Javier García-Bernardo

University of Amsterdam

Mar 13th, 2017

Nature, origins and political consequences of corporate networks in modern economic life?

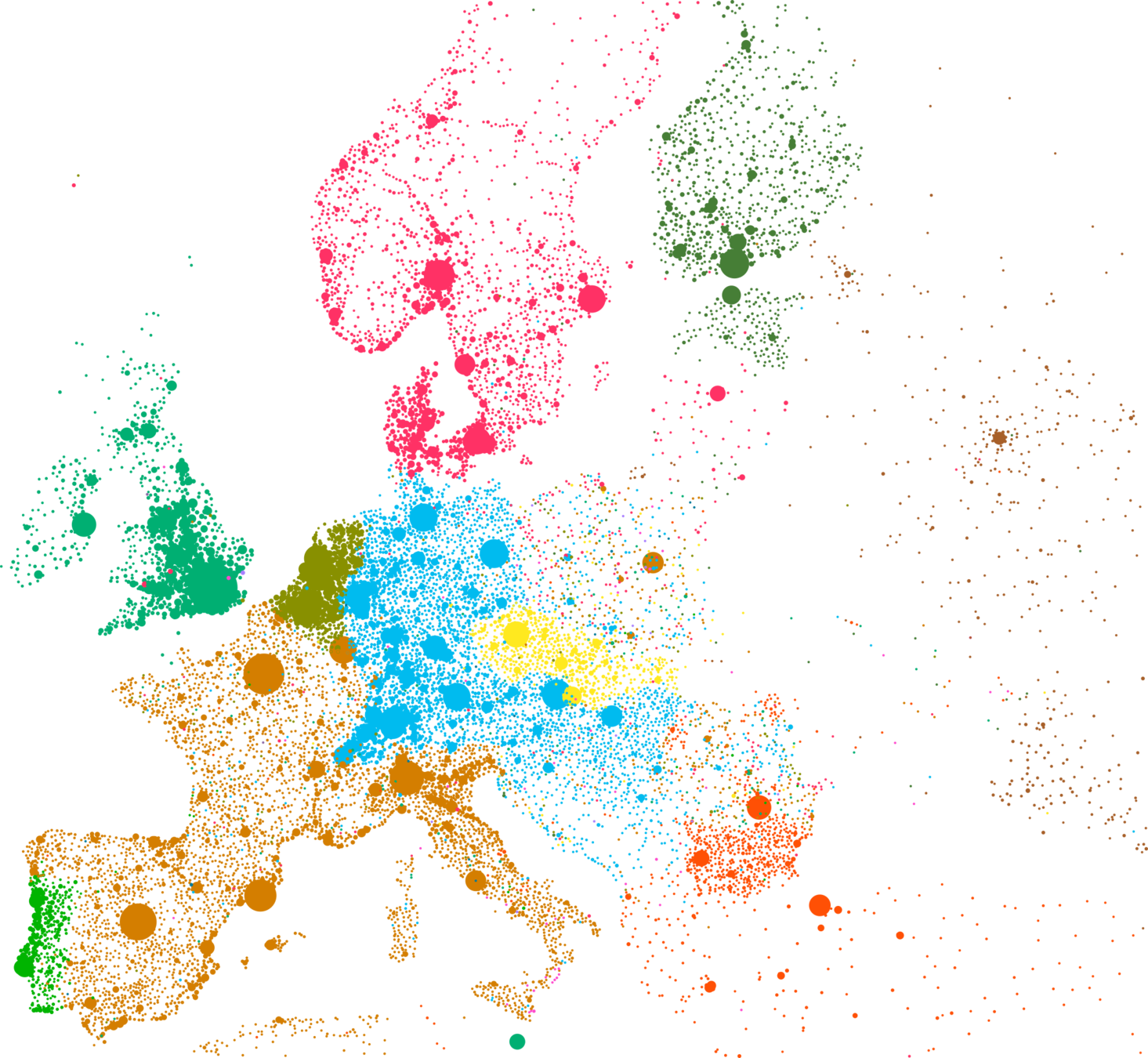

corporate networks

Nodes:

- Companies

Links:

- Shared directors

E.M. Heemskerk, F.W. Takes, J. Garcia-Bernardo and M.J. Huijzer ‘Where is the global corporate elite? A large-scale network study of local and nonlocal interlocking directorates‘, Sociologica 2016(2): 1-31, 2016.

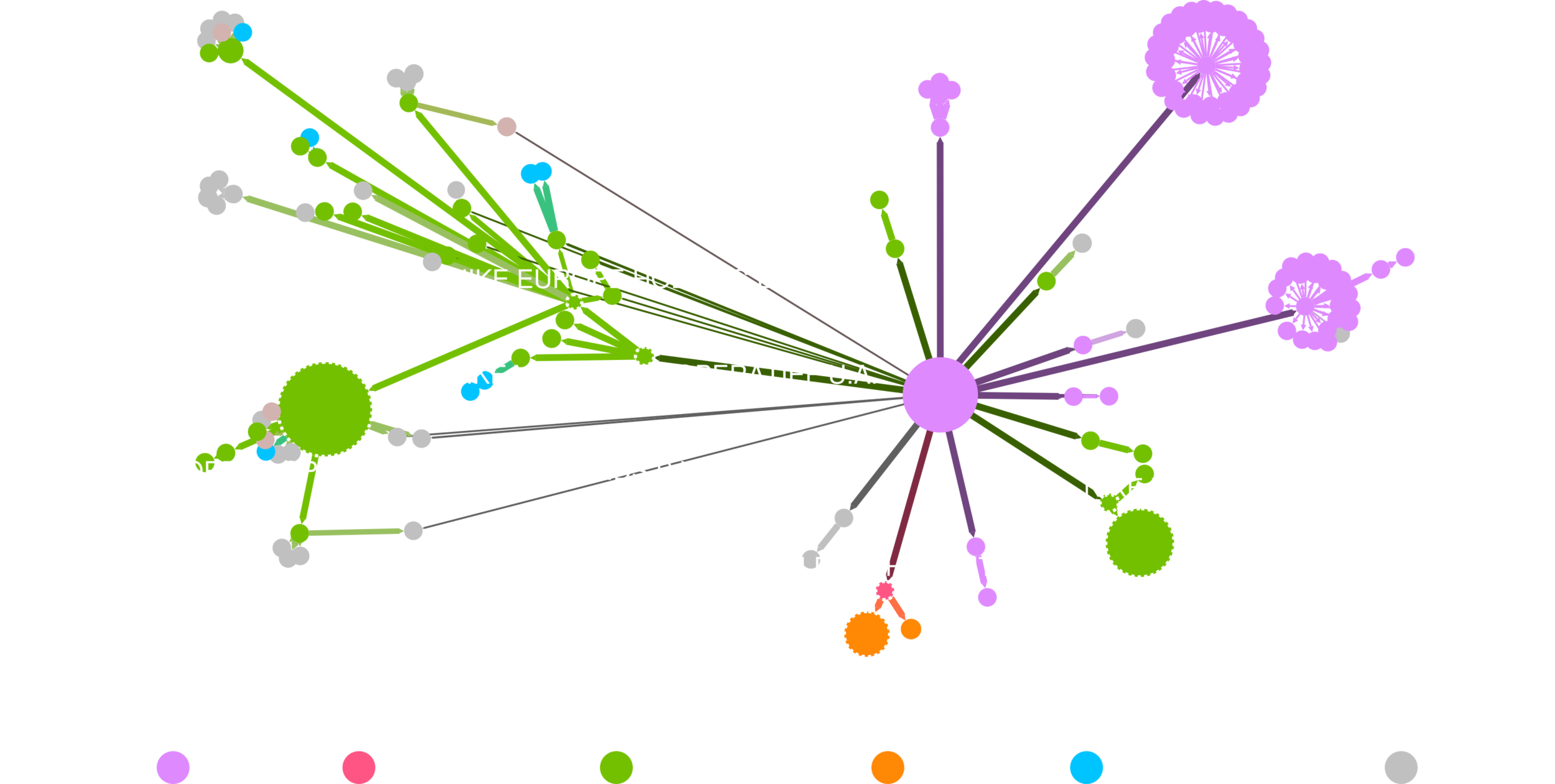

Mr. Jorge Paulo Lemann - Heinz - 3G Capital - AB Inbev - And another 70 positions

Nodes:

- Companies

Links:

- Ownership relationships

corporate networks

PARt 1: how to gain knowledge from complex structures?

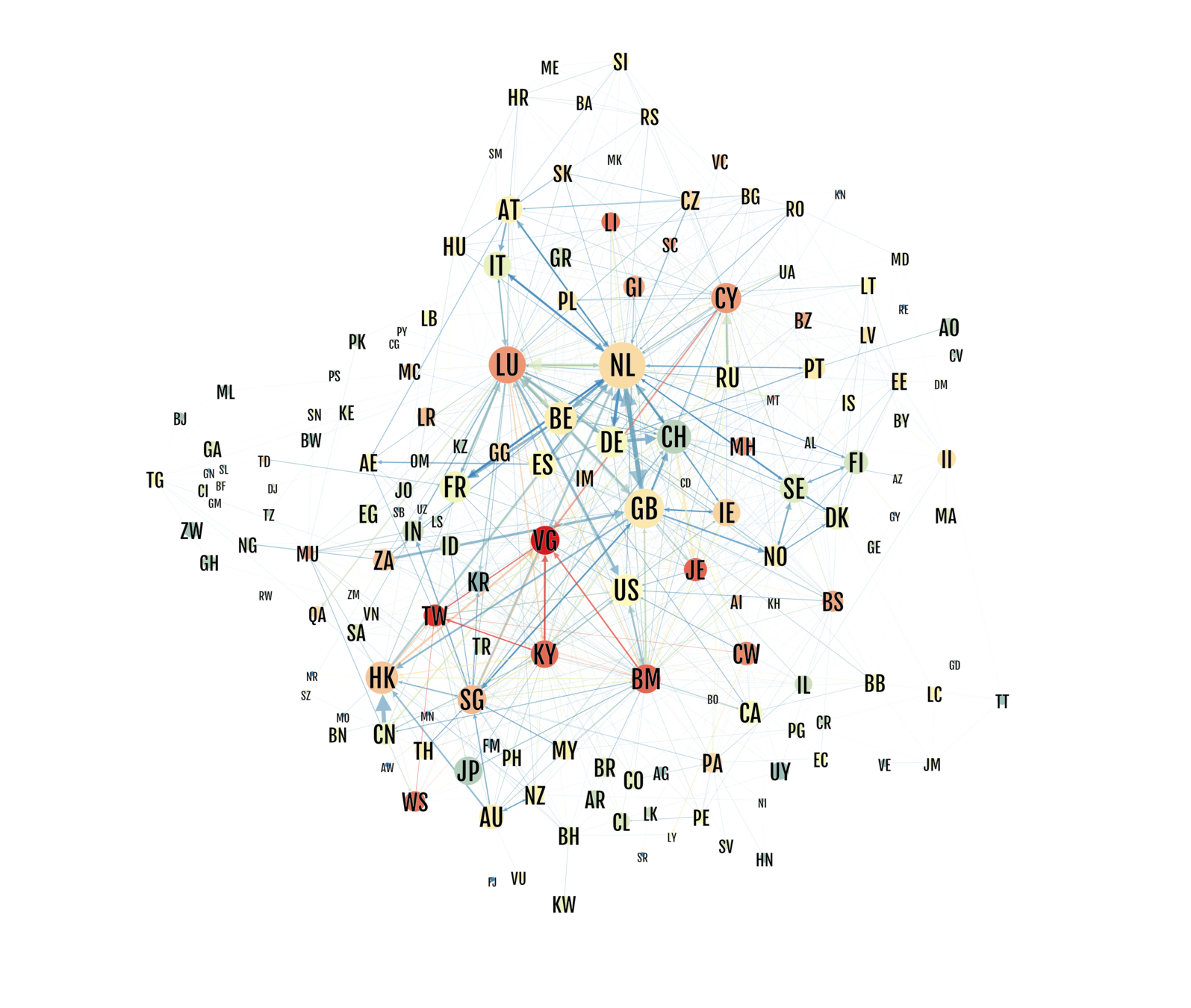

``Uncovering Offshore Financial Centers: Conduits and Sinks in the Global Corporate Ownership Network''

https://www.nature.com/articles/s41598-017-06322-9

Javier Garcia-Bernardo, Jan Fichtner, Frank Takes, Eelke Heemskerk

OFFSHORE FINANCIAL CENTERS

Offshore Financial Center (OFC): a jurisdiction (country) that attracts financial activities from abroad through low taxation and lenient regulation.

- So, which countries are OFCs?

- Definitions differ

- Highly contested and politicized

- FDI/GDP ratio approach: substantially more Foreign Direct Investment than expected based on GDP

- Problematic because:

- No exact investment flows, just dyadic relationships

- OFC homogeneity assumption

- Large countries hard to detect

- No differentiation in roles

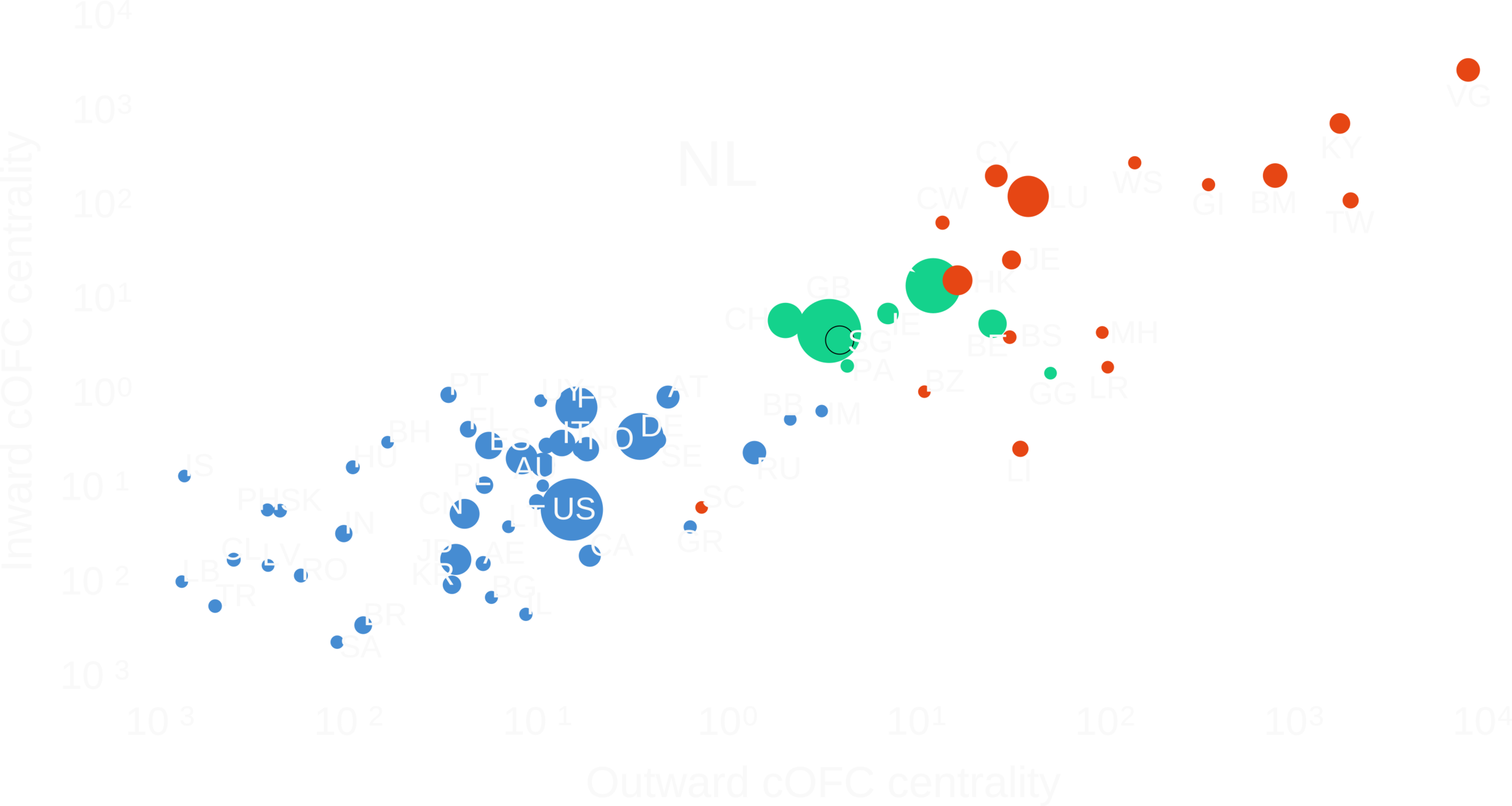

sinks and conduits

We look at which countries are used disproportionally in transnational ownership chains.

ORBIS DATABASE

- 200 million companies

- 70 million ownership relationships

- 10 million transnational chains

sink-OFCs

sink-OFFshore financial centers

15 companies per capita

siNKS ARE RELATIVELY STABLE OVER TIME

siNKS ARE geographically specialized

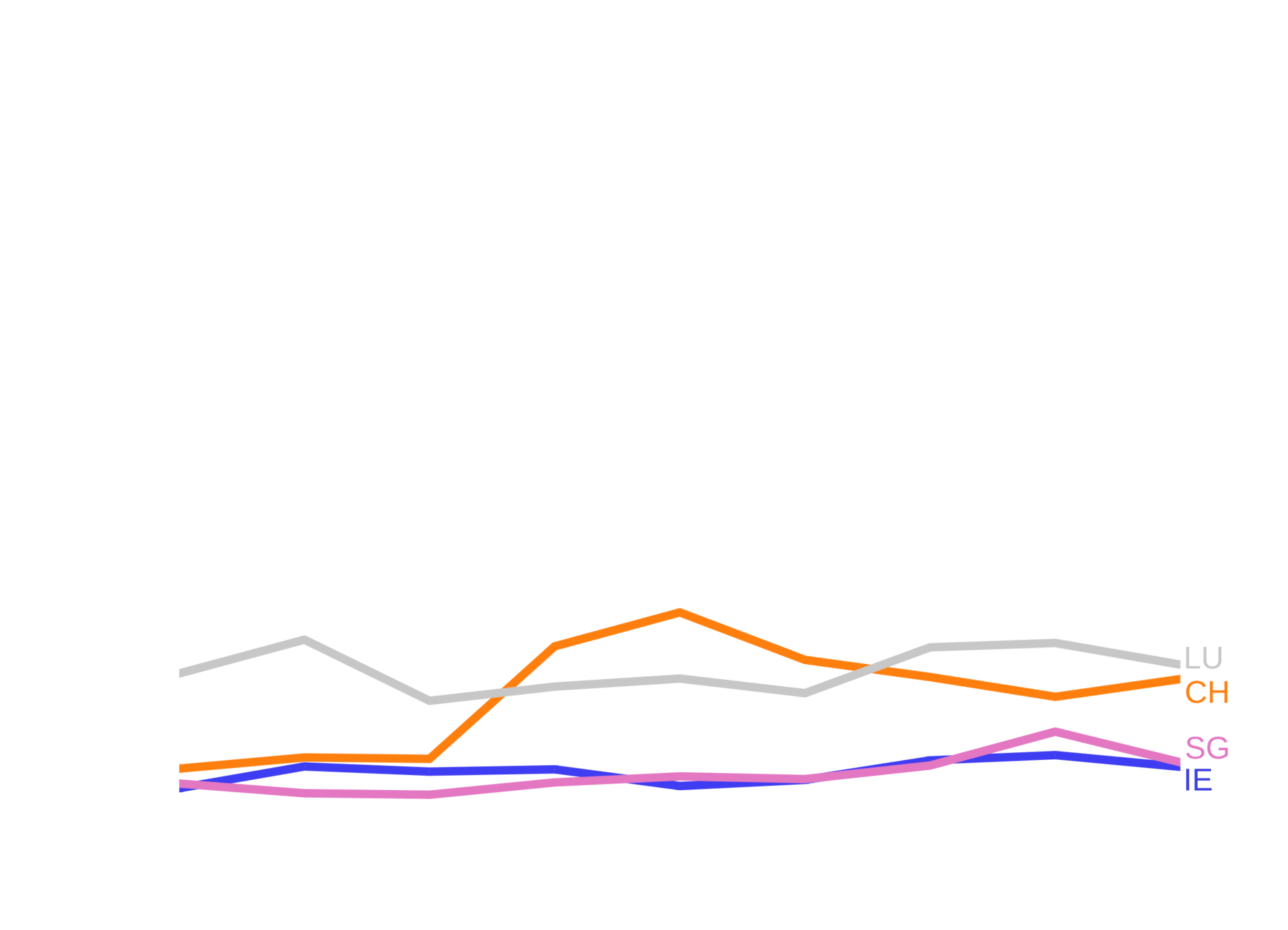

conduit-OFCs

conduit-OFFshore financial centers

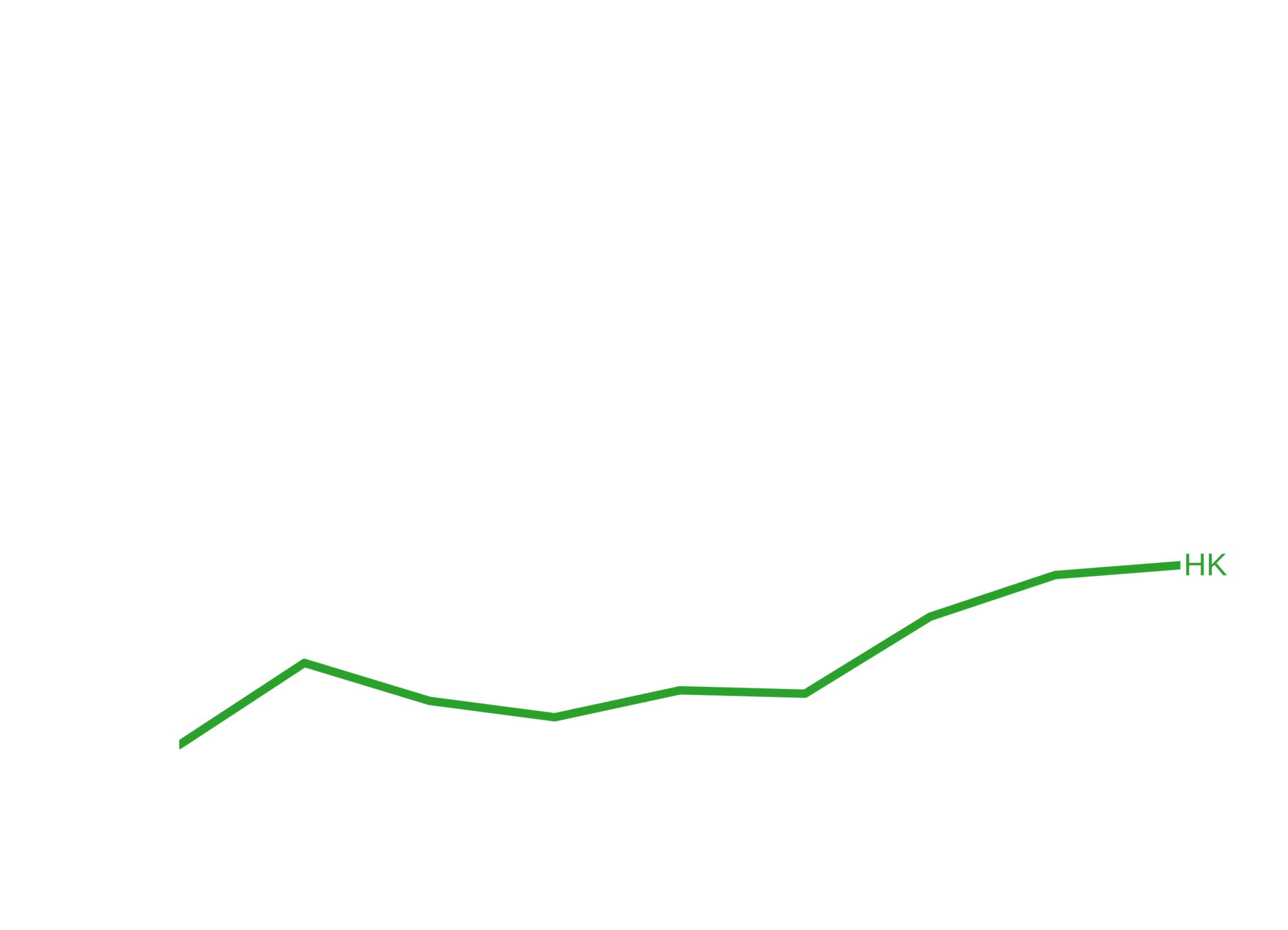

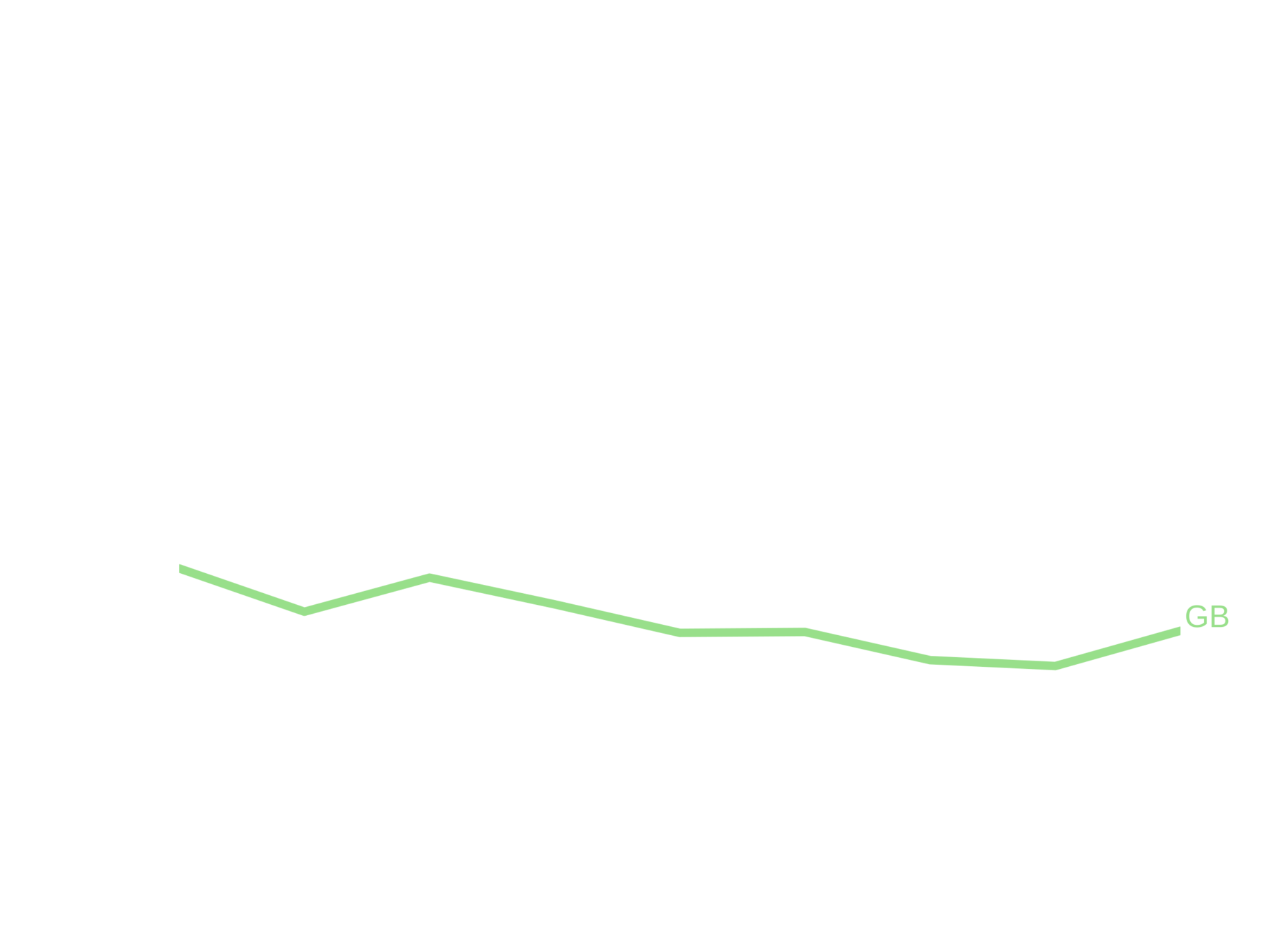

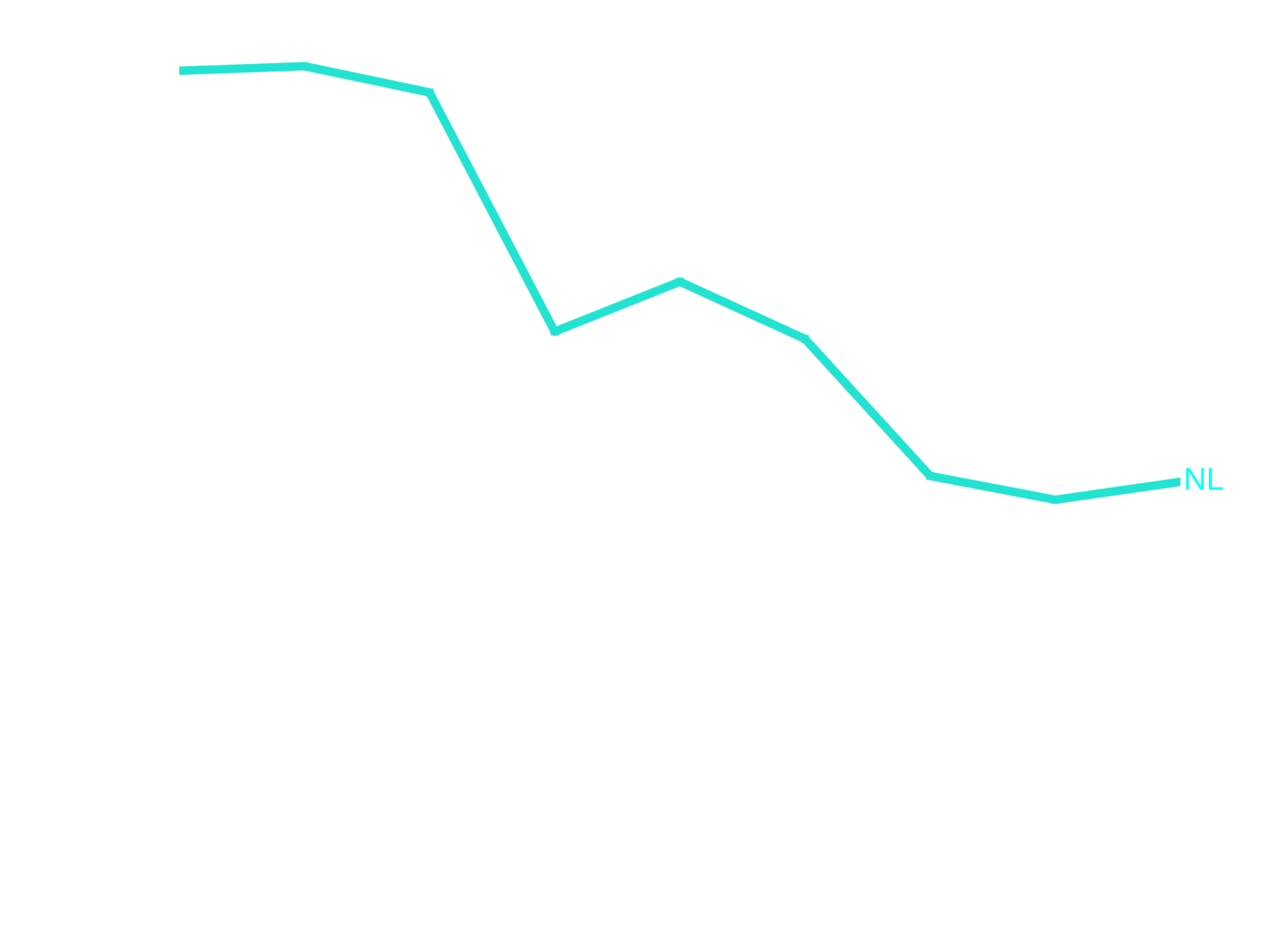

Larger flows towards sink-OFCs

Larger flows from sink-OFCs

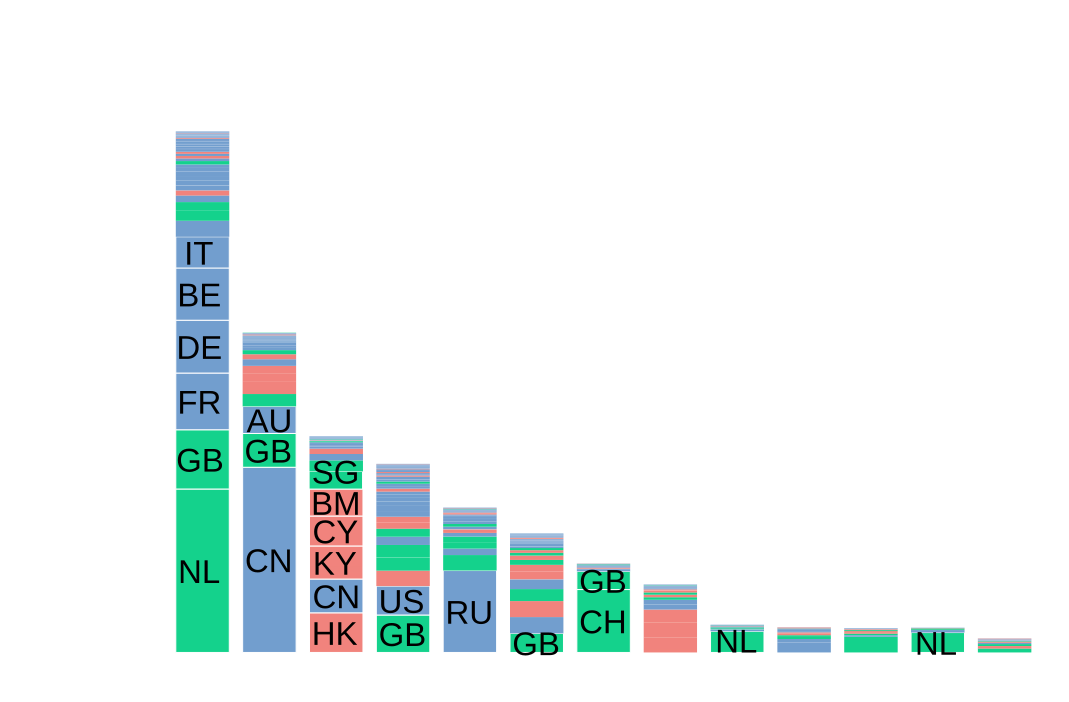

decline of the netherlands

importance of the netherlands

-

23% of all the value flowing to a sink-OFC flows through a Dutch Special Financial Institutions

- Percentage of chains that go through the Netherlands and end in:

-

Luxembourg: 40%

-

Cyprus: 30%

-

Malta: 71%

-

Curaçao: 90%

-

Lichtenstein: 30%

-

PARt 2: why the netherlands?

Historical reasons:

- Curaçao: Just before World War II, Dutch multinationals moved to CW to avoid the confiscation of assets.

- Curaçao developed a prominent and flexible management industry.

- Used to avoid withholding taxes (no longer applicable)

- Effective tax rate in CW: 2.4 - 3%

During the 80s there was a push towards attracting corporations in the Netherlands.

importance of the netherlands

Reasons

(PwC / EY / DELOITTE / KPMG)

- Logistic:

- Located in the heart of Europe.

- Outstanding infrastructure.

- Highly educated and multilingual workforce.

- Well-developed trust and management services.

- Easy to start Special Purpose Entities (SFIs in NL)

- Beneficial tax regime:

- No withholding taxes for interest and royalties.

- No real withholding tax for dividends.

- Participation exemption.

- Large number of tax treaties.

- Advance Tax Rulings (ATR) and Advance Pricing Agreements (APA)

- Investor protection

- Large number of bilateral investment treaties

- Advanced tax ruling system (increases certainty)

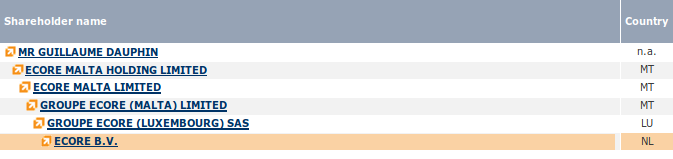

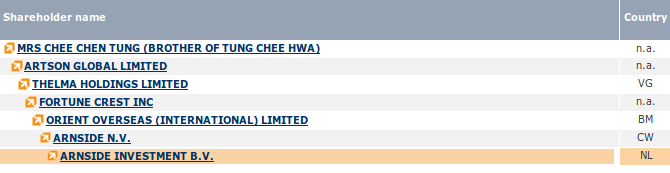

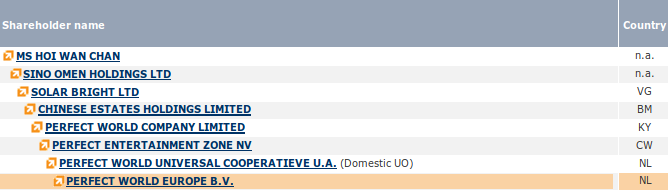

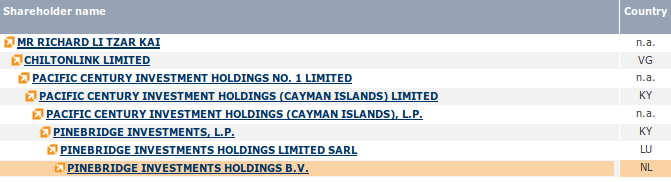

INDIVIDUALS INVESTING Through THE NETHERLANDS

Orbis data, blanked

INDIVIDUALS INVESTING Through THE NETHERLANDS

Orbis data, blanked

PART 3: the intermediaries

- Asset management structures are complex for two reasons:

- Mergers/acquisitions make them complex (for corporations)

- Are created complex (for corporations/individuals):

- To hedge against failures

- To avoid regulations

- To avoid taxation

- They are created by intermediaries:

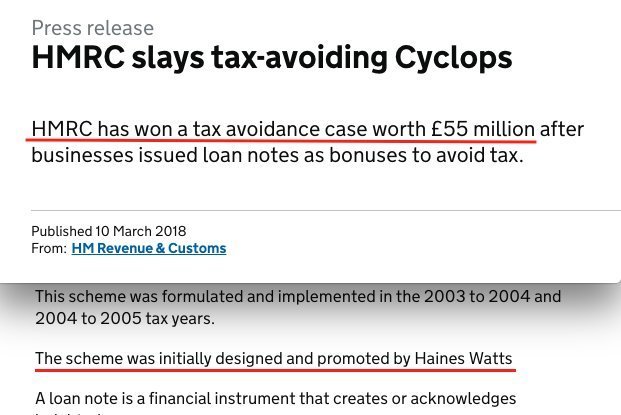

- Law/trust firms (Appleby, Mossack Fonseca, Intertrust)

- Accounting/auditor firms (The Big Four)

- In the case of private investors there are usually several layers of intermediaries involved.

- 25% of all Dutch entities are registered in 1% of all addresses; 41% in Luxembourg.

the intermediaries

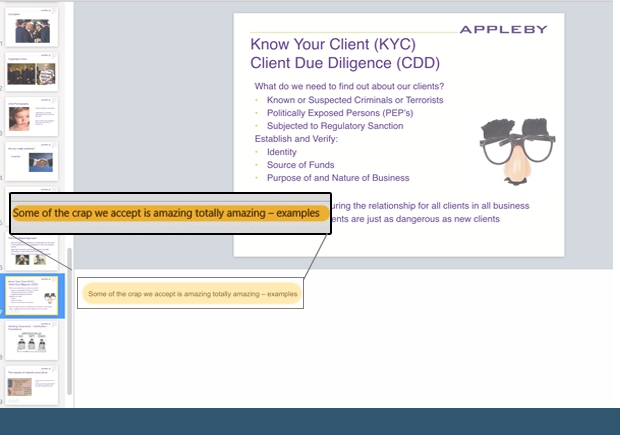

Source: Internal presentation by the director of compliance (Woods)

- - Terrorist financing offences: “We have a current case where we are sitting on about 400K that is definitely tainted and it is not easy to deal with.”

- - Set up a trust and accepted money on his behalf “without question.”

- Intermediaries typically advise clients to go offshore:

- Reduces or eliminates taxes

- Prevents courts control over assets

- Privacy: Exchange of information only on request

- "Business-friendly" legislation

- A typical trick to increase privacy is to give up legal ownership of your assets (but maintain beneficial ownership)

- Foundation/Stichting: Not private

- Trust:

- Originated from common law

- Person (trustee) accepts assets from another person (settlor), for the benefit of a third person (beneficiary).

- Private relationships, no legal entities, no record whatsoever.

- "Flee" clauses: In case of specified "trigger" events, automatically transfers the trustees, assets, and governing law of the trust to another jurisdiction.

the intermediaries

- Another trick to increase privacy is to use layering:

- Layer a trust through four countries for the trustee, settler, beneficiary and governing law.

- Add layers of shell companies within your structure in different countries.

- Exchange of information is on request. Takes 2-3 months to answer.

- The registry of corporations lie with the intermediaries.

- An investigation involves asking the company for information about one of their clients.

- How to prevent this?

- More transparency (EU, OECD)

- Using a big data approach, combining databases.

the intermediaries

summary

1. Offshore financial centers can be divided into sinks and conduits

- Sinks are:

- EU: Luxembourg, Malta, Cyprus, Jersey, Gibraltar

- Other former colonies/territories of the United Kingdom

- Conduits are:

- Netherlands, Ireland, Switzerland, Singapore, United Kingdom

2. The Netherlands is the largest conduit in offshore finance:

- Long history of offshore asset management

- Great infrastructure, services and taxes

- It is declining: more strict regulations in the last decade

3. Asset management structures are becoming more complex. We need new techniques to be able to detect tax fraud.

corpnet.uva.nl

@javiergb_com

@uvaCORPNET

javiergb.com

corpnet@uva.nl

garcia@uva.nl

This presentation: slides.com/jgarciab/bd

Belastingdienst presentatie March 2018

By Javier GB

Belastingdienst presentatie March 2018

sink and conduits in Corporate Structures