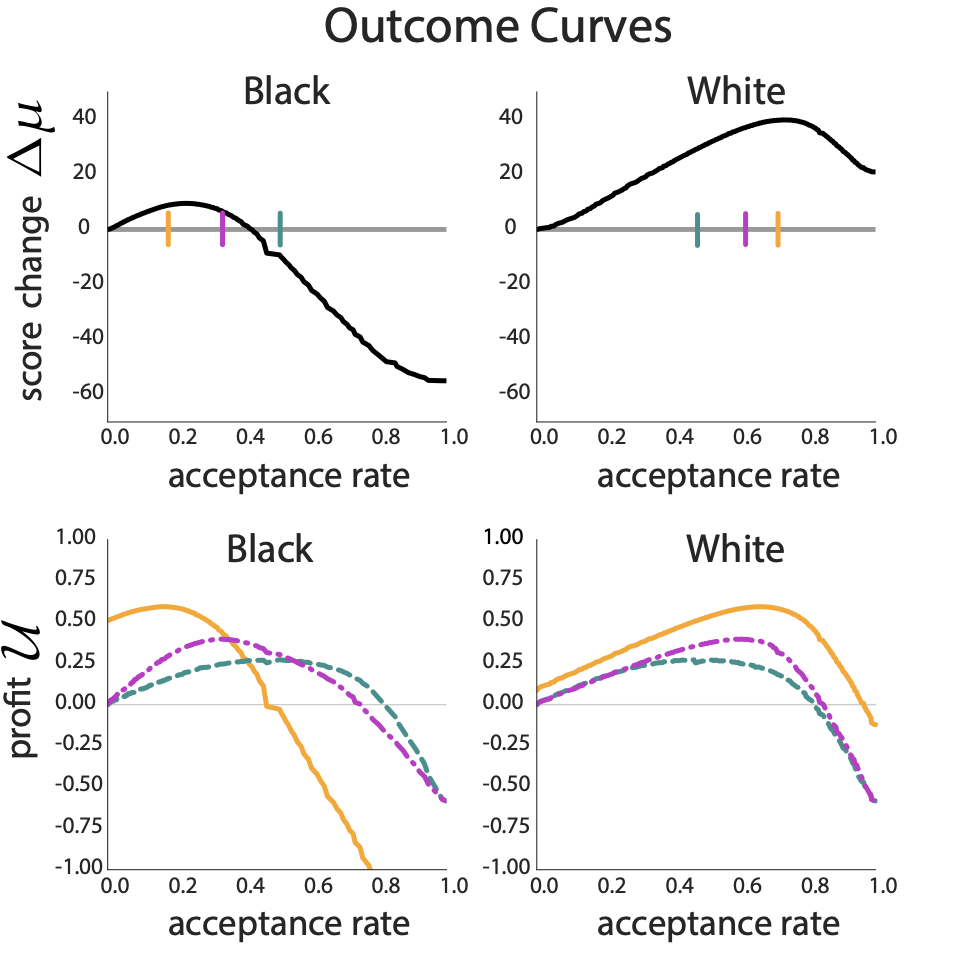

average score change

Alternative to unconstrained utility maximization

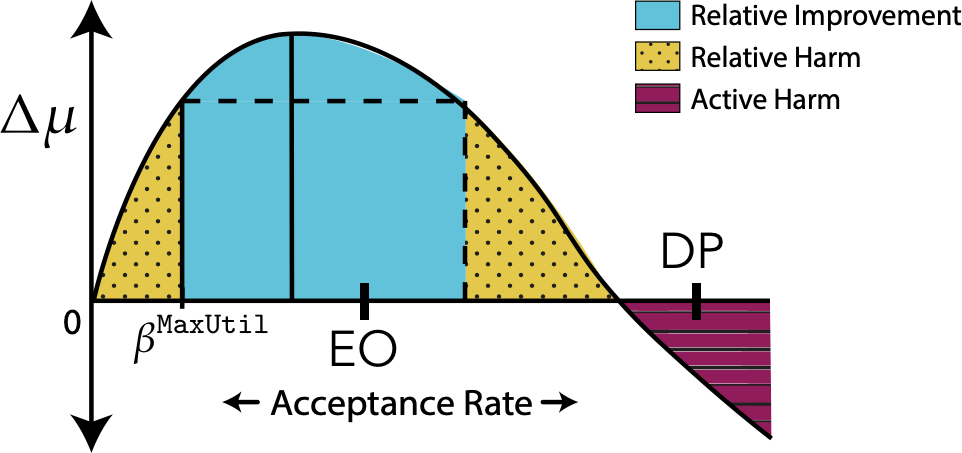

Demographic Parity: Equal Acceptance Rate

Equal Opportunity: Equal True Positive Rates

All outcome regimes are possible

Result 1

Equal opportunity and demographic parity may cause relative improvement, relative harm, or active harm.

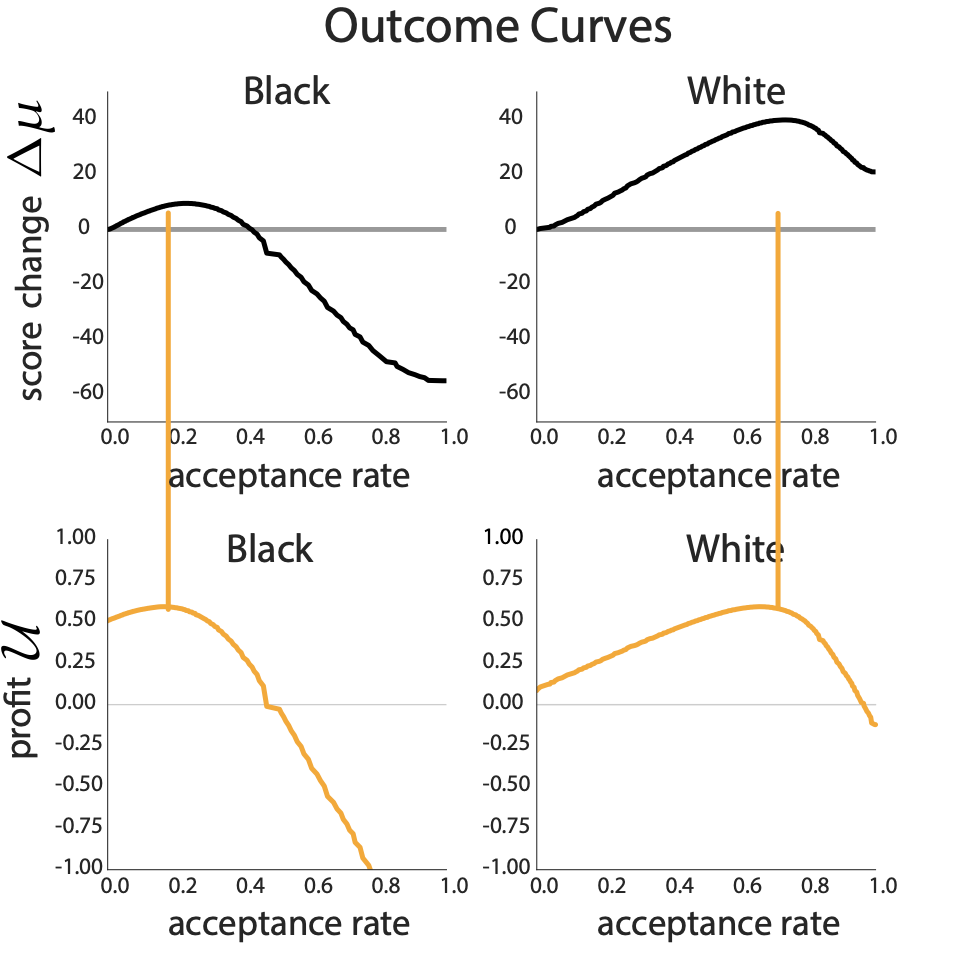

Unconstrained utility maximization never causes active harm.

Result 2

Demographic parity (DP) may cause active or relative harm by over-acceptance; equal opportunity (EO) doesn't.

Result 3

Equal opportunity may cause relative harm by under-acceptance; demographic parity never under-accepts.

Choice of Fairness Criteria Matters

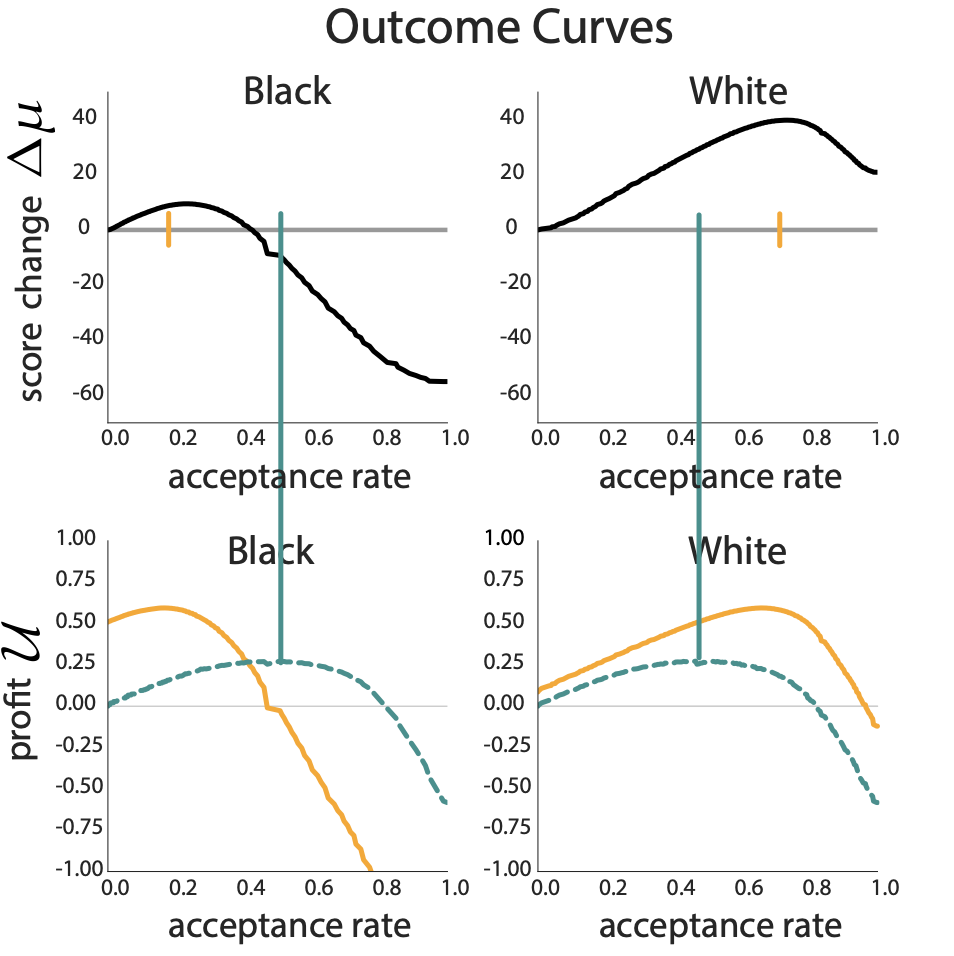

Experiments on FICO Credit Scores

Why the large difference in delayed impact?

Maxima of outcome and utility curves under fairness criteria are more misaligned in the minority black group

Details in full paper:

https://arxiv.org/abs/1803.04383

Algorithmic decisions are everywhere

\(\mathbb{E}[\mathrm{utility}|T] = \mathbb{E}[\mathrm{reward~from~repayments}|T] - \mathbb{E}[\mathrm{loss~from~defaults}|T]\)

\(R_\mathrm{new} = \begin{cases} R_\mathrm{old}+c_+ &\text{if repaid} \\ R_\mathrm{old}-c_- &\text{if defaulted} \end{cases}\)

\(\Delta \mu = \mathbb{E}[R_\mathrm{new}-R_\mathrm{old}]\)

Measurement Error Increases Potential for Improvement

Result 4

If scores are systematically underestimated in the protected group, then regime of relative improvement is widened

What we did

Experiments on FICO Credit Scores

By Sarah Dean