LP Wealth Growth in Uniswap

Preliminaries

- \(X_t, Y_t \) are the quantities of numeraire and asset held by the LPs in the AMM

- The price process of the asset is defined as \(S_0 = 1, S_t = S_{t-1}e^{\delta U_t}\)

- \(\{U_i\}_{i \in \mathbb{N}}\) are i.i.d random variables s.t. \(\mathbb{P}[U_i = 1] = p, \ \mathbb{P}[U_i = -1] = 1-p\)

- The implicit price given by the curve at time \(t\) is given by \(S_t^{\ast} = \frac{X_t}{Y_t}\)

- Percentage fee: \((1 - \gamma)\), we constrain \(\gamma\) to be of the form \(e^{- k_{\gamma} \delta}, k_{\gamma} \in \mathbb{Z}\)

- Trading equation \((X_t + \Delta X_t)^{\gamma} (Y_t - \Delta Y_t) = X_t^{\gamma} Y_t\)

- Note that this is equivalent to \((X_t + \gamma\Delta X_t) (Y_t - \Delta Y_t) = X_t Y_t\)

\begin{aligned}

\therefore \left(1 + \frac{\Delta X_t}{X_t}\right)^{\gamma} \left(1 - \frac{\Delta Y_t}{Y_t}\right) = 1 \quad

&\implies \left(1 + \gamma\frac{\Delta X_t}{X_t}\right) \left(1 - \frac{\Delta Y_t}{Y_t}\right) = 1

\end{aligned}

\begin{aligned}

\therefore (X_t + \gamma\Delta X_t) (Y_t - \Delta Y_t) &= X_t Y_t

\end{aligned}

\begin{aligned}

(X_t + \Delta X_t)^{\gamma} (Y_t - \Delta Y_t) &= X_t^{\gamma} Y_t

\end{aligned}

Markov Chains

- A stochastic model describing a sequence of possible events in which the probability of each event depends only on the current system state.

- A discrete-time Markov chain is a sequence of random variables \(X_1, X_2, X_3, \ldots \) s.t.

\mathbb{P}\left(X_{n+1} = x \ | \ X_1 = x_1, X_2 = x_2, \dots, X_{n} = x_n\right) = \mathbb{P}\left(X_{n+1} = x \ | \ X_{n} = x_n\right)

Credits: https://setosa.io/ev/markov-chains/

Markov Chains

- State space: \(S = \{A, B\}\), Transition matrix \(P \in \mathbb{R}_{[0, 1]}^{|S| \times |S|}\)

- Stationary distribution: A probability distribution \(\pi = (p_A, p_B)\) that remains unchanged in the Markov chain as time progresses.

\pi P = \pi

- Clearly, \(\pi\) is the left eigenvector of P for the eigenvalue \(\lambda = 1\).

- For the above \(P\), we would have \(\pi = \left(\frac{5}{8}, \frac{3}{8}\right)\)

Implicit Price Manipulation

- Suppose at time \(t\), we have \(S_t = \gamma^{-1}\left(\frac{X_t}{Y_t}\right) e^{\delta} = \gamma S_t^{\ast} e^{\delta}\)

- We wish to bring the implicit price to \(S_{t+1}^{\ast} = \left(\frac{X_t}{Y_t}\right) e^{\delta}\) by trading \(\Delta Y_t\) for \(\Delta X_t\)

- Thus, we have

\begin{aligned}

\left(\frac{X_t + \Delta X_t}{Y_t - \Delta Y_t}\right) &= \left(\frac{X_t}{Y_t}\right) e^{\delta}\\[15pt]

\quad (X_t + \Delta X_t)^{\gamma} (Y_t - \Delta Y_t) &= X_t^{\gamma} Y_t

\end{aligned}

\begin{aligned}

\implies \ \left(1 + \frac{\Delta X_t}{X_t}\right) = \left(1 - \frac{\Delta Y_t}{Y_t}\right) e^{\delta}

\end{aligned}

\begin{aligned}

\implies \ \left(1 + \frac{\Delta X_t}{X_t}\right)^{\gamma} \left(1 - \frac{\Delta Y_t}{Y_t}\right) = 1

\end{aligned}

\begin{aligned}

\therefore \quad \Delta X_t = X_t\left(e^{\frac{\delta}{\gamma + 1}} - 1\right), \ \Delta Y_t = Y_t\left(1 - e^{\frac{-\gamma\delta}{\gamma + 1}}\right)

\end{aligned}

- Similarly, if \(S_t = \gamma \left(\frac{X_t}{Y_t}\right) e^{-\delta}\) and we pull the implicit price to \(S_{t+1}^{\ast} = \left(\frac{X_t}{Y_t}\right) e^{-\delta}\)

\begin{aligned}

\therefore \quad \Delta X_t = X_t\left(1 - e^{\frac{-\gamma\delta}{\gamma + 1}}\right), \ \Delta Y_t = Y_t\left(e^{\frac{\delta}{\gamma + 1}} - 1\right)

\end{aligned}

Price as Markov Process

- Recall, we traded \(\Delta Y_t\) for \(\Delta X_t\) when \(S_t = \gamma^{-1} S_t^{\ast} e^{\delta} \implies S_t > \gamma^{-1} S_t^{\ast} \)

- Similarly, we traded \(\Delta X_t\) for \(\Delta Y_t\) when \(S_t = \gamma S_t^{\ast} e^{-\delta} \implies S_t < \gamma S_t^{\ast} \)

Not profitable

Get \(\Delta Y_t\) for \(\Delta X_t\)

Get \(\Delta X_t\) for \(\Delta Y_t\)

\(0\)

\(\delta\)

\(-\delta\)

\(k_{\gamma}\delta\)

\(-k_{\gamma}\delta\)

\(\dots\)

\(\dots\)

\(k_{\gamma}\delta+\delta\)

\(-k_{\gamma}\delta-\delta\)

\text{log}\left(\frac{S_t}{S_t^{\ast}}\right)

- Thus, \(M_t = \text{log}\left(\frac{S_t}{S_t^{\ast}}\right)\) is a Markov process with \(S = \{-k_{\gamma}\delta, \dots, -1, 0, 1, \dots, k_{\gamma}\delta\}\).

- A trade occurs when \(M_t\) stays on one of the two end states.

- Let's construct the transition matrix \(P\) and find a stationary distribution \(\pi\)

Price as Markov Process

- Let's construct the transition matrix \(P\) and find a stationary distribution \(\pi\)

\(-k_{\gamma}\delta\)

\(-k_{\gamma}\delta + \delta\)

\(-k_{\gamma}\delta + \delta\)

\(-k_{\gamma}\delta\)

\(\ldots\)

\(k_{\gamma}\delta\)

\(k_{\gamma}\delta\)

\(\ldots\)

\(-k_{\gamma}\delta + 2\delta\)

\(1-p\)

\(p\)

\(0\)

\(1-p\)

\(1-p\)

\(p\)

\(1-p\)

\(p\)

\(p\)

\(0\)

\(0\)

\(p\)

\(0\)

\text{log}\left(\frac{S_t}{S_t^{\ast}}\right)

\pi =

\begin{cases}

\left[ (2k_{\gamma} + 1)^{-1}, \dots, (2k_{\gamma} + 1)^{-1} \right] & \text{if } p = 0.5 \\[5pt]

\left[ \frac{(1 - c)}{c^{-(2k_{\gamma}+1)} - 1},

\frac{(1 - c)c^{-1}}{c^{-(2k_{\gamma}+1)} - 1},

\frac{(1 - c)c^{-(2k_{\gamma} + 1)}}{c^{-(2k_{\gamma}+1)} - 1} \right] & \text{if } p \in (0.5,1], \ c = \frac{1-p}{p}

\end{cases}

Constant Growth of Invariant

\begin{aligned}

K_{\gamma} &= \frac{(X + \Delta X_t)(Y - \Delta Y_t)}{X_t Y_t} \\[5pt]

&= \left(\frac{X + \Delta X_t}{X_t}\right)^{1 - \gamma} \frac{(X + \Delta X_t)^{\gamma}(Y - \Delta Y_t)}{X_t^{\gamma} Y_t} \\[5pt]

&= \left(1 + \frac{\Delta X_t}{X_t}\right)^{1 - \gamma} = e^{\delta \frac{1 - \gamma}{1 + \gamma}}

\end{aligned}

- After each trade the product \(C_t = X_tY_t\) is increased by the same factor \(K_{\gamma}\)

- If \(N_t\) trades occur until time \(t\), the wealth in the AMM at time \(t\) in the absence of fees is

\begin{aligned}

K_{\gamma}^{-\frac{N_t}{2}} (Y_t S_t^{\ast} + X_t) &= (X_t Y_t)^{-\frac{1}{2}} (Y_t S_t^{\ast} + X_t)

= 2 (X_t Y_t)^{-\frac{1}{2}} Y_t = 2 (S_t^{\ast})^{\frac{1}{2}}

\end{aligned}

Expected Geometric Return for LPs

\begin{aligned}

\mathbb{E}(\text{log} \ W_t) &= \mathbb{E}(\text{log} (Y_tS_t + X_t)) \\

&= \mathbb{E}(\text{log} (Y_tS^{\ast}_t + X_t)) + \mathbb{E}\left(\text{log} \left(\frac{Y_tS_t + X_t}{Y_tS^{\ast}_t + X_t}\right)\right)

\end{aligned}

- The wealth of LPs at time \(t\) is given as \(W_t = Y_t S_t + X_t\). Expected wealth is

\begin{aligned}

\gamma \le \frac{S_t}{S^{\ast}_t} \le \gamma^{-1}

\implies \gamma \le \left(\frac{Y_tS_t + X_t}{Y_tS^{\ast}_t + X_t}\right) \le \gamma^{-1}

\end{aligned}

But we have,

\(m\) (constant)

\begin{aligned}

\therefore \ \mathbb{E}(\text{log} \ W_t) &= \mathbb{E}(\text{log} (Y_tS^{\ast}_t + X_t)) + m

\end{aligned}

\(\because \ K_{\gamma}^{-\frac{N_t}{2}}(Y_t S_t^{\ast} + X_t) = 2(S_t^{\ast})^{\frac{1}{2}} \)

\begin{aligned}

= \mathbb{E}\left( \text{log} K_{\gamma}^{\frac{N_t}{2}} + \frac{1}{2}\text{log} S_t^{\ast}\right) + m

\end{aligned}

\begin{aligned}

= \left(\frac{\text{log} K_{\gamma}}{2}\right) \mathbb{E}(N_t) + \frac{1}{2} \mathbb{E}(\text{log} S_t^{\ast}) + m

\end{aligned}

Asymptotic Geometric Return for LPs

\begin{aligned}

\therefore \ \lim_{t\to\infty} \frac{\mathbb{E}(\text{log} \ W_t)}{t}

\end{aligned}

\begin{aligned}

= \left(\frac{\text{log} K_{\gamma}}{2}\right) \lim_{t\to\infty} \frac{\mathbb{E}(N_t)}{t} +

\frac{1}{2} \lim_{t\to\infty} \frac{\mathbb{E}(\text{log} S_t^{\ast})}{t}

\end{aligned}

\begin{aligned}

(1 - p)(-\delta) + p\delta = \delta(2p-1)

\end{aligned}

Average number of trades during an interval of time while in the stationary distribution of the Markov chain.

Let \(\pi = \left[\pi(-k_{\gamma}\delta), \dots, \pi(-k_{\gamma}\delta) \right]\)

\(\mathbb{E}(N_t) = nt [(1 - p)\pi(-k_{\gamma}\delta) + p\pi(k_{\gamma}\delta)]\), \(\frac{1}{n}\) is the time interval

\begin{aligned}

\therefore \ \lim_{t\to\infty} \frac{\mathbb{E}(\text{log} \ W_t)}{t}

\end{aligned}

\begin{aligned}

= \left(\frac{\text{log} K_{\gamma}}{2}\right) n[(1 - p)\pi(-k_{\gamma}\delta) + p\pi(k_{\gamma}\delta)] +

\frac{n\delta(2p-1)}{2}

\end{aligned}

Therefore, we finally have a closed form expression for the wealth growth of LPs!

Understanding Volatility Drag

Geometric Brownian Motion

- Stock prices in traditional finance are modeled using GBM

\begin{aligned}

\frac{\Delta S_t}{S_t} = \mu \Delta t + \sigma \sqrt{\Delta t} \varepsilon

\end{aligned}

- \(\mu \Delta t\) - the expected returns of the stock

- \(\sigma \sqrt{\Delta t} \varepsilon\) - models the random fluctuations of the stock price

- On solving the above SDE, we note that \(S_t\) is log-normally distributed

\begin{aligned}

\text{log}\left(\frac{ S_t}{S_0}\right) \sim \mathcal{N}\left(\left(\mu - \frac{\sigma^2}{2}\right)t , \sigma \sqrt{t}\right)

\end{aligned}

Volatility

Random process

Markov process

Drift

Price Process as a GBM

- For the price process \(S_t\) of the asset \(Y_t\), we have

- Mean: \(\mathbb{E}(\text{log}(S_t)) = \delta p + (-\delta)(1 - p) = \delta(2p-1)\)

- Variance: \(\mathbb{V}(\text{log}(S_t)) = \mathbb{E}((\text{log}(S_t))^2) - (\mathbb{E}(\text{log}(S_t)))^2 = \delta^2 - \delta^2(2p-1)^2 = 4\delta^2 p(1-p)\)

- Let us assume that \(\delta\) depends on \(\Delta t = \frac{1}{n}\). For \(S_t\) to be GBM, we must have

S_t =

\begin{cases}

S_{t-1}e^{\delta} & \text{with probability } p \\

S_{t-1}e^{-\delta} & \text{with probability } (1-p)

\end{cases}

\begin{aligned}

\delta_n (2p_n - 1) &= \left(\mu - \frac{\sigma^2}{2} \right)\frac{1}{n} \\

2\delta_n \sqrt{p(1-p)} &= \frac{\sigma}{\sqrt{n}}

\end{aligned}

- Thus, we get \(\delta_n \approx \frac{\sigma}{\sqrt{n}}\) and \(p_n \approx \frac{1}{2} + \frac{d}{2\sigma \sqrt{n}} \) where \(d = \left(\mu - \frac{\sigma^2}{2} \right)\).

LP Wealth Growth

- For a time interval \(\Delta_t = \frac{1}{n}\) and let \(a = \frac{1-p}{p}\), the growth rate of LP wealth is

\begin{aligned}

\lim_{t\to\infty} \frac{\mathbb{E}(\text{log} \ W_t)}{t} =

\begin{cases}

\frac{n\delta}{2} \frac{1}{1 - 2 \frac{\text{log}\gamma}{\delta}} \left(\frac{1 - \gamma}{1 + \gamma}\right) & p = \frac{1}{2} \\[10pt]

\frac{n\delta(2p-1)}{2} \left(\frac{1 \ - \ a \gamma^{-\frac{2}{\delta}\text{log}(a)}}{1 \ + \ a \gamma^{-\frac{2}{\delta}\text{log}(a)}}

\left(\frac{1 - \gamma}{1 + \gamma}\right) + 1\right)

& p > \frac{1}{2}

\end{cases}

\end{aligned}

- The wealth of LP at time \(t\), given by \(W_t = X_t + S_t Y_t\)

- The factor by which the price \(S_t\) can change

- Fee percentage \(1 - \gamma\), note that \(\gamma \rightarrow 1\)

- Substituting \((p_n, \delta_n)\) from previous slide, we can obtain LP wealth growth for a continuous case.

- Case I: \(p = \frac{1}{2} \implies d = 0\). Substituting \(\delta_n = \frac{\sigma}{\sqrt{n}}\) for \(n \rightarrow \infty\)

Convergence to Continuity

\begin{aligned}

\lim_{n\to\infty} \lim_{t\to\infty} \frac{\mathbb{E}(\text{log} \ W_t)}{t} &=

\lim_{n\to\infty} \frac{\sigma\sqrt{n}}{2} \frac{1}{1 - 2 \sqrt{n} \frac{\text{log}\gamma}{\sigma}} \left(\frac{1 - \gamma}{1 + \gamma}\right)

= -\frac{\sigma^2}{4\text{log}(\gamma)} \left(\frac{1 - \gamma}{1 + \gamma}\right)

\end{aligned}

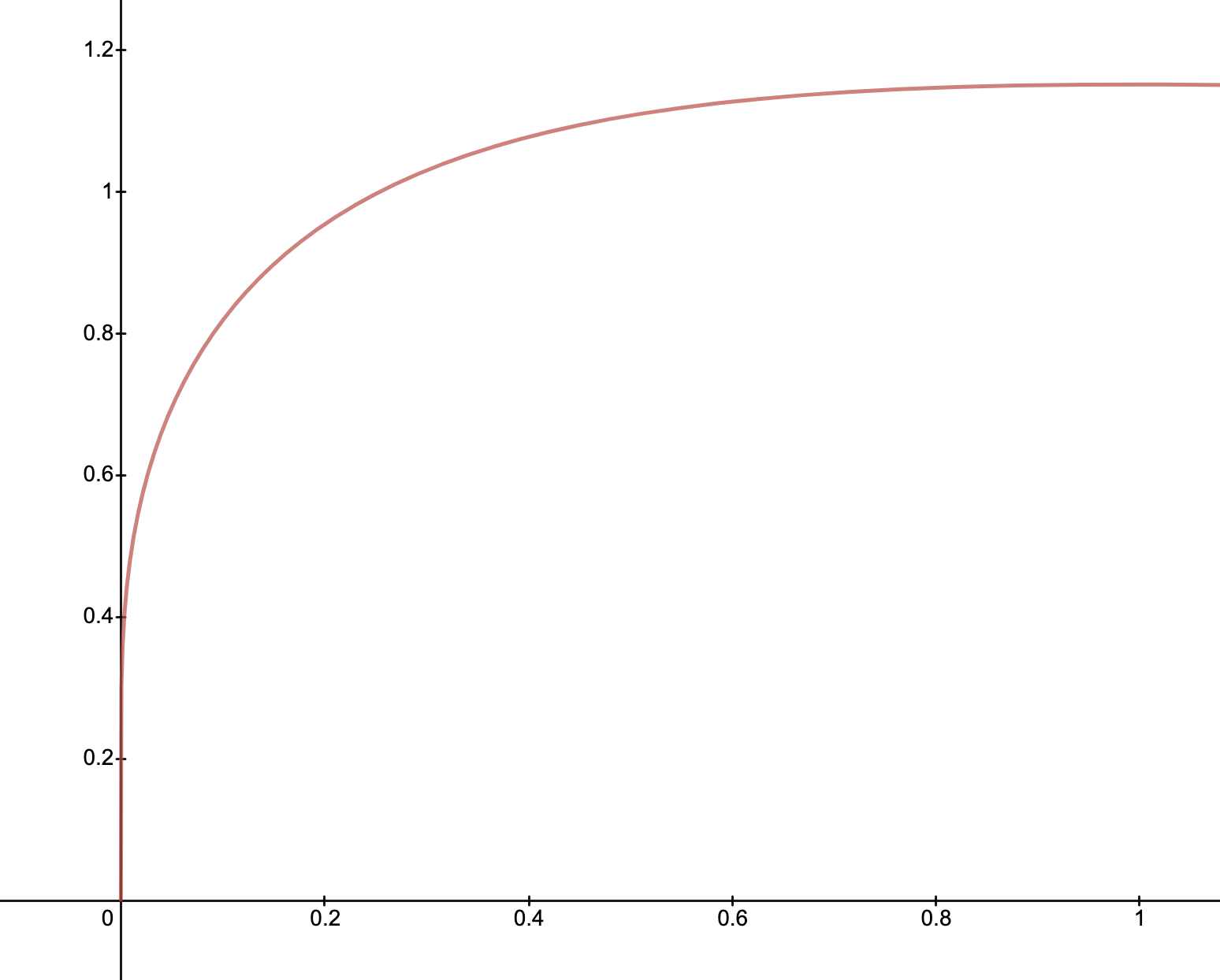

-\frac{1}{\text{log}(\gamma)} \left(\frac{1 - \gamma}{1 + \gamma}\right)

- The LP wealth increases in \(\gamma \in [0,1]\)

- For \(\gamma \rightarrow 1\), the return is

\begin{aligned}

\lim_{\gamma\to1} -\frac{\sigma^2}{4\text{log}(\gamma)} \left(\frac{1 - \gamma}{1 + \gamma}\right) = \frac{\sigma^2}{8}

\end{aligned}

- The un-rebalanced portfolio is zero!

Convergence to Continuity

\begin{aligned}

\lim_{n\to\infty} \lim_{t\to\infty} \frac{\mathbb{E}(\text{log} \ W_t)}{t} &=

\frac{d}{2}

\left(

\left( \frac{1 + \gamma^{\frac{4d}{\sigma^2}}}{1 - \gamma^{\frac{4d}{\sigma^2}}} \right)

\left(\frac{1 - \gamma}{1 + \gamma}\right)

+ 1

\right)

\end{aligned}

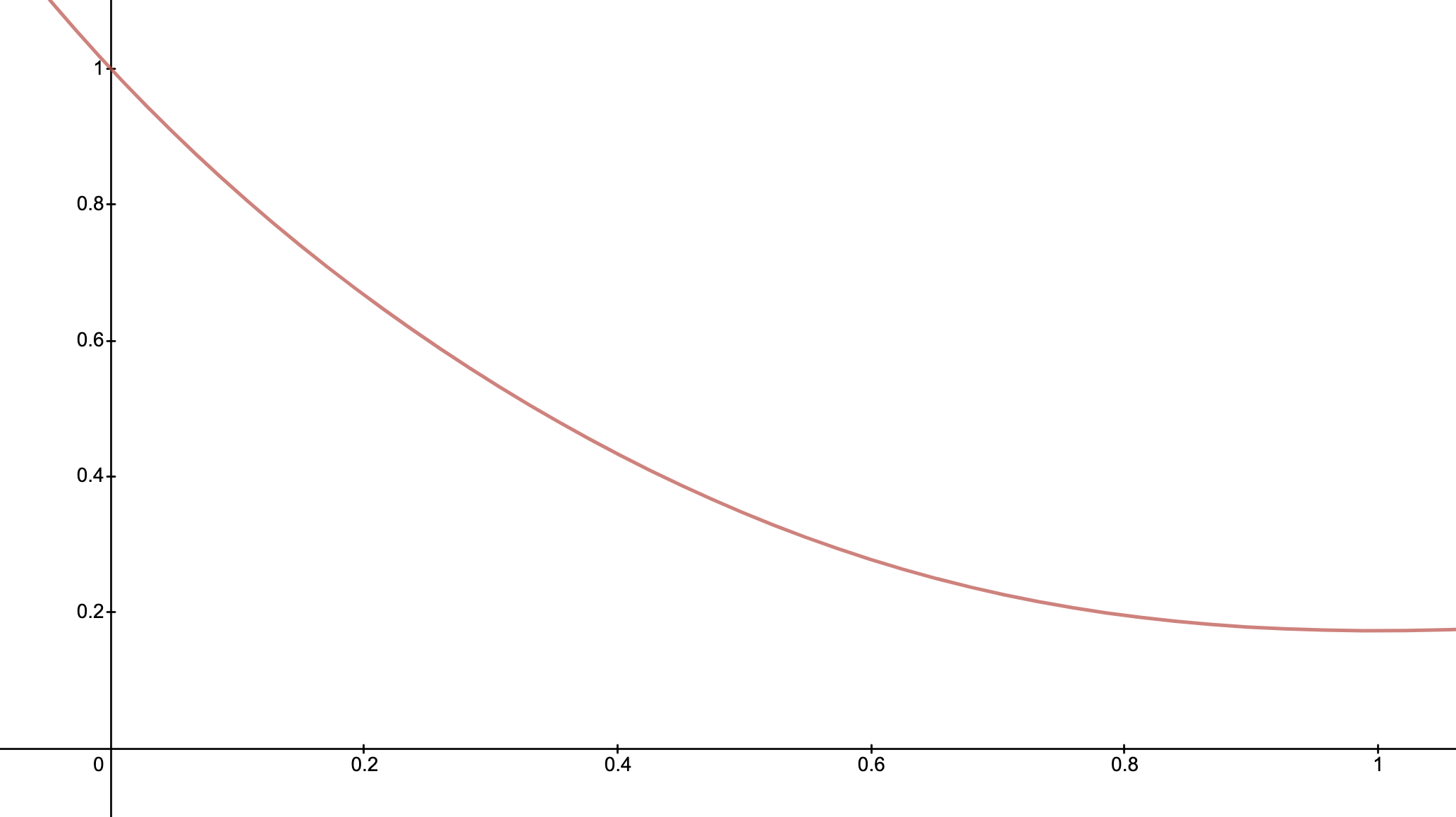

- Case II: \(p > \frac{1}{2}\). Substituting \(p_n\) and \(\delta_n\)

- The LP wealth decreases in \(\gamma \in [0,1]\) if \(4d > \sigma^2\). \(\gamma \rightarrow 0\) gives best possible growth \(d\).

- The wealth increases in \(\gamma \in [0,1]\) if \(4d < \sigma^2\). \(\gamma \rightarrow 1\) gives best growth \(\frac{d}{2} + \frac{\sigma^2}{8}\).

\begin{aligned}

\left( \frac{1 + \gamma^{\frac{4d}{\sigma^2}}}{1 - \gamma^{\frac{4d}{\sigma^2}}} \right)

\left(\frac{1 - \gamma}{1 + \gamma}\right)

\end{aligned}

\(\frac{4d}{\sigma^2} > 1\)

\(\frac{4d}{\sigma^2} < 1\)

Summary

\(p = \frac{1}{2}\)

\(p > \frac{1}{2}\)

HOLDers

LPs

\(0\)

\(\mu - \frac{\sigma^2}{2}\)

\(3\sigma^{2}> 4\mu\)

\(3\sigma^{2} < 4\mu\)

\(\frac{\sigma^2}{8}\)

\(\frac{1}{2}\left(\mu - \frac{\sigma^2}{4}\right)\)

\(3\sigma^{2}= 4\mu\)

\(\mu - \frac{\sigma^2}{2}\)

\(\mu - \frac{\sigma^2}{2}\)

- Therefore, LPs always do either equal or better than HODLers!

- For LPs to always do better, we must that: \(3\sigma^2 > 4\mu\) and \(\mu > \frac{\sigma^2}{4}\). Thus,

\begin{aligned}

\frac{4\mu}{3} < \sigma^2 < 4\mu \ \implies \ \frac{2}{3} < \frac{\sigma^2/2}{\mu} < 2

\end{aligned}

Volatility Drag

- When \(p > 0.5\), the expected growth rate of the price of the asset is

\begin{aligned}

G_{\text{HODL}} = \mu - \frac{\sigma^2}{2}

\end{aligned}

- Here the term \(-\frac{\sigma^2}{2}\) is known as the volatility drag.

- In the same case of \(p > 0.5\), if we have \(\frac{2\sqrt{\mu}}{\sqrt{3}} < \sigma < 2\sqrt{\mu},\) we have

\begin{aligned}

G_{\text{LP}} = \frac{1}{2}\left(\mu - \frac{\sigma^2}{4}\right) > G_{\text{HODL}}

\end{aligned}

Within that range, being a Uniswap LP will eventually make you rich, and in fact richer than you could become by holding any unrebalanced portfolio consisting of cash and the asset.

- LP Wealth paper Authors

Uniswap LP Growth and Volatility Drag

By Suyash Bagad

Uniswap LP Growth and Volatility Drag

Some deep diving about the volatility drag in prices in Uniswap.