Economic Data Sciences PRO

Understandable A.I.

Understandable Artificial Intelligence

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

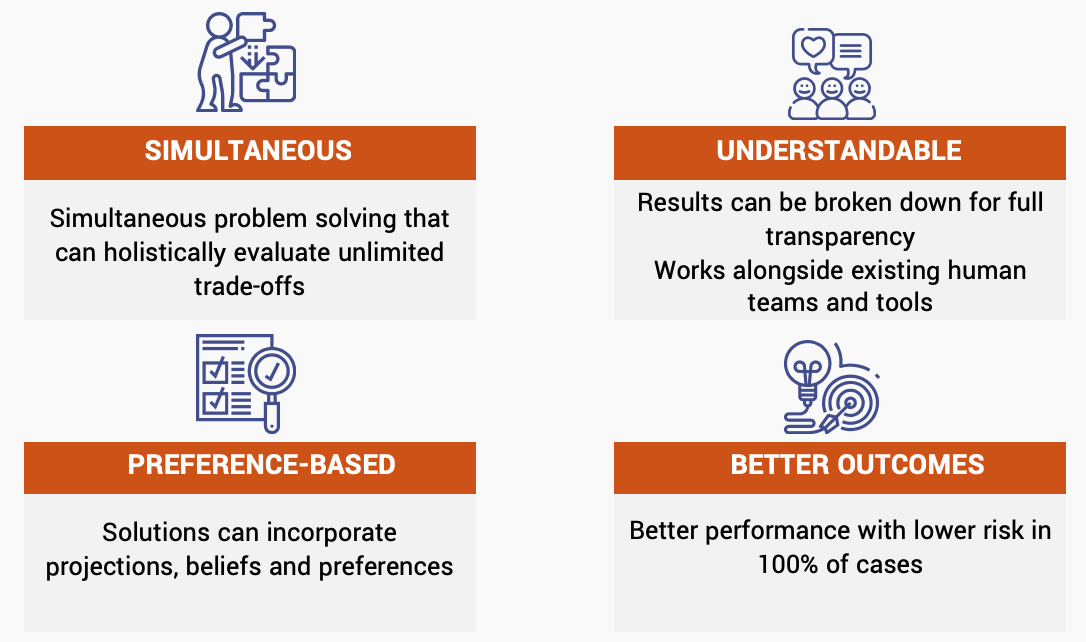

It has a unique ability to make improvements by searching across every known factor to get the best from existing best-practices

56% of institutional investors plan to increase integration of A.I.*

A.I. is best used when combined with humans

©2019 Economic Data Sciences

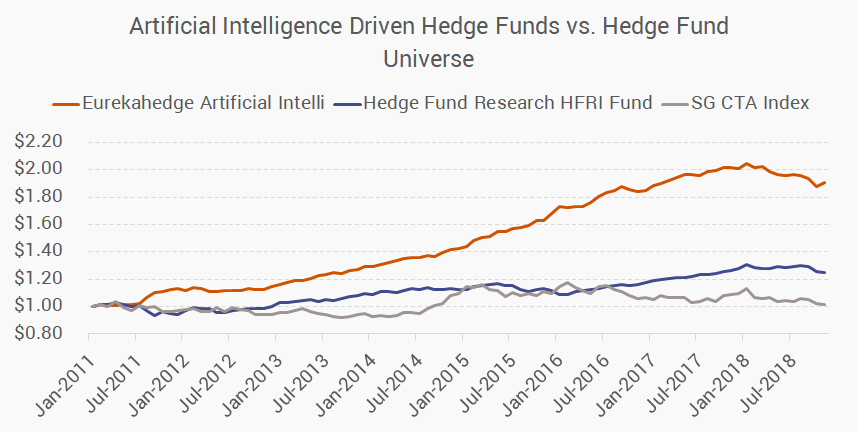

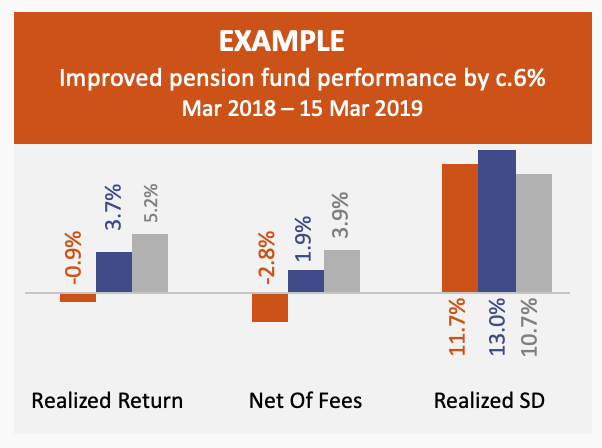

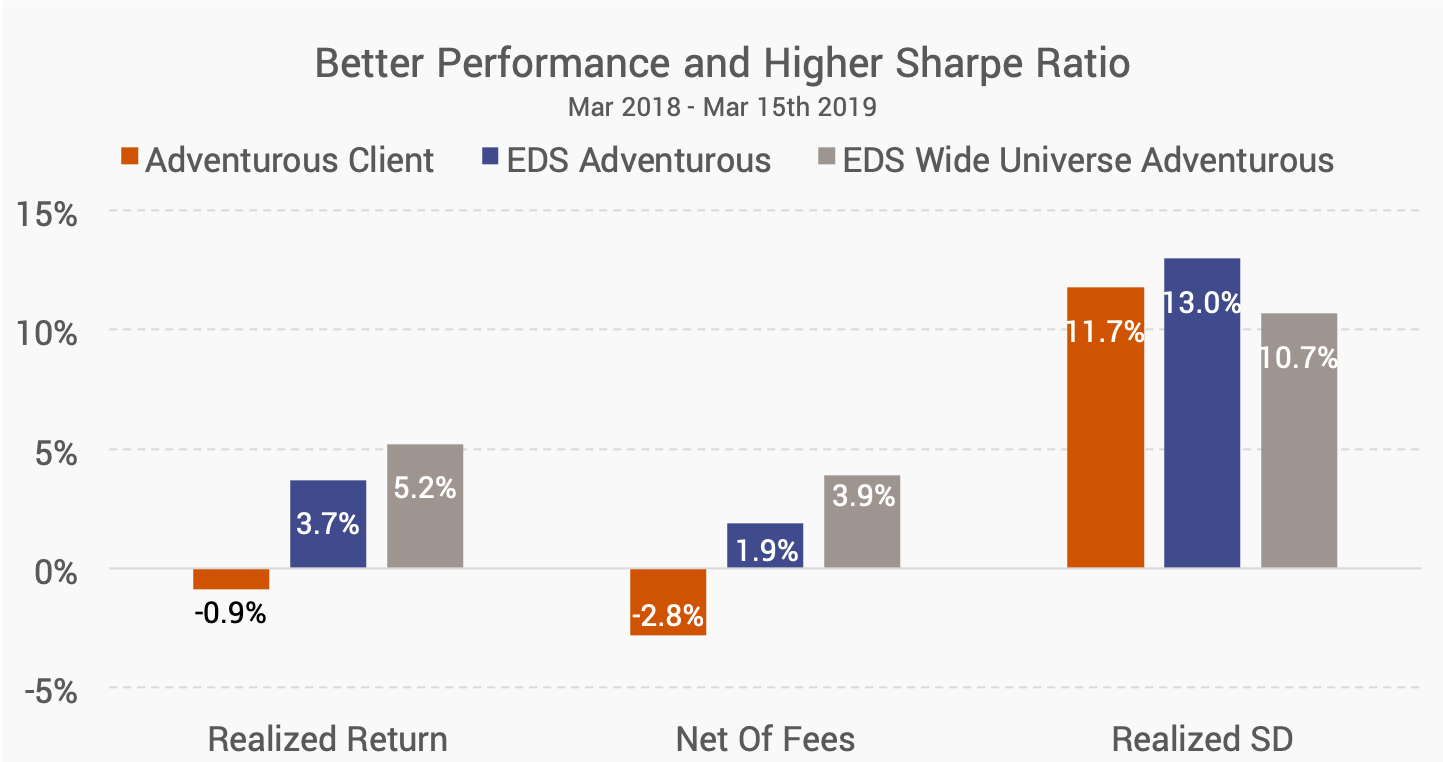

*Past performance is not a reliable indicator of future results, Yearly performance available in the Appendix

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

*Past performance is not a reliable indicator of future results

©2019 Economic Data Sciences

©2019 Economic Data Sciences

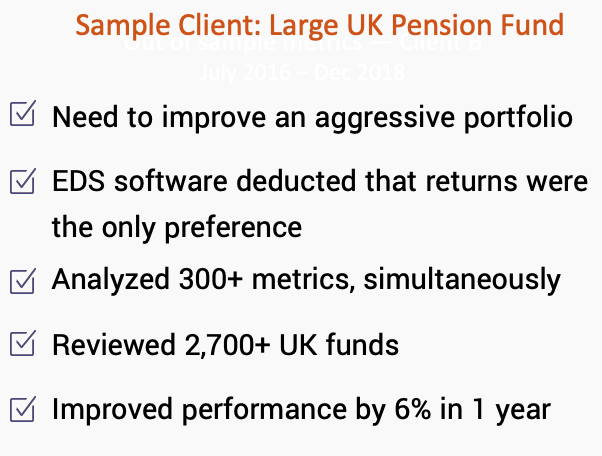

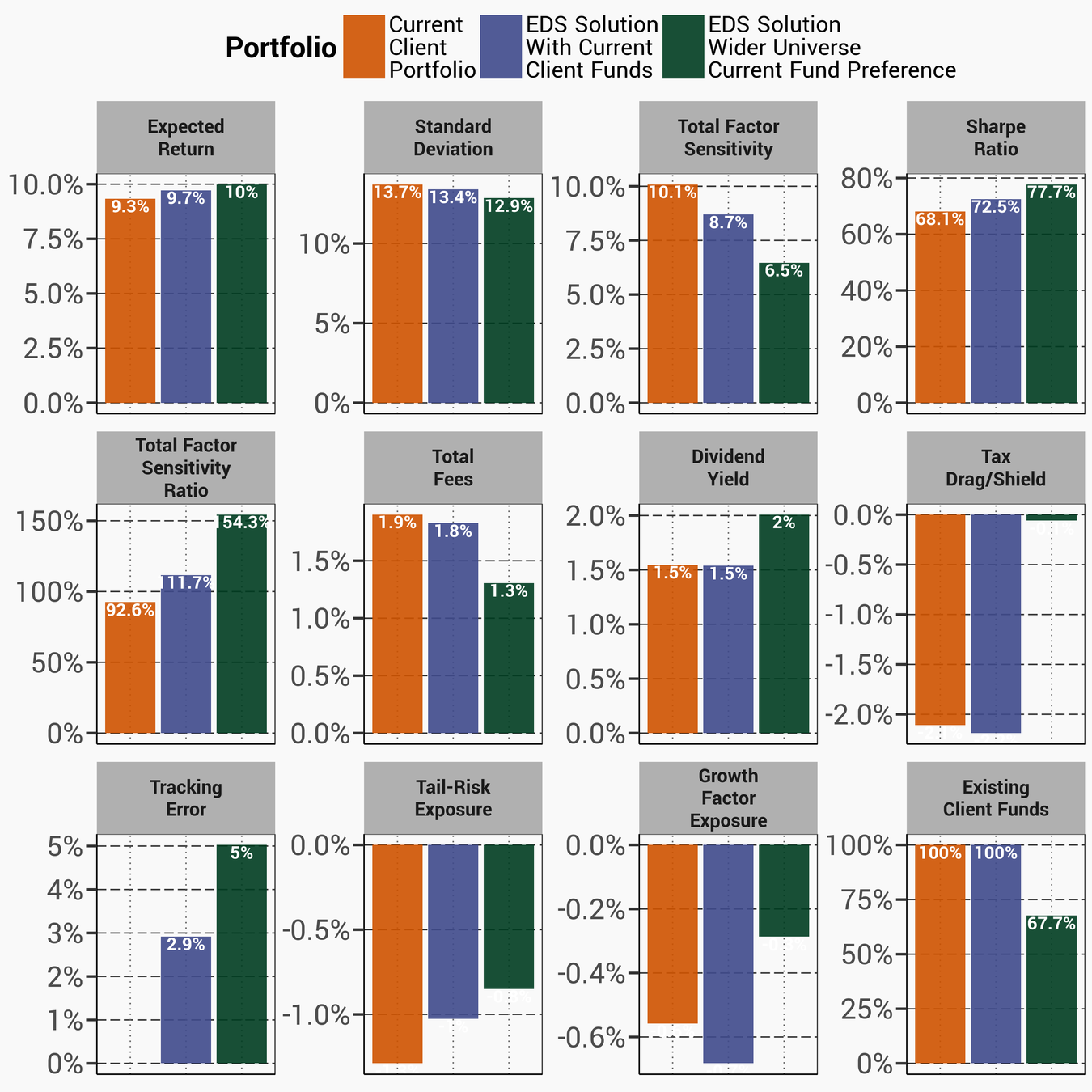

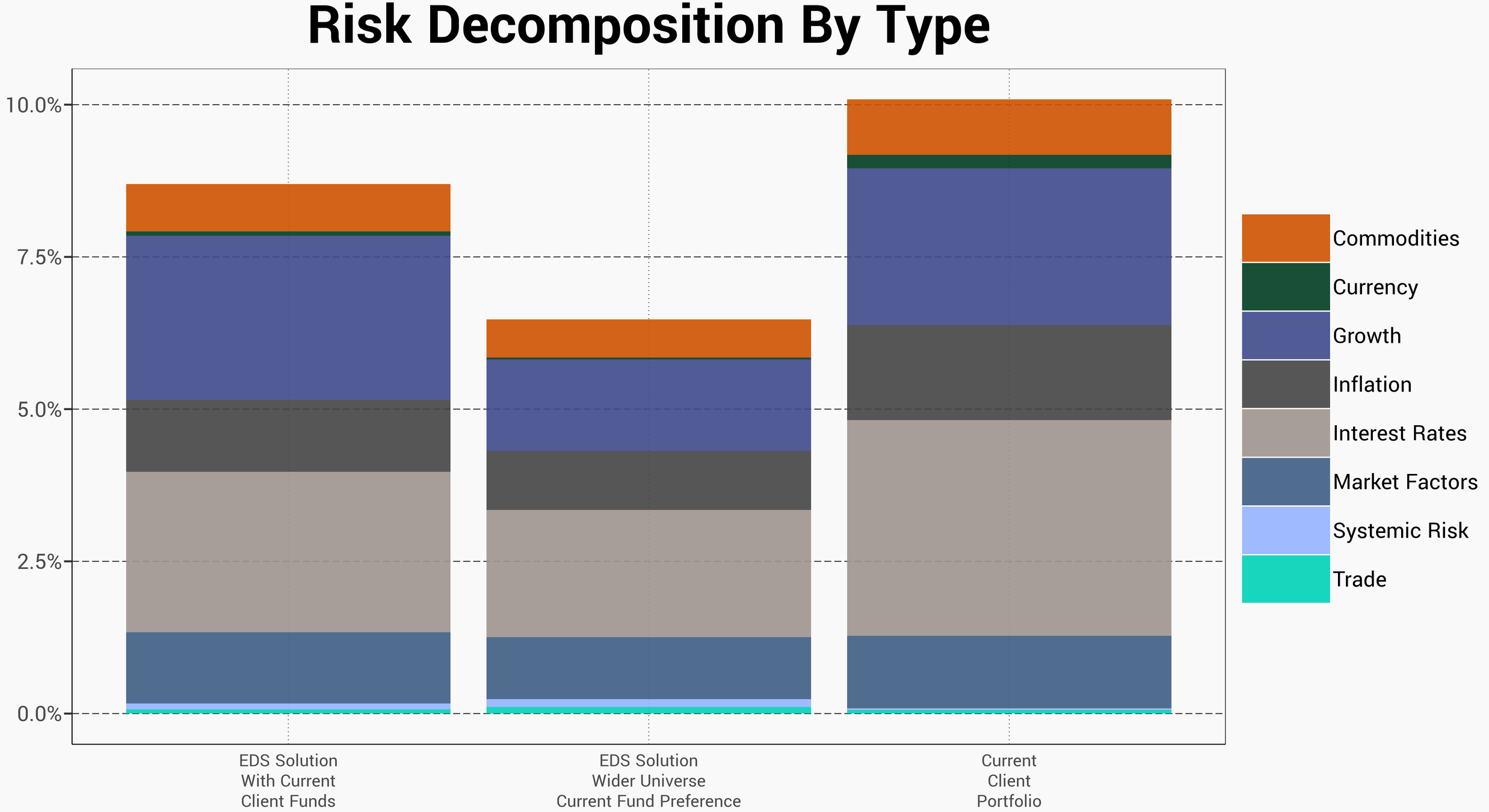

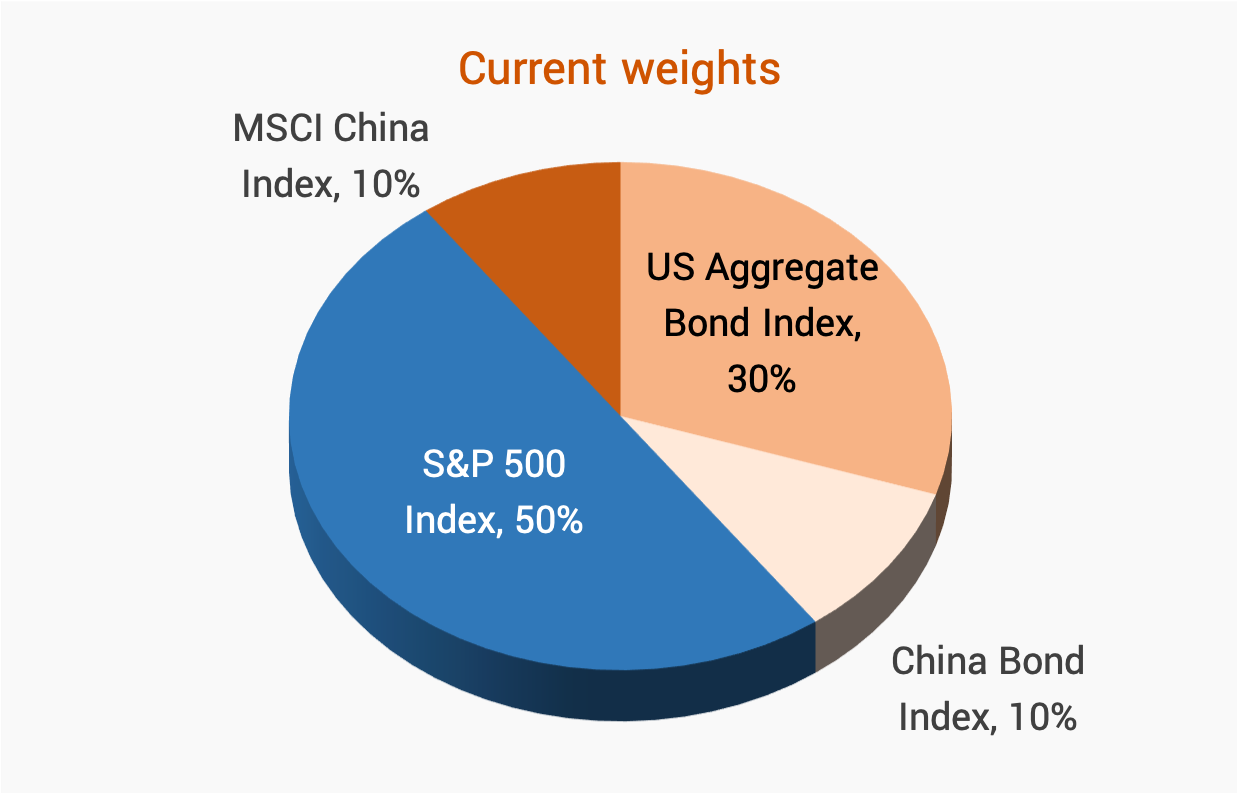

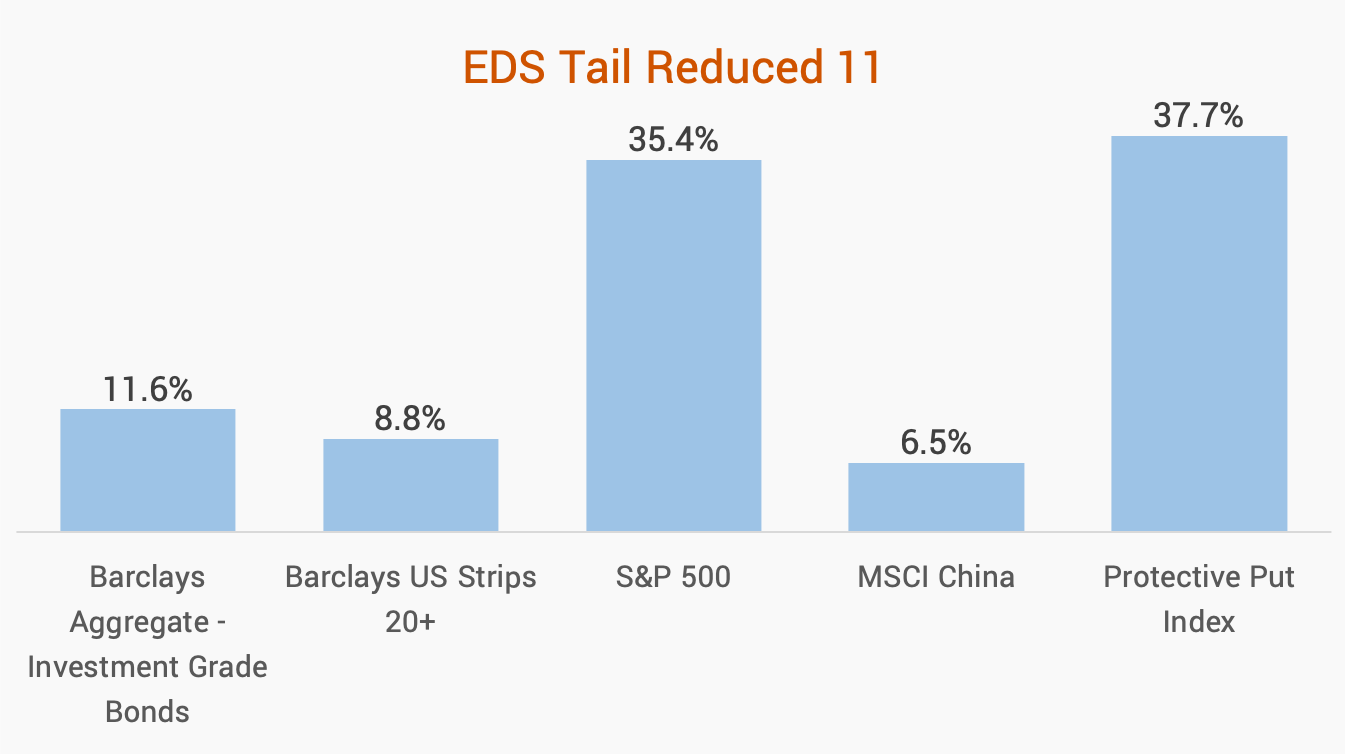

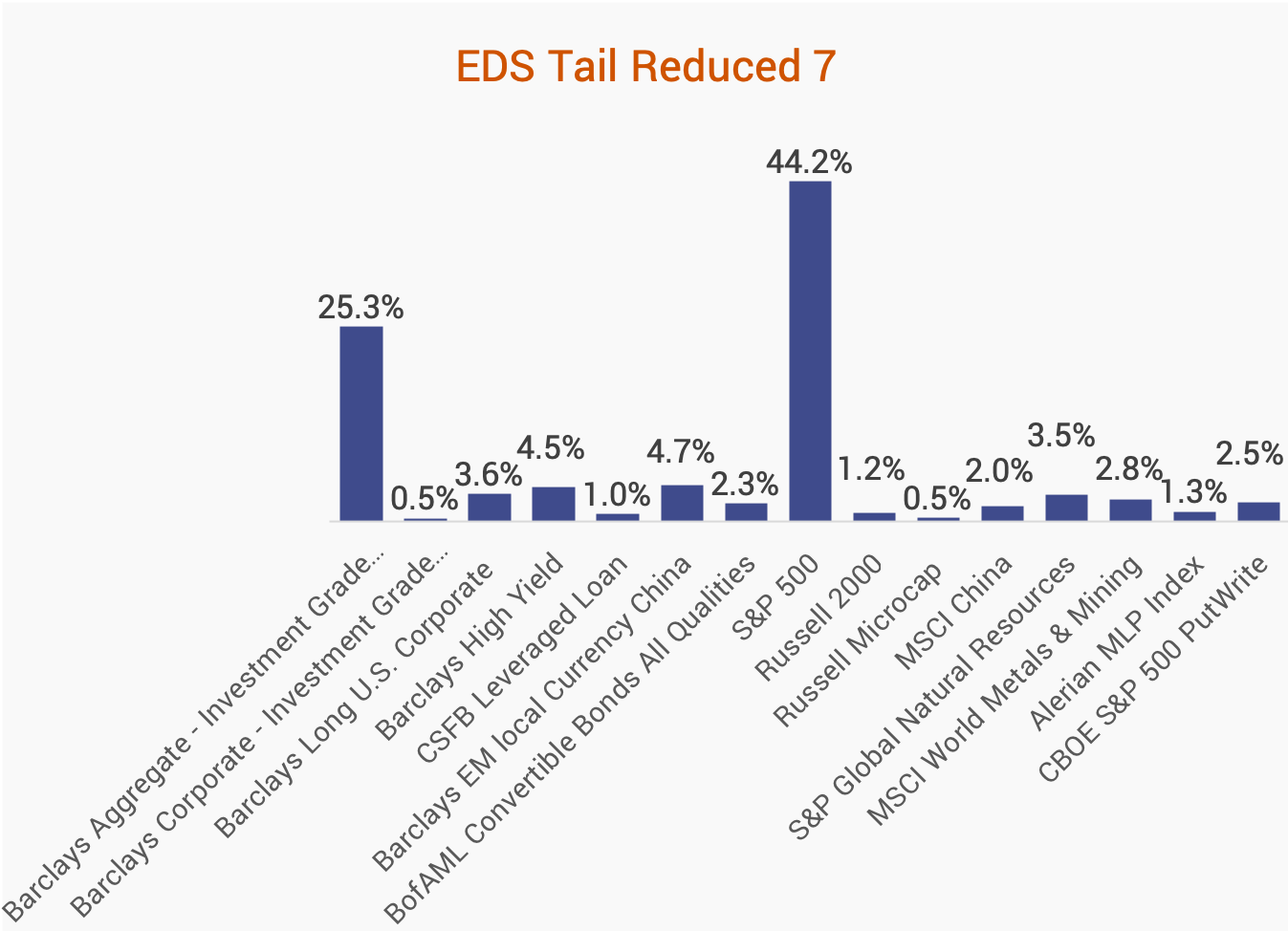

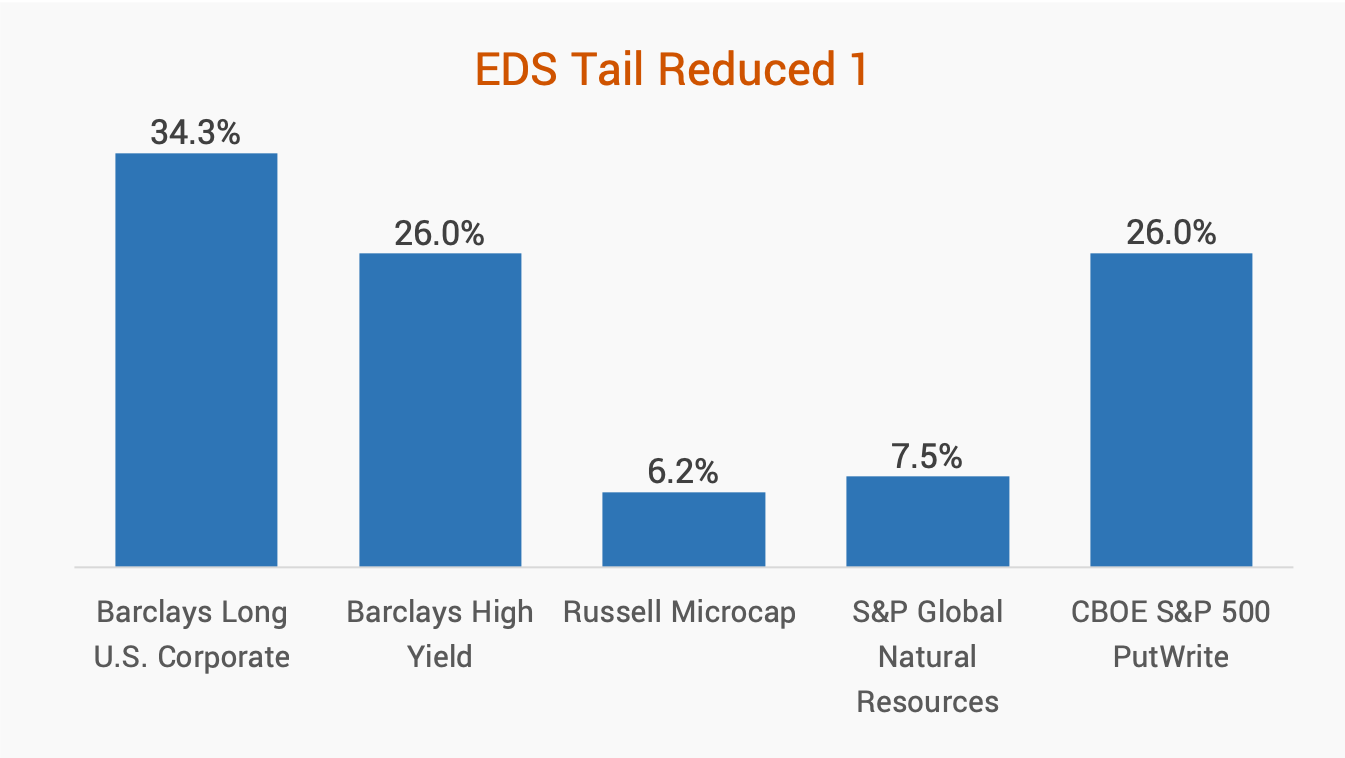

EDS was given a sample portfolio by a UK pension fund. Since only the asset weights were known, EDS tool deducted the investors' preferences and proceeded to analyze the holdings

The following preferences were deducted:

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

*Past performance is not a reliable indicator of future results

©2019 Economic Data Sciences

©2019 Economic Data Sciences

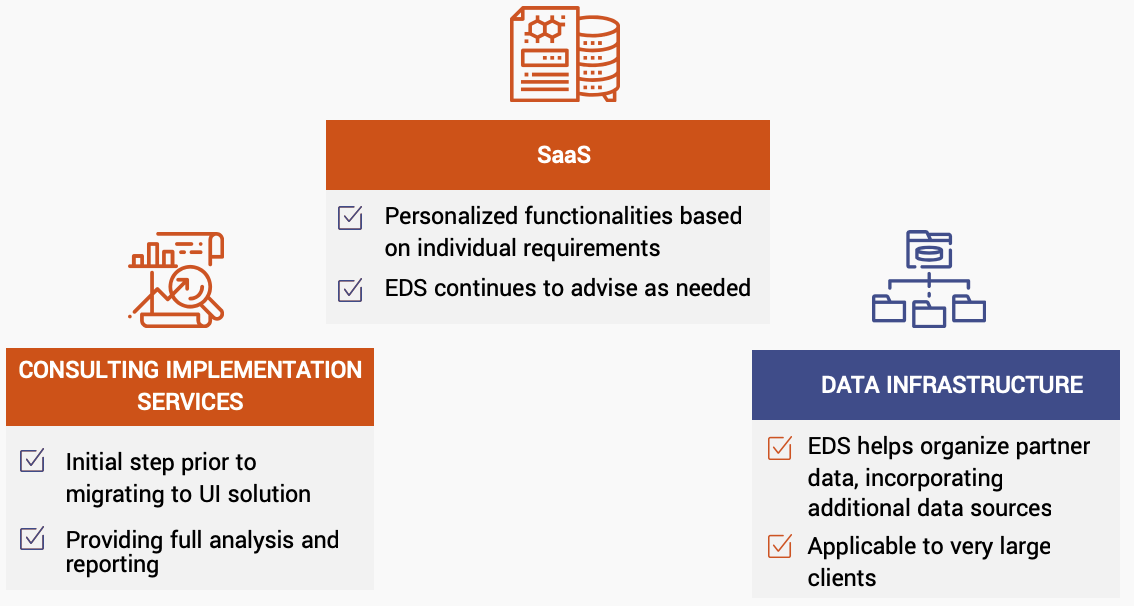

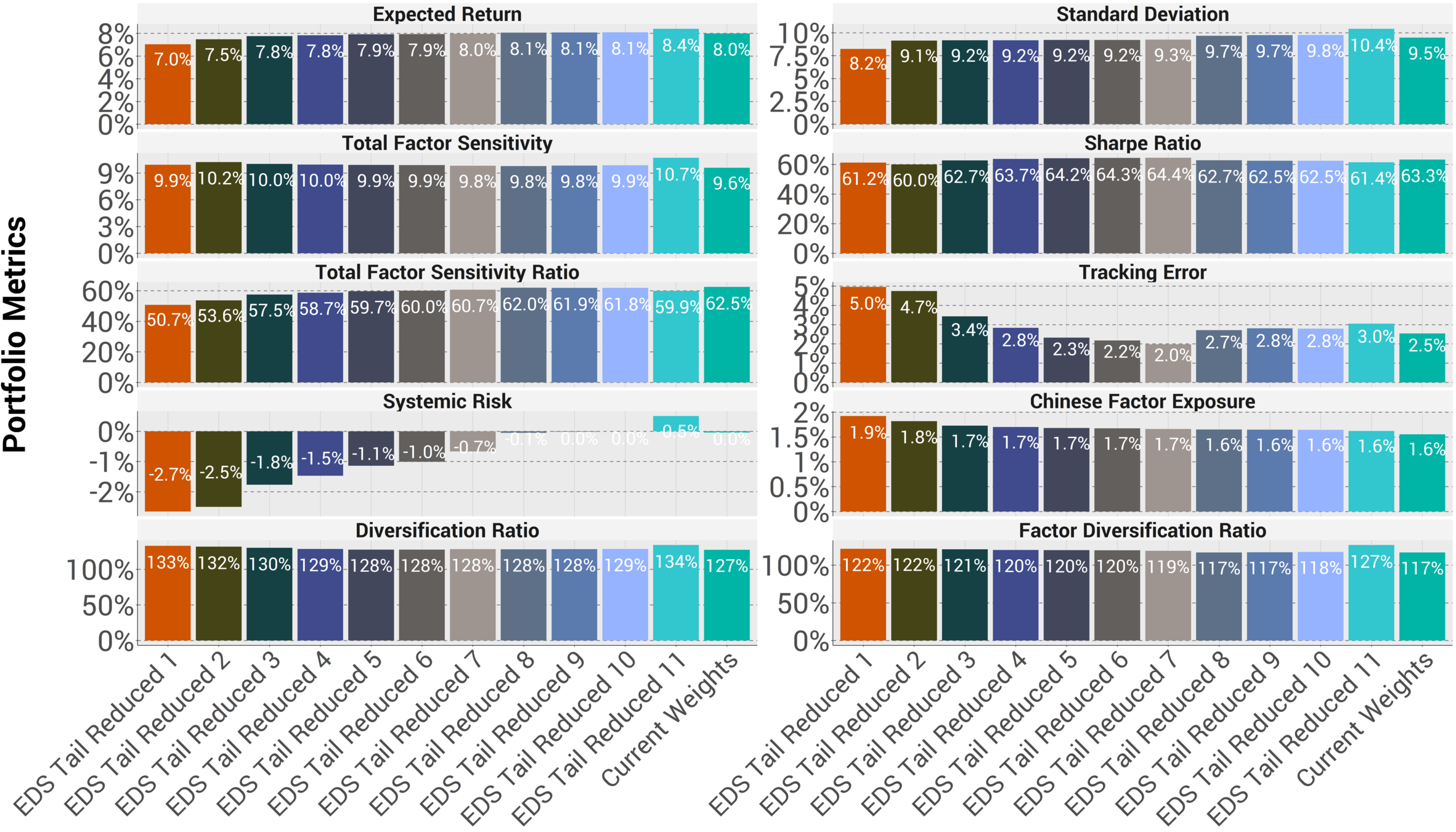

We show how the software iterates through portfolios and provides different options, depending on Client preferences

The Client had several simultaneous goals:

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

Number of funds or desired minimum/maximum fund weight can be modified

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

©2019 Economic Data Sciences

info@EconomicDataSciences.com

By Economic Data Sciences

Quick Intro & 2 Case Studies