Andreas Park PRO

Professor of Finance at UofT

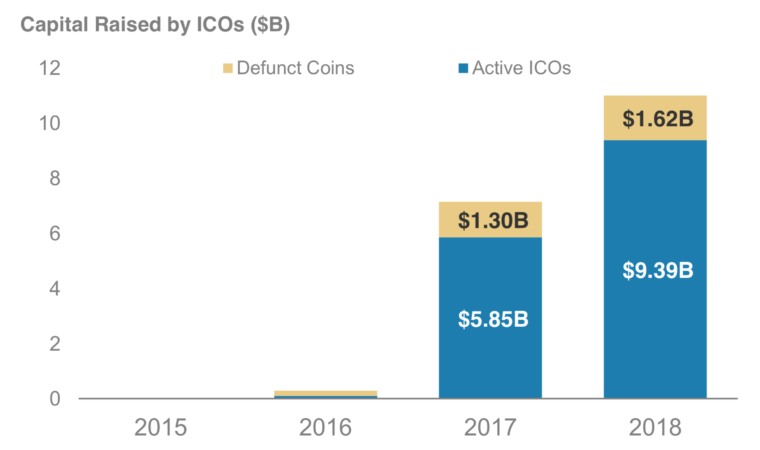

Data: coinschedule

for comparison: total size of

Toronto Stock Exchange: $2,200B

Toronto Venture Exchange: $41B

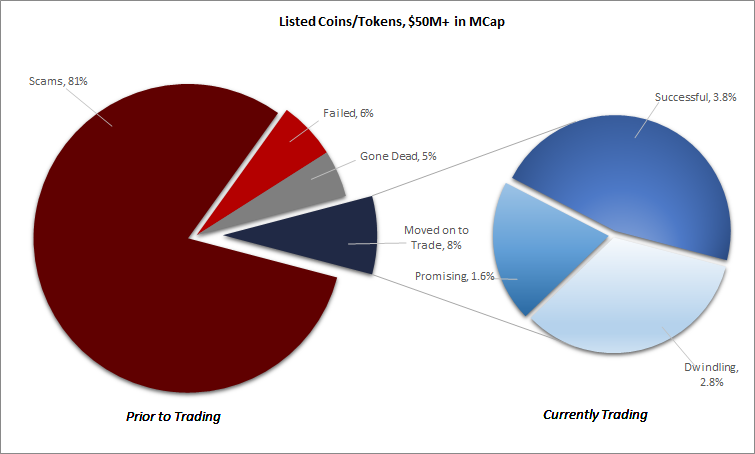

Source: Tokendata

native to a blockchain for payment

examples: Bitcoin, Bitcoin Cash, Ether, Lumens, Cardano

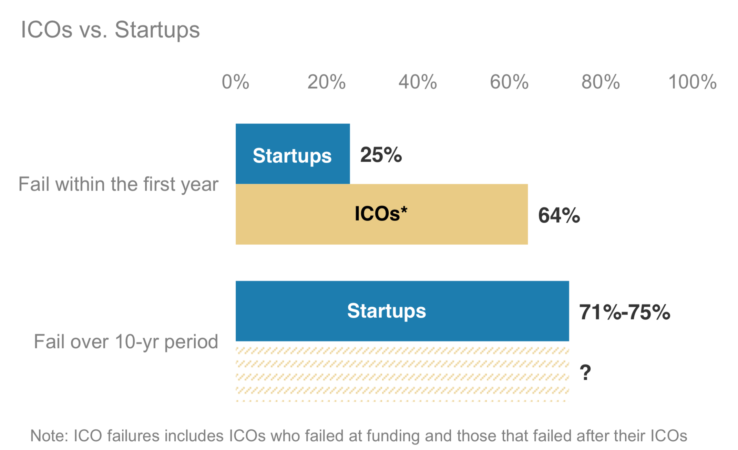

Source: Satis Group LLC

Source: Morgan Stanley (Nov 2018) “Update: Bitcoin, Cryptocurrencies and Blockchain”

Source: Tokendata

price

demand

marginal cost

marginal revenue

general idea: sell future output

two approaches for token sales

price

demand

marginal cost

marginal revenue

\(\Rightarrow\) shifts marginal revenue for entrepreneuer left because get only fraction of revenue

Result: underproduction

NB: Chod and Lyandres (2018) have the same result

price

demand

marginal cost

marginal revenue

Entrepreneur does not internalize that extra output unit affects revenue for tokenholders!

Result: overproduction

\(c\)

\(MR\)

general idea: sell future output

two approaches for token sales

Common result in the literature: only debt guarantees effort

Idea: entrepreneur can influence expected demand with "effort"

effort is costly

Is it worth it for the entrepreneur?

Optimal contract looks like debt:

Feb 2000

Aug 2014

blockchain only useful with applications

applications require (tech + economics) + business

understanding of economics on blockchain requires development

our paper: \(\exists\) real economic value in tokens, when used properly

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

By Andreas Park

I used this deck for a presentation for the Osgoode Certificate in Blockchains, Smart Contracts, and the Law.