Andreas Park PRO

Professor of Finance at UofT

2018 American Economic Association Meeting in Philadelphia

Model Mechanism Review (simplified):

no blockchain = benchmark

Model with Blockchain and smart contract

Idea

Role of blockchain: escrow account that releases payment upon delivery confirmation

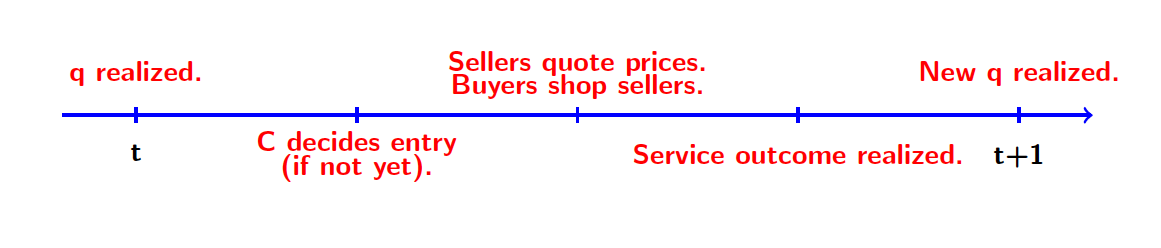

Model Mechanism Review (simplified):

with blockchain

Welfare Results (simplified):

with blockchain

Comment: What is the right benchmark?

But: there are other established market solutions!

Currently:

Why not:

Why important?

Comment: is entry vs collusion the key trade-off when thinking about blockchain-registered smart contracts?

Comment 1: Key question reg. smart contracts in this setting is/should be the trade-off that non-intermediated decentralized interactions bring.

Model Ingredient Review (simplified): product market

what are the buyers' decision rules?

what's the role of qualities? why needed?

how do I interpret this in finance?

for most of the paper: truthful verification

Model Ingredient Review (simplified): verifiers

Comment 2 (part 1): the main results in the paper don't use the verifier and instead assume perfect revelation.

Review of model extensions

Comment 2 (part 2): These results have an appendix-like/robustness-check feel. Why not simplify the model and shift all the complex material to an online appendix?

Comment 3: Does the paper address a question on blockchain design question? If so, organize the paper as such.

Summary Main Comments

By Andreas Park

My discussion of Cong and He "Blockchain Disruption and Smart Contracts" at the 2018 AEA meeting.