Danielle Navarro

I am a computational cognitive scientist at the University of New South Wales. My research focuses on human concept learning, reasoning and decision making.

11 June 2018, ALG meeting, Katoomba

Products don't stay on sale forever

Possible romantic partners move on

Houses go off the market

Images via pixabay

Images via pixabay

RSVP now to attend party later

Study now for a career later

Show up to the first date to get invited on a second

Images via unsplash

Pursuing too many options consumes time, effort and other scarce resources

The opportunity cost for maintaining poor options can be substantial

Yet... pursuing too few is risky... What if the world changes? What if your needs change?

"doors" problems

image source: flaticon

M1

M2

M3

M4

lose $5

win $2

lose $1

lose $1

win $2

lose $3

I've not used these machines recently, and someone else has taken them

I've concentrated recent bets on these machines

win $2

win $2

lose $5

1

2

3

4

5

6

7

8

chosen

viable option not chosen

someone takes the machine

someone takes the machine

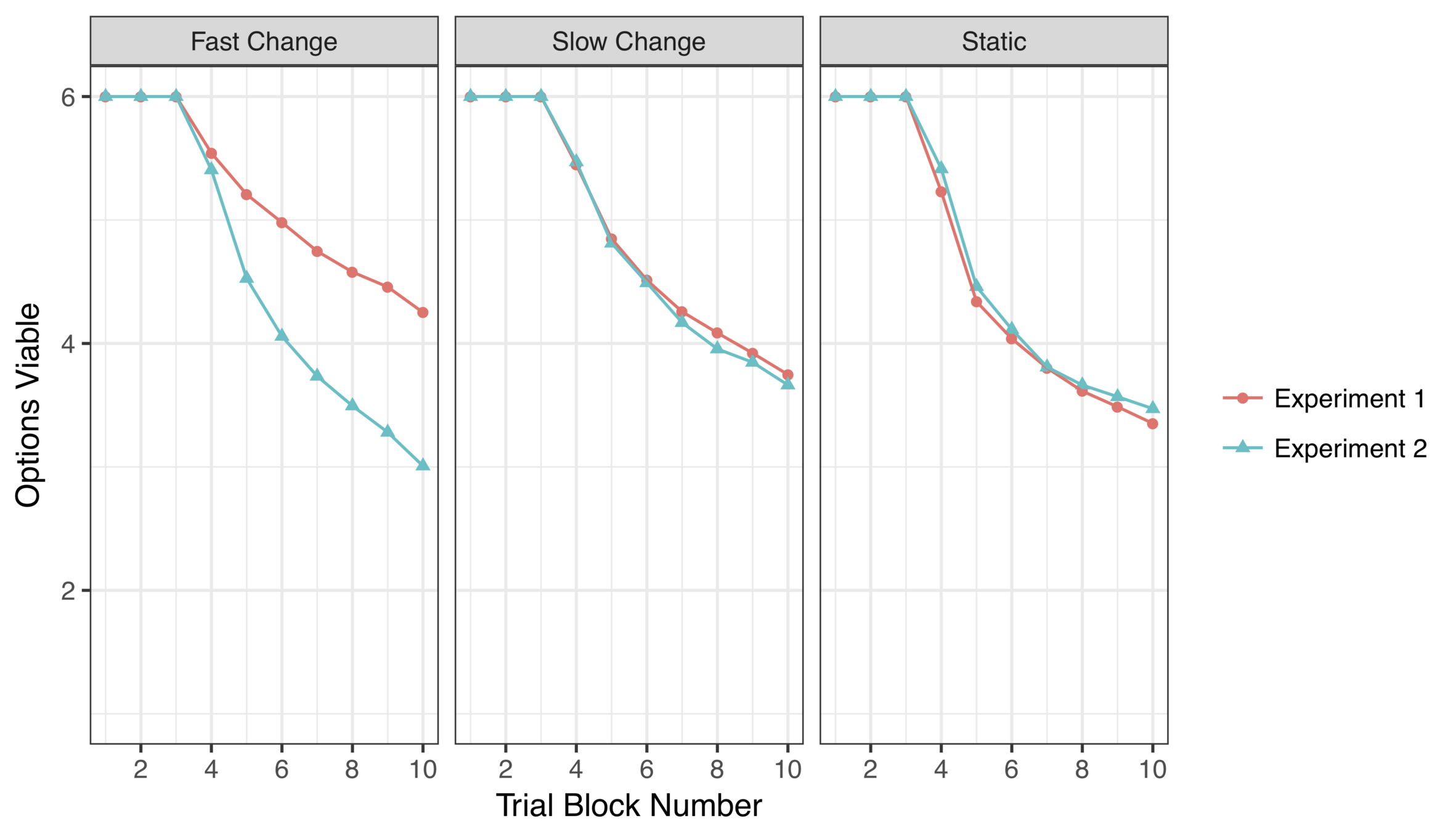

~ 3-4 options retained

(consistent with Ejova et al 2009)

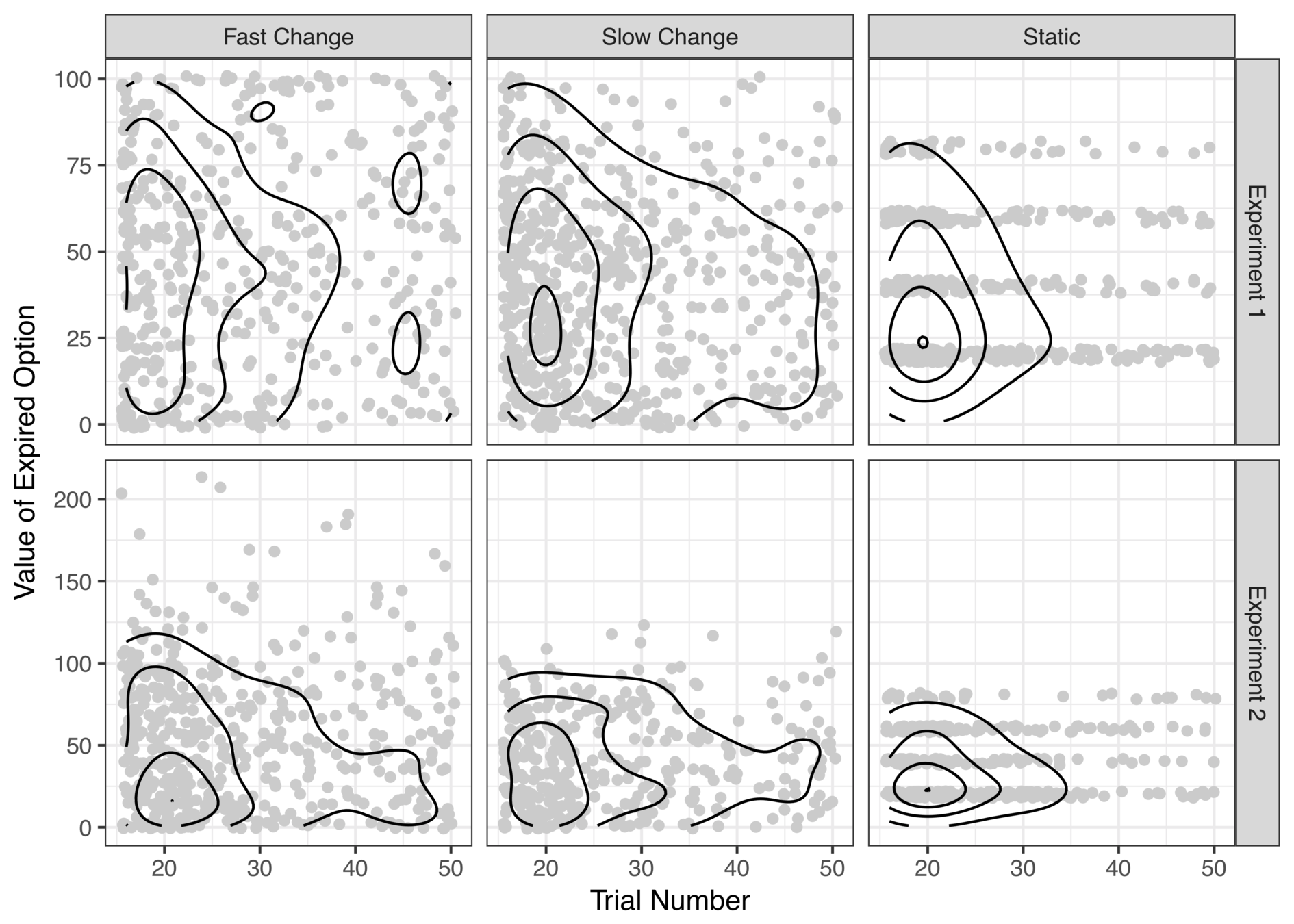

(an unapologetically exploratory analysis!)

early expired options almost always low value

early expired options sometimes high value

Looks like people are "clinging" to a few suboptimal options only to let them expire right before the deadline?

Expected reward for option \(j\) on this trial

Uncertainty about reward for option \(j\) on this trial

Expected reward for option \(j\) on last trial

Uncertainty about reward for option \(j\) on last trial

Uncertainty drives Kalman gain

Kalman gain influences beliefs about expected reward and uncertainty

Predicted reward for choosing the option

Prediction error

(only update chosen option)

Amount of learning depends on the Kalman gain

KF updates uncertainty

Gain depends on uncertainty

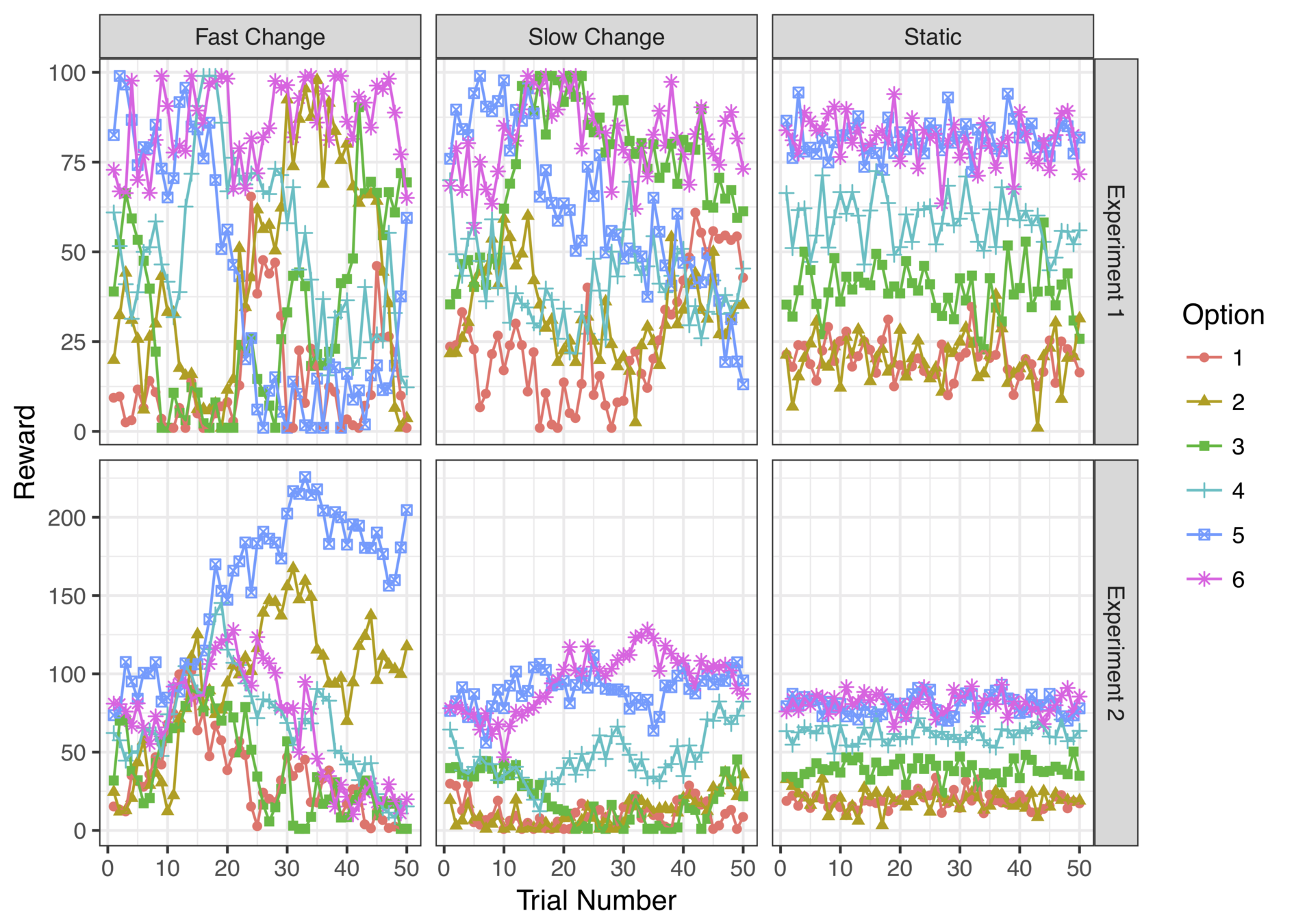

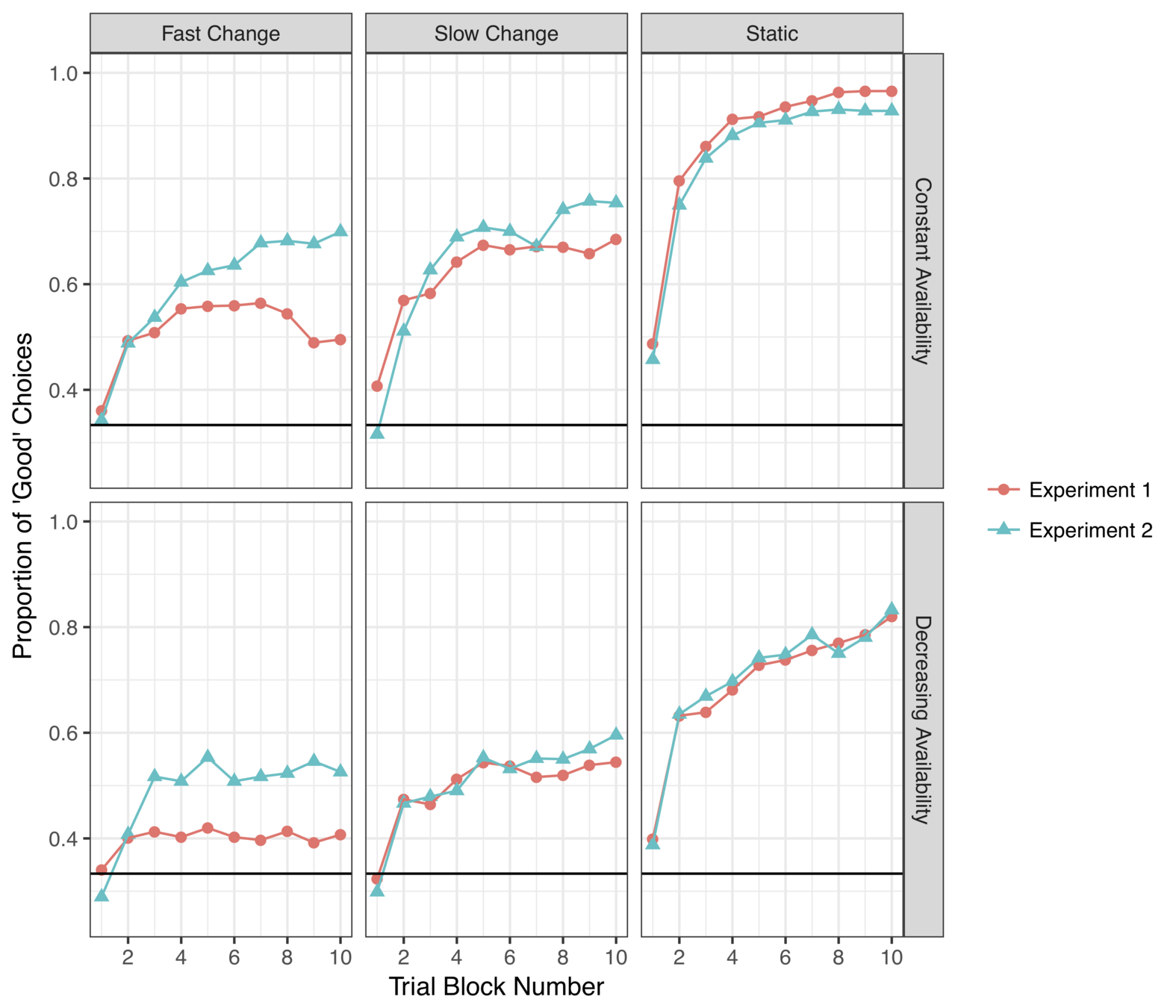

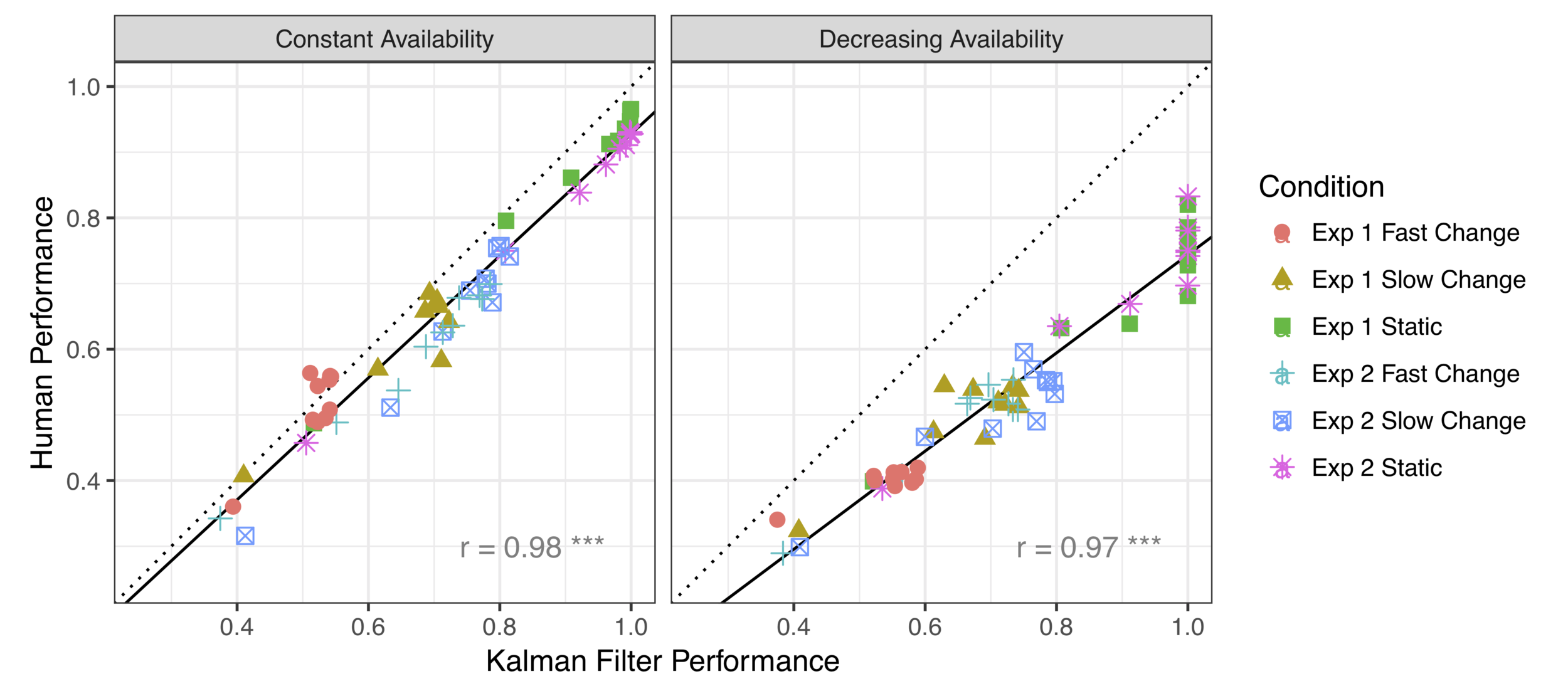

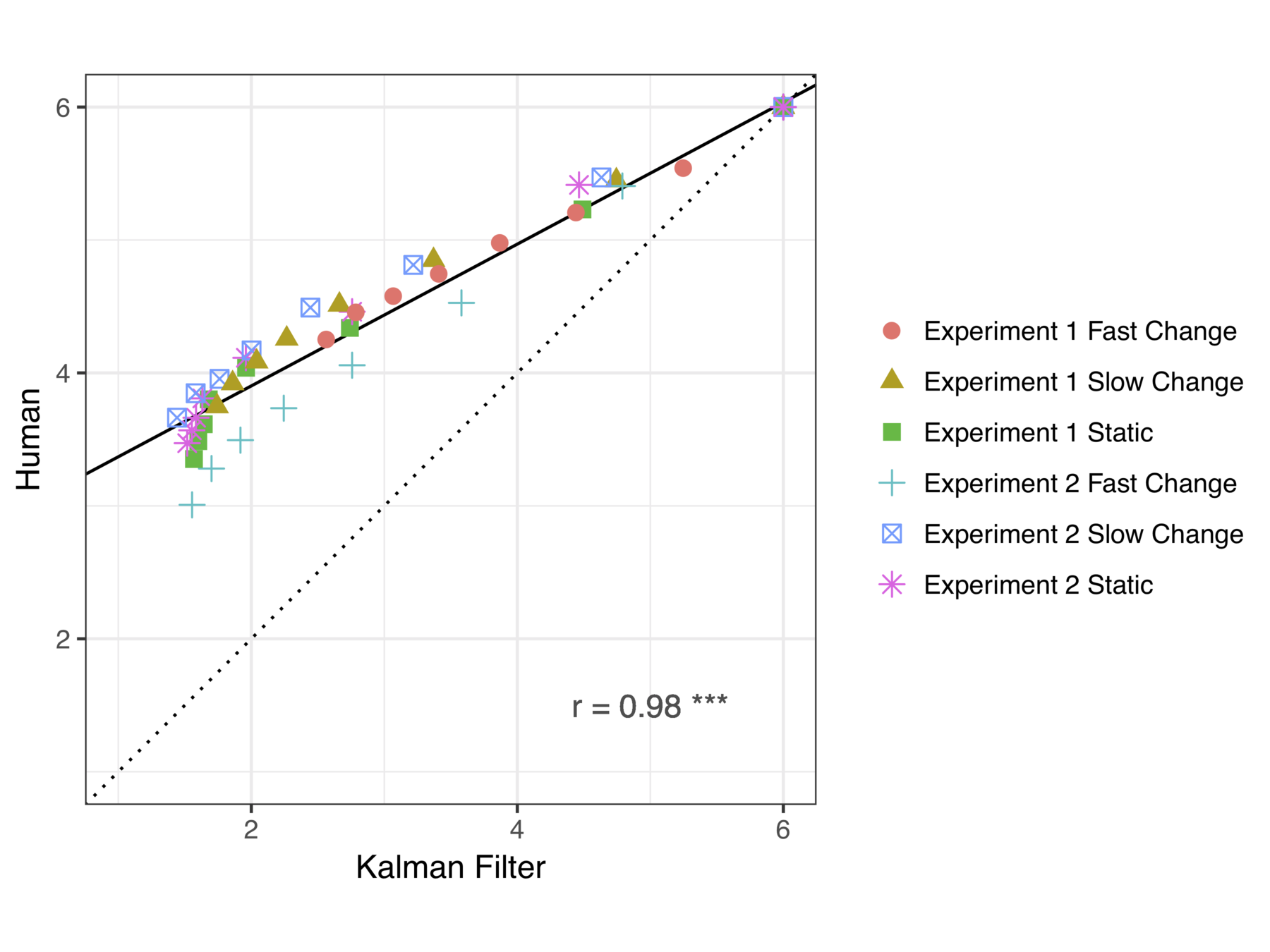

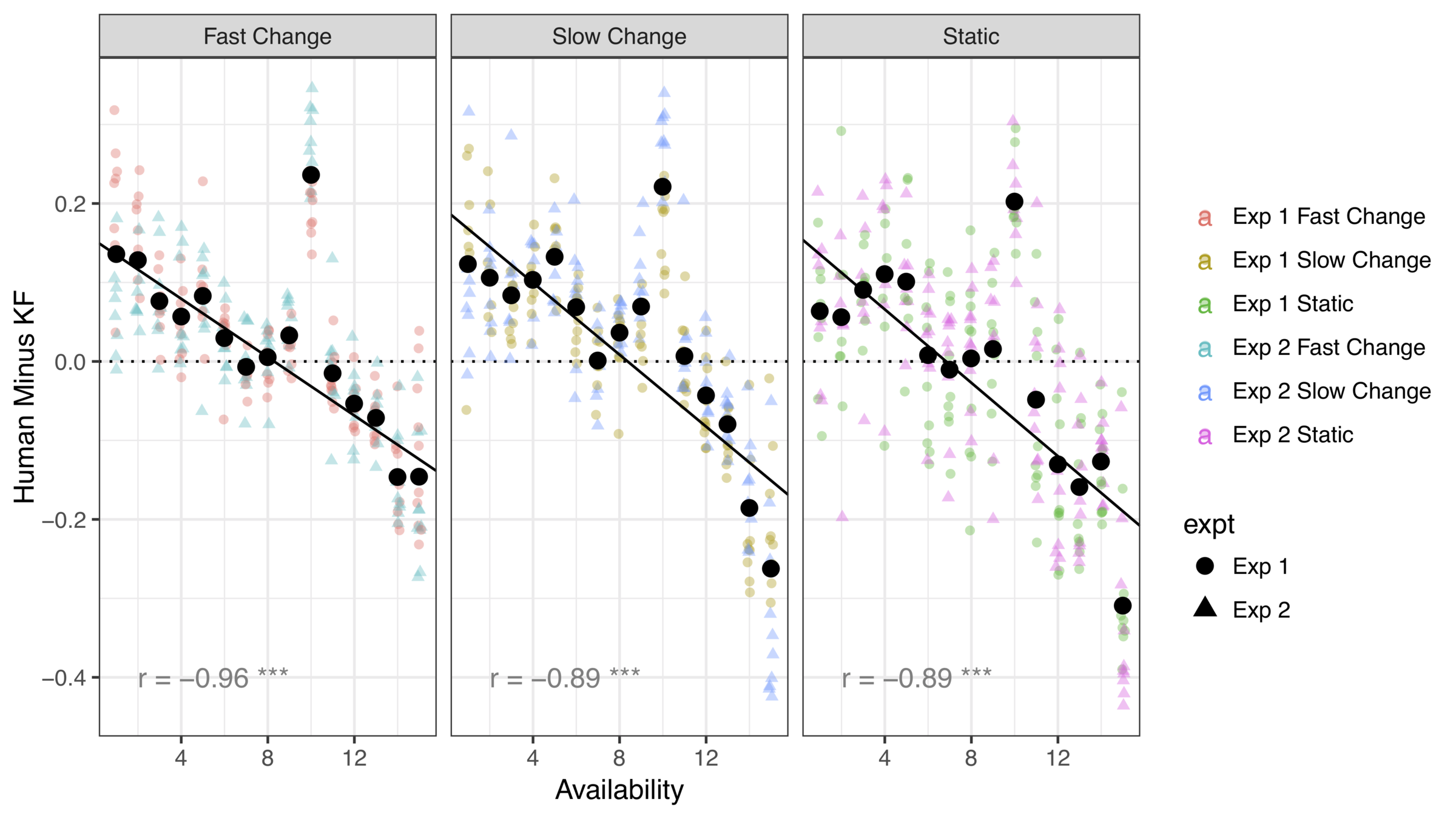

KF model provides an excellent account of choice behaviour when options do not expire

There is a systematic difference when option loss is a possibility

Human decision makers retain more options than the KF model

Project:

Support:

By Danielle Navarro

We present two experiments using multi- armed bandit tasks in both static and dynamic environments, in situations where options can become unviable and vanish if they are not pursued. A Kalman filter model provides an excellent account of human learning in a standard restless bandit task, but there are systematic departures in the vanishing bandit task. (Talk for the 2018 mid-year meeting of the Australian Learning Group. Preprint: https://psyarxiv.com/3g4p5/https://psyarxiv.com/3g4p5/