Andreas Park PRO

Professor of Finance at UofT

paper by Chen, Foley, Goldstein, and Ruf

discussion by Andreas Park

Who benefits from a speed bump on marketable orders that provides a speed advantage to some limit orders?

The famous case: IEX's Speed Bump

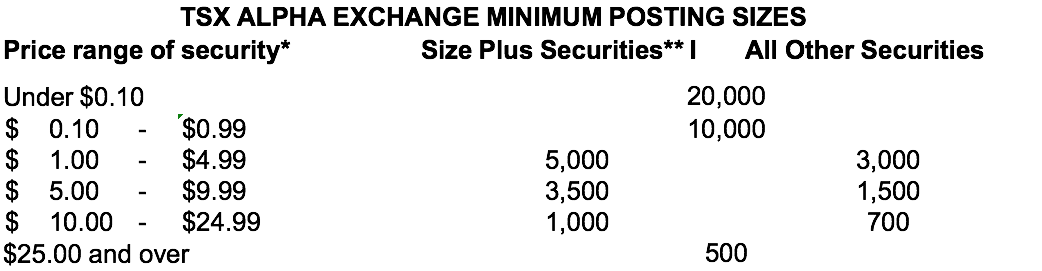

Here: TSX Alpha Exchange

market event

expect market orders

200 shares

100 shares

500 shares

before

at the ask

market event

expect market orders

200 shares

100 shares

500 shares

after

cancels

1 event = 4 changes

| Price level | retail | non-retail |

|---|---|---|

| $1-$5 | 1,486 | 697 |

| $5-$10 | 791 | 413 |

| $10-$25 | 422 | 266 |

| >$25 | 275 | 203 |

average volume for single-market marketable orders

| Price level | retail | non-retail | %retail | minimum size Alpha |

|---|---|---|---|---|

| $1-$5 | 5,100 | 5,797 | 26% | 5,000 |

| $5-$10 | 2,134 | 2,378 | 17% | 3,500 |

| $10-$25 | 1,032 | 1,128 | 27% | 1,000 |

| >$25 | 664 | 719 | 17% | 500 |

average volume for multi-market marketable orders

=> retail trades are neither small nor trade on only one market

HANDLE WITH CARE: "retail orders, on average, are unlikely to need to execute quantities larger than the 5 board lot minimum Alpha enforces"

overall I like many of the results, and I believe that they make intuitive sense, but I think the construction of measures requires work

overall I like many of the results, and I believe that they make intuitive sense, but I think the construction of measures requires work

| Broker | %Vol |

|---|---|

| Anonymous | 24% |

| CIBC | 13% |

| TD | 11% |

| RBC | 9% |

| BMO | 5% |

| Scotia | 5% |

| National Bank | 4% |

| Merrill | 4% |

| Instinet | 2% |

| Morgan Stanley | 2% |

Source: RBC Marketstructure Guidebook Jan 2016

Who are the retail brokers? RBC & TD?

my view: take with huge grain of salt due to the many simultaneous changes

By Andreas Park

This is a discussion of Chen, Foley, Goldstein, Ruf's paper on "The Value of a Millisecond..."