Online Learning via Prediction with Experts' Advice

Victor Sanches Portella

UBC - CS

June 2022

Experts' Problem and Online Learning

Prediction with Experts' Advice

Player

Adversary

\(n\) Experts

0.5

0.1

0.3

0.1

Probabilities

x_t

1

0

0.5

0.3

Costs

\ell_t

Player's loss:

\langle \ell_t, x_t \rangle

Adversary knows the strategy of the player

Picking a random expert

vs

Picking a probability vector

Measuring Player's Perfomance

\displaystyle

\mathrm{Regret}(T) = \sum_{t = 1}^T \langle \ell_t, x_t \rangle - \min_{i = 1, \dotsc, n} \sum_{t = 1}^T

\ell_t(i)

\displaystyle

\sum_{t = 1}^T \langle \ell_t, x_t \rangle

Total player's loss

Can be = \(T\) always

\displaystyle

\sum_{t = 1}^T \langle \ell_t, x_t \rangle - \sum_{t = 1}^T \min_{i = 1, \dotsc, n} \ell_t(i)

Compare with offline optimum

Almost the same as Attempt #1

Restrict the offline optimum

\displaystyle

\frac{\mathrm{Regret}(T) }{T} \to 0

Attempt #1

Attempt #2

Attempt #3

Loss of Best Expert

Player's Loss

Goal:

Example

Cummulative Loss

Experts

0

1

0.5

1

t = 1

1

1.5

0.5

1

t = 2

1.5

2

1

1.5

t = 3

2.5

3

2

1.5

t = 4

General Online Learning

Player

Adversary

Player's loss:

x_t \in \mathcal{X}

f_t(\cdot)

Convex

f_t(x_t)

The player sees \(f_t\)

\mathcal{X} = \Delta_n

Simplex

f_t(x) = \langle \ell_t, x \rangle

Linear functions

Some usual settings:

\mathcal{X} = \mathbb{R}^n

\mathcal{X} = \mathrm{Ball}

f_t(x) = \lVert Ax - b \rVert^2

f_t(x) = - \log \langle a, x \rangle

Experts' problem

Why Online Learning?

Traditional ML optimization makes stochastic assumptions on the data

OL strips away the stochastic layer

Traditional ML optimization makes stochastic assumptions on the data

Less assumptions \(\implies\) Weaker guarantees

Less assumptions \(\implies\) More robust

Adaptive algorithms

AdaGrad

Adam

Parameter Free algorithms

Coin Betting

Meta-optimization

Algorithms

Follow the Leader

Idea: Pick the best expert at each round

x_t = e_i = \begin{pmatrix}0\\ 0 \\ 1 \\ 0 \end{pmatrix}

where \(i\) minimizes

\displaystyle \sum_{s = 1}^t \ell_t(i)

Can fail badly

Player loses \(T -1\)

Best expert loses \(T/2\)

Works very well for quadratic losses

0

1

1

0

0

1

1

0

0

1

1

0

0

1

1

0

* picking distributions instead of best expert

Gradient Descent

\displaystyle x_{t+1} = \mathrm{Proj}_{\Delta_n} (x_t - \eta_t \ell_t)

\(\eta_t\): step-size at round \(t\)

\(\ell_t\): loss vector at round \(t\)

= \nabla f_t(x)

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{2 T n}

Sublinear Regret!

Optimal dependency on \(T\)

Can we improve the dependency on \(n\)?

Yes, and by a lot

Multiplicative Weights Update Method

\displaystyle x_{t+1}(i) \propto x_t(i) \cdot e^{- \eta \ell_t(i)}

\displaystyle x_{t+1}(i) \propto x_t(i)\cdot (1 - \eta \ell_t(i))

Normalization

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{2 T \ln n}

Exponential improvement on \(n\)

Optimal

Other methods had clearer "optimization views"

Rediscovered many times in different fields

This one has an optimization view as well!

Follow the Regularized Leader

p_{t+1} = \displaystyle \mathrm{arg}\,\mathrm{min} \sum_{i = 1}^t \langle\ell_t, p \rangle + R(x)

\displaystyle p \in \Delta_n

Regularizer

"Stabilizes the algorithm"

R(x) = \frac{1}{\eta 2} \lVert x \rVert_2^2

\implies

"Lazy" Gradient Descent

R(x) = \sum_i x_i \ln x_i

\implies

Multiplicative Weights Update

Good choice of \(R\) depends of the functions and the feasible set

Online Mirror Descent

- \nabla f_t(x_t)

X

x_t

x_{t+1}

projection

Online Mirror Descent

x_t

\nabla R(x_t)

Dual

Primal

X

\nabla R

- \nabla f_t(x_t)

\nabla R^{-1}

\Pi_X^R

Bregman

Projection

x_{t+1}

Regularizer

R(x) = \frac{1}{\eta 2} \lVert x \rVert_2^2

GD:

R(x) = \sum_i x_i \ln x_i

MWU:

OMD and FTRL are quite general

Applications

Approximately Solving Zero-Sum Games

\begin{pmatrix} -1 & 0.7 \\ 1 & -0.5 \end{pmatrix}

Payoff matrix \(A\) of row player

Row player

Column player

Strategy \(p = (0.1~~0.9)\)

Strategy \(q = (0.3~~0.7)\)

Von Neumman min-max Theorem:

\mathbb{E}[A_{ij}] = p^{T} A q

\displaystyle

\max_p \min_q p^T A q = \min_q \max_p p^T A q = \mathrm{OPT}

Row player

picks row \(i\) with probability \(p_i\)

Column player

picks column \(j\) with probability \(q_j\)

Row player

gets \(A_{ij}\)

Column player

gets \(-A_{ij}\)

Approximately Solving Zero-Sum Games

Main idea: make each row of \(A\) be an expert

For \(t = 1, \dotsc, T\)

\(p_1 =\) uniform distribution

Loss vector \(\ell_t\) is the \(j\)-th col. of \(-A\)

Get \(p_{t+1}\) via Multiplicative Weights

Thm:

\displaystyle

\mathrm{OPT} - \tfrac{1}{T}\mathrm{Regret}(T) \leq \bar{p}^T A \bar{q} \leq \mathrm{OPT} + \tfrac{1}{T}\mathrm{Regret}(T)

Cor:

\displaystyle

T \geq \frac{2 \ln n}{\varepsilon^2} \implies

\displaystyle

\mathrm{OPT} - \varepsilon \leq \bar{p}^T A \bar{q} \leq \mathrm{OPT} + \epsilon

where \(j\) maximizes \(p_t^T A e_j\)

\(q_t = e_j\)

\(\bar{p} = \tfrac{1}{T} \sum_{t} p_t\)

\(\bar{q} = \tfrac{1}{T} \sum_{t} q_t\)

and

Boosting

Training set

\displaystyle

S = \{(x_1, y_1), (x_2, y_2), \dotsc, (x_n, y_n)\}

Hypothesis class

\displaystyle

\mathcal{H}

of functions

\displaystyle

\mathcal{X} \to \{0,1\}

\displaystyle

x_i \in \mathcal{X}

\displaystyle

y_i \in \{0,1\}

Weak learner:

\displaystyle

\mathrm{WL}(p, S) = h \in \mathcal{H}

such that

\displaystyle

\mathbb{P}_{i \sim p}[h(x_i) = y_i] \geq \frac{1}{2} + \gamma

Question: Can we get with high probability a hypothesis* \(h^*\) such that

\displaystyle

h(x_i) \neq y_i

only on a \(\varepsilon\)-fraction of \(S\)?

Generalization follows if \(\mathcal{H}\) is simple (and other conditions)

Boosting

For \(t = 1, \dotsc, T\)

\(p_1 =\) uniform distribution

\(\ell_t(i) = 1 - 2|h_t(x_i) - y_i|\)

Get \(p_{t+1}\) via Multiplicative Weights (with right step-size)

\(h_t = \mathrm{WL}(p_t, S)\)

\(\bar{h} = \mathrm{Majority}(h_1, \dotsc, h_T)\)

Theorem

If \(T \geq (2/\gamma^2) \ln(1/\varepsilon)\), then \(\bar{h}\) makes at most \(\varepsilon\) mistakes in \(S\)

Main ideas:

Regret only against distrb. on examples that \(\bar{h}\) errs

Due to WL property, loss of the player is \(\geq 2 T \gamma\)

\(\ln n\) becomes \(\ln (n/\mathrm{\# mistakes}) \)

Cost of any distribution of this type is \(\leq 0\)

From Electrical Flows to Maximum Flow

\displaystyle

s

\displaystyle

t

Goal:

Route as much flow as possible from \(s\) to \(t\) while respecting the edges' capacities

We can compute in time \(O(|V| \cdot |E|)\)

This year there was a paper with a \(O(|E|^{1 + o(1)})\) alg...

What if we want something faster even if approx.?

From Electrical Flows to Maximum Flow

Fast Laplacian system solvers (Spielman & Teng' 13)

We can compute electrical flows by solving this system

Electrical flows may not respect edge capacities!

Solves

\displaystyle

L x = b

in \(\tilde{O}(|E|)\) time

Laplacian matrix of \(G\)

Main idea: Use electrical flows as a "weak learner", and boost it using MWU!

Edges = Experts

Cost = flow/capacity

Other applications (beyond experts)

Solving Packing linear systems with oracle access

Approximating multicommodity flow

Approximately solve some semidefinite programs

Spectral graph sparsification

Approximating multicommodity flow

Computational complexity (QIP = PSPACE)

Anytime Regret and Stochastic Calculus

Fixed-time vs Anytime

MWU regret

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{2 T \ln n}

when \(T\) is known

\displaystyle

\mathrm{Regret}(T) \leq 2\sqrt{T \ln n}

when \(T\) is not known

\displaystyle

\Bigg\{

anytime

fixed-time

Does knowing \(T\) gives the player an advantage?

Mirror descent in anytime can fail terribly

[Huang, Harvey, VSP, Friedlander]

Optimum for 2 experts anytime is worse

[Harvey, Liaw, Perkins, Randhawa]

Similar techniques also work for fixed-time

[Greenstreet, Harvey, VSP]

Continuous-time experts show interesting behaviour

[VSP, Liaw, Harvey]

Random Experts' Costs

What happens when we randomize experts' losses?

\displaystyle

\ell_t(i) =

\begin{cases}

1 &\text{w.p.}~1/2\\

-1 &\text{w.p.}~1/2

\end{cases}

\displaystyle

L_t(i)

Culmulative loss

of expert \(i\) is a random walk

independently

Worst-case adversary:

\displaystyle

\mathbb{E}[\mathrm{Regret}(T) ] \geq \sqrt{2 T \ln n} - o(1)

Regret bound hold with probability 1

\displaystyle

\implies

Regret bound against any adversary

Idea: Move to continuous time to use powerful stochastic calculus tools

Worked very well with 2 experts

Moving to Continuous Time

Moving to continuous time:

Random walk \(\longrightarrow\) Brownian Motion

\displaystyle

L_t(i) =B_i(t)

\displaystyle

B_1, \dotsc, B_n

are Independent Brownian motions

where

Moving to Continuous Time

Discrete time

Continuous time

\displaystyle

\mathrm{Regret}(t) = A(t) - \min_{i} L_t(i)

\displaystyle

R_i(t) = A(t) - L_t(i)

\displaystyle

L_t(i) =B_i(t)

\displaystyle

L_t(i) =S_i(t)

Cummulative loss

Player's cummulative loss

\displaystyle

\sum_{t = 1}^T\langle p(t), \Delta L(t)\rangle

\displaystyle

\int_0^T\langle p(t), \mathrm{d} L(t) \rangle

\displaystyle

A(t)

\displaystyle

A(t)

Player's loss per round

\displaystyle

\langle p(t), \Delta L(t)\rangle

\displaystyle

\langle p(t), \ell(t)\rangle

\displaystyle

\langle p(t), \mathrm{d} L(t) \rangle

MWU in Continuous Time

Potential based players

\displaystyle

p(t) \propto \nabla \Phi(t, R(t))

\displaystyle

\Phi(t, R(t)) = \ln \left( \sum_{i} e^{-\eta_t R_i(t)} \right)

\displaystyle

p(t) \propto e^{-\eta_t L_t(i)}

\displaystyle

\implies

Regret bounds

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{2 T \ln n}

when \(T\) is known

\displaystyle

\mathrm{Regret}(T) \leq 2\sqrt{T \ln n}

when \(T\) is not known

anytime

fixed-time

\displaystyle

\Bigg\{

MWU!

Same as discrete time!

Idea: Use stochastic calculus to guide the algorithm design

with prob. 1

New Algorithms in Continuous Time

Potential based players

\displaystyle

p(t) \propto \nabla \Phi(t, R(t))

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{2 T \ln n}(1 + o(1))

Matches fixed-time!

Stochastic calculus suggests pontential that satisfy the Backwards Heat Equation

\;\;\;\;\Phi + \;\;\;\;\;\;\; \Phi = 0

\displaystyle

\partial_t

\displaystyle

\tfrac{1}{2}\partial_{gg}

This new algorithm has good regret!

Does not translate easily to discrete time

need to add correlation between experts

New algorithms with good quantile regret bounds!

Fixed-time vs Anytime is still open!

Online Learning via Prediction with Experts' Advice

Victor Sanches Portella

UBC - CS

June 2022

Kitchen Sink

Simplifying Assumptions

We will look only at \(\{0,1\}\) costs

1

0

0

1

0

0

1

1

Equal costs do not affect the regret

Cover's algorithm relies on these assumptions by construction

Our alg. and analysis extends to fractional costs

Gap between experts

Thought experiment: how much probability mass to put on each expert?

Cumulative Loss on round \(t\)

\(\frac{1}{2}\) is both cases seems reasonable!

Takeaway: player's decision may depend only on the gap between experts's losses

Gap = |42 - 20| = 22

Worst Expert

Best Expert

42

20

2

2

42

42

(and maybe on \(t\))

Cover's Dynamic Program

Player strategy based on gaps:

Choice doesn't depend on the specific past costs

p(t, g)

on the Worst expert

1 - p(t, g)

on the Best expert

We can compute \(V^*\) backwards in time via DP!

\displaystyle

V^*[t, g] =

Max regret to be suffered at time \(t\) with gap \(g\)

\(O(T^2)\) time to compute \(V^*\)

At round \(t\) with gap \(g\)

\displaystyle

V^*[0, 0] =

Max. regret for a game with \(T\) rounds

Computing the optimal strategy \(p^*\) from \(V^*\) is easy!

Cover's DP Table

(w/ player playing optimally)

Cover's Dynamic Program

Player strategy based on gaps:

Choice doesn't depend on the specific past costs

p(t, g)

on the Lagging expert

1 - p(t, g)

on the Leading expert

We can compute \(V^*\) backwards in time via DP!

Getting an optimal player \(p^*\) from \(V^*\) is easy!

\displaystyle

V^*[t, g] =

Max regret-to-be-suffered at round \(t\) with gap \(g\)

\(O(T^2)\) time to compute the table — \(O(T)\) amortized time per round

p^*(t,g) = \frac{1}{2} \big( V^*[t, g-1] - V^*[t, g+1]\big)

At round \(t\) with gap \(g\)

\displaystyle

V^*[0, 0] =

Optimal regret for 2 experts

Connection to Random Walks

Optimal player \(p^*\) is related to Random Walks

\displaystyle

p^*(t,g)

For \(g_t\) following a Random Walk

\displaystyle

\approx\mathbb{P}\Big(\mathcal{N}(0,T - t) > g\Big)

Central Limit Theorem

Not clear if the approximation error affects the regret

The DP is defined only for integer costs!

Lagging expert finishes leading

= \mathbb{P} \Big(

\Big)

Let's design an algorithm that is efficient and works for all costs

Bonus: Connections of Cover's algorithm with stochastic calculus

Connection to Random Walks

Theorem

\displaystyle

\Big]

\displaystyle

= \sqrt{\frac{T}{2\pi}} + O(1)

Player \(p^*\) is also connected to RWs

\displaystyle

p^*(t,g)

For \(g_t\) following a Random Walk

\displaystyle

\approx\mathbb{P}\Big(\mathcal{N}(0,T - t) > g\Big)

Central Limit Theorem

Not clear if the approximation error affects the regret

The DP is defined only for integer costs!

\displaystyle

V^*[0,0] =

\displaystyle

\frac{1}{2}

\displaystyle

\mathbb{E}\Big[

Lagging expert finishes leading

= \mathbb{P} \Big(

\Big)

[Cover '67]

# of 0s of a Random Walk of len \(T\)

Let's design an algorithm that is efficient and works for all costs

Bonus: Connections of Cover's algorithm with stochastic calculus

Discrete Itô's Formula

\displaystyle

R(T, |B_T|) - R(0, 0) = \displaystyle

\mathrm{ContRegret}(\partial_g R, T) + \int_{0}^T \overset{*}{\Delta} R(t, |B_t|) \mathrm{d}t

\displaystyle

R(T, g_T) - R(0, 0) =\;\;\; \mathrm{Regret}(R_g, T)

How to analyze a discrete algorithm coming from stochastic calculus?

Discrete Itô's Formula!

\displaystyle

+ \sum_{t = 1}^T \Big(R_t(t, g_t) + \frac{1}{2} R_{gg}(t, g_t)\Big)

Discrete Derivatives

Surprisingly, we can analyze Cover's algorithm with discrete Itô's formula

Itô's Formula

Discrete Itô's Formula

Discrete Algorithms

p^*(t,g)

= V_g^*[t,g]

V_t^*[t, g] + \frac{1}{2} V_{gg}^*[t,g] = 0

\(V^*\) satisfies the "discrete" Backwards Heat Equation!

Not Efficient

Efficient

Discrete Itô \(\implies\)

Regret of \(p^* \leq V^*[0,0]\)

BHE = Optimal?

Hopefully, \(R\) satisfies the discrete BHE

Discretized player:

R_g(t,g)

We show the total is \(\leq 1\)

Cover's strategy

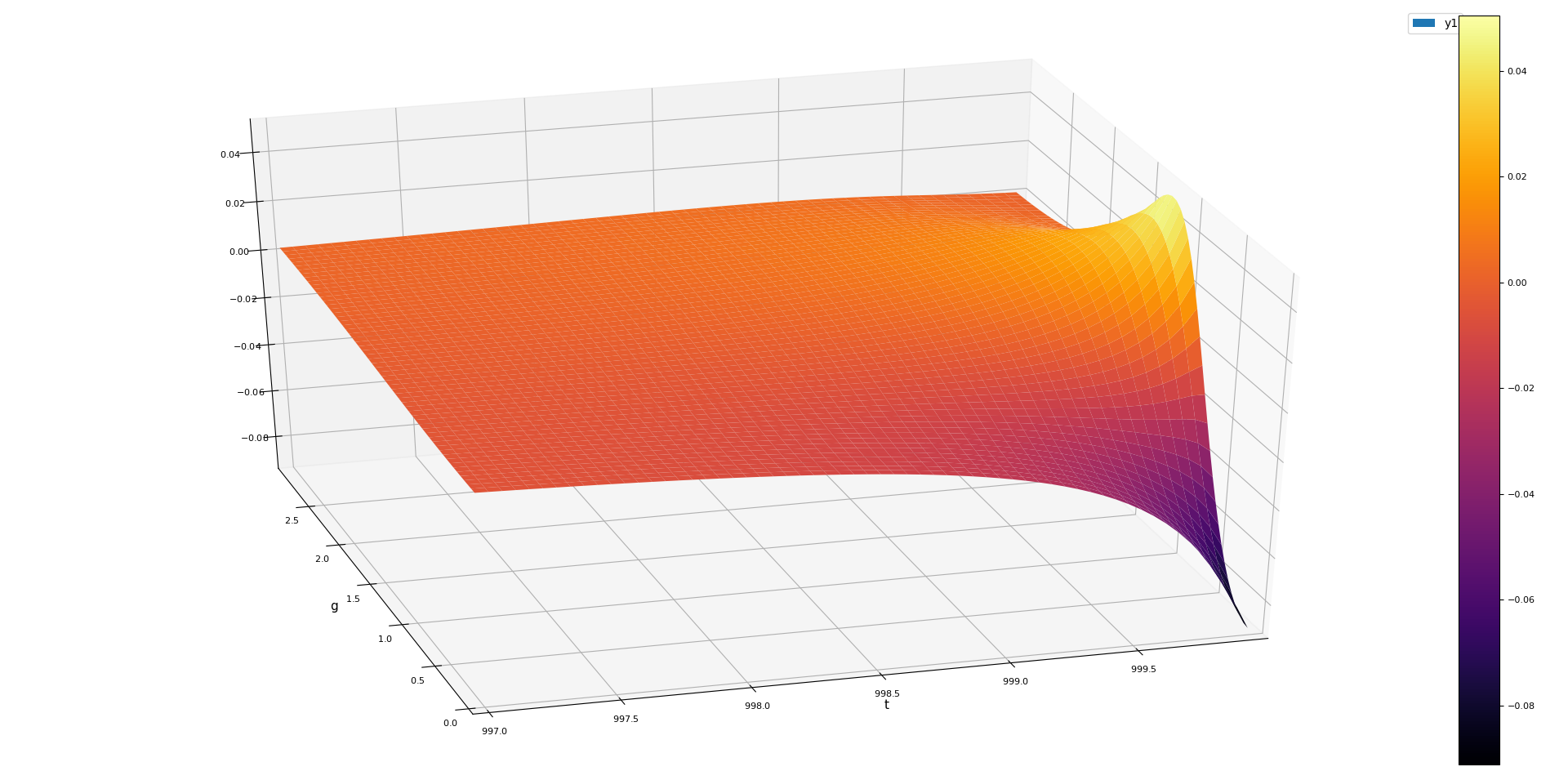

Bounding the Discretization Error

In the work of Harvey et al., they had

In this fixed-time solution, we are not as lucky.

Negative discretization error!

g

t

T = 1000

We show the total discretization error is always \(\leq 1\)

A Probabilistic View of Regret Bounds

Formula for the regret based on the gaps

\displaystyle

\mathrm{Regret(T)}

= \sum_{t = 1}^{T}

p(t, g_{t-1})(g_t - g_{t-1})

Random walk \(\longrightarrow\) Brownian Motion

\displaystyle

\mathrm{ContRegret(p, T)}

= \int_{0}^{T}

p(t, |B_t|)\mathrm{d}|B_t|

Reflected Brownian motion (gaps)

Conditions on the continuous player \(p\)

Continuous on \([0,T) \times \mathbb{R}\)

p(t,0) = \frac{1}{2}

for all \(t \geq 0\)

Stochastic Integrals and Itô's Formula

How to work with stochastic integrals?

\displaystyle

R(T, |B_T|) - R(0, 0) =

Itô's Formula:

\(\overset{*}{\Delta} R(t, g) = 0\) everywhere

ContRegret \( = R(T, |B_T|) - R(0,0)\)

\displaystyle

\implies

Goal:

Find a "potential function" \(R\) such that

(1) \(\partial_g R\) is a valid continuous player

(2) \(R\) satisfies the Backwards Heat Equation

\displaystyle

+ \int_{0}^T \overset{*}{\Delta} R(t, |B_t|) \mathrm{d}t

Different from classic FTC!

\displaystyle

\mathrm{ContRegret}(\;\;\;\;\;\;, T)

\displaystyle

\partial_g R

\;\;\; \vphantom{\overset{*}{\Delta}} R = \;\;\;R + \;\;\;\;\;\;\; R

\displaystyle

\partial_t

\displaystyle

\tfrac{1}{2}\partial_{gg}

\displaystyle

\overset{*}{\Delta}

Backwards Heat Equation

Stochastic Integrals and Itô's Formula

\displaystyle

R(T, |B_T|) - R(0, 0) =

Goal:

Find a "potential function" \(R\) such that

(1) \(\partial_g R\) is a valid continuous player

(2) \(R\) satisfies the Backwards Heat Equation

\displaystyle

\mathrm{ContRegret}(\;\;\;\;\;\;, T)

\displaystyle

\partial_g R

How to find a good \(R\)?

?

Suffices to find a player \(p\) satisfying the BHE

p(t,g) = \mathbb{P}(\mathcal{N}(0, T - t) > g)

\(\approx\) Cover's solution!

Also a solution to an ODE

\displaystyle R(T, |B_T|) - R(0,0) \leq \sqrt{\frac{T}{2\pi}}

R(t,g) \approx \int p(t,g)

Then setting

preserves BHE and

p = \partial_g R

Stochastic Integrals and Itô's Formula

How to work with stochastic integrals?

\displaystyle

R(T, |B_T|) - R(0, |B_0|) = \int_{0}^T \partial_g R(t, |B_t|) \mathrm{d}|B_t|

Itô's Formula:

\(\overset{*}{\Delta} R(t, g) = 0\) everywhere

ContRegret is given by \(R(T, |B_T|)\)

\displaystyle

\implies

Goal:

Find a "potential function" \(R\) such that

(1) \(\partial_g R\) is a valid continuous player

(2) \(R\) satisfies the Backwards Heat Equation

\displaystyle

+ \int_{0}^T \overset{*}{\Delta} R(t, |B_t|) \mathrm{d}t

Different from classic FTC!

\displaystyle

\mathrm{ContRegret}(\;\;\;\;\;\;, T)

\displaystyle

\partial_g R

\;\;\; \vphantom{\overset{*}{\Delta}} R = \;\;\;R + \;\;\;\;\;\;\; R

\displaystyle

\partial_t

\displaystyle

\tfrac{1}{2}\partial_{gg}

\displaystyle

\overset{*}{\Delta}

Backwards Heat Equation

[C-BL 06]

Our Results

An Efficient and Optimal Algorithm in Fixed-Time with Two Experts

Technique:

Solve an analogous continuous-time problem, and discretize it

[HLPR '20]

How to exploit the knowledge of \(T\)?

Discretization error needs to be analyzed carefully.

BHE seems to play a role in other problems in OL as well!

Solution based on Cover's alg

Or inverting time in an ODE!

We show \(\leq 1\)

\(V^*\) and \(p^*\) satisfy the discrete BHE!

Insight:

Cover's algorithm has connections to stochastic calculus!

Questions?

Known Results

Multiplicative Weights Update method:

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{\frac{T}{2} \ln n}

Optimal for \(n,T \to \infty\) !

If \(n\) is fixed, we can do better

\(n = 2\)

\(n = 3\)

\(n = 4\)

\sqrt{\frac{T}{2\pi}} + O(1)

\sqrt{\frac{8T}{9\pi}} + O(\ln T)

\sim \sqrt{\frac{T \pi}{8}}

Player knows \(T\) !

Minmax regret in some cases:

What if \(T\) is not known?

\displaystyle

\frac{\gamma}{2} \sqrt{T}

Minmax regret

\(n = 2\)

[Harvey, Liaw, Perkins, Randhawa FOCS 2020]

They give an efficient algorithm!

\displaystyle

\gamma \approx 1.307

A Dynamic Programming View

Optimal regret (\(V^* = V_{p^*}\))

\displaystyle

V^*[t,g] = \frac{1}{2}(V^*[t+1, g-1] + V^*[t+1, g + 1])

\displaystyle

V^*[t,0] = \frac{1}{2} + V^*[t+1, 1]

For \(g > 0\)

For \(g = 0\)

g

t

4

3

2

1

0

0

0

0

0

0

0

0

\frac{1}{2}

0

0

0

0

0

0

0

0

0

0

0

0

0

1

2

3

Regret and Player in terms of the Gap

Path-independent player:

If

round \(t\) and gap \(g_{t-1}\) on round \(t-1\)

p(t, g_{t-1})

1 - p(t, g_{t-1})

on the Lagging expert

on the Leading expert

Choice doesn't depend on the specific past costs

p(t, 0) = 1/2

for all \(t\), then

\displaystyle

\mathrm{Regret(T)}

= \sum_{t = 1}^{T}

p(t, g_{t-1})(g_t - g_{t-1})

gap on round \(t\)

A discrete analogue of a Riemann-Stieltjes integral

A formula for the regret

A Dynamic Programming View

\displaystyle

V_p[t, g] =

Maximum regret-to-be-suffered on rounds \(t+1, \dotsc, T\) when gap on round \(t\) is \(g\)

Path-independent player \(\implies\) \(V_p[t,g]\) depends only on \(\ell_{t+1}, \dotsc, \ell_T\) and \(g_t, \dotsc, g_{T}\)

\displaystyle

V_p[t, 0] = \max\{p(t+1,0), 1 - p(t+1,0)\} + V_p[t+1, 1]

Regret suffered on round \(t+1\)

Regret suffered on round \(t + 1\)

\displaystyle

V_p[t, g] = \max \Bigg\{

\displaystyle

V_p[t+1, g+1] + p(t + 1,g)

\displaystyle

V_p[t+1, g-1] - p(t + 1,g)

A Dynamic Programming View

\displaystyle

V_p[t, g] =

Maximum regret-to-be-suffered on rounds \(t+1, \dotsc, T\) if gap at round \(t\) is \(g\)

We can compute \(V_p\) backwards in time!

Path-independent player \(\implies\)

\(V_p[t,g]\) depends only on \(\ell_{t+1}, \dotsc, \ell_T\) and \(g_t, \dotsc, g_{T}\)

We then choose \(p^*\) that minimizes \(V^*[0,0] = V_{p^*}[0,0]\)

\displaystyle

V_p[0, 0] =

Maximum regret of \(p\)

A Dynamic Programming View

For \(g > 0\)

\displaystyle

p^*(t,g) = \frac{1}{2}(V_{p^*}[t, g-1] - V_{p^*}[t, g + 1])

Optimal player

\displaystyle

p^*(t,0) = \frac{1}{2}

Optimal regret (\(V^* = V_{p^*}\))

\displaystyle

V^*[t,g] = \frac{1}{2}(V^*[t+1, g-1] + V^*[t+1, g + 1])

For \(g = 0\)

\displaystyle

V^*[t,0] = \frac{1}{2} + V^*[t+1, 1]

For \(g > 0\)

For \(g = 0\)

Discrete Derivatives

p^*(t,g) = \frac{1}{2} \big( V^*[t, g-1] - V^*[t, g+1]\big)

\approx \partial_g V^*[t,g]

\eqqcolon V_g^*[t,g]

V^*[t, g] - V^*[t-1, g]

= \frac{1}{2}( V^*[t, g-1] - V^*[t, g]) - \frac{1}{2}(V^*[t, g] - V^*[t,g+1])

\coloneqq V_t^*[t,g]

\coloneqq \frac{1}{2}V_{gg}^*[t,g]

\partial_t V^*[t,g] \approx

\approx \frac{1}{2}\partial_g V^*[t,g-1]

\approx \frac{1}{2} \partial_g V^*[t,g]

\approx \frac{1}{2} \partial_{gg} V^*[t,g]

Bounding the Discretization Error

Main idea

\(R\) satisfies the continuous BHE

\implies

R_t(t,g) + \frac{1}{2} R_{gg}(t,g) \approx

Approximation error of the derivatives

\implies

\leq 0.74

\displaystyle

\mathrm{Regret(T)} \leq \frac{1}{2} + \sqrt{\frac{T}{2\pi}} + \sum_{t = 1}^T O\Bigg( \frac{1}{(T - t)^{3/2}}\Bigg)

Lemma

\partial_{gg}R(t,g) - R_{gg}(t,g)

\partial_t R(t,g) - R_t(t,g)

\in O\Big( \frac{1}{(T - t)^{3/2}}\Big)

\Bigg\}

Known and New Results

Multiplicative Weights Update method:

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{\frac{T}{2} \ln n}

Optimal for \(n,T \to \infty\) !

If \(n\) is fixed, we can do better

Worst-case regret for 2 experts

Player knows \(T\) (fixed-time)

Player doesn't know \(T\) (anytime)

Question:

Is there an efficient algorithm for the fixed-time case?

Ideally an algorithm that works for general costs!

\(O(T)\) time per round

Dynamic Programming

\(\{0,1\}\) costs

\(O(1)\) time per round

Stochastic Calculus

\([0,1]\) costs

[Harvey, Liaw, Perkins, Randhawa FOCS 2020]

\displaystyle

\approx

0.65 \sqrt{T}

\displaystyle \sqrt{\frac{T}{2\pi}} + O(1)

[Cover '67]

Our Results

Result:

An Efficient and Optimal Algorithm in Fixed-Time with Two Experts

\(O(1)\) time per round

was \(O(T)\) before

\displaystyle

\mathrm{Regret}(T) \leq \sqrt{\frac{T}{2 \pi}} + 1.3

Holds for general costs!

Technique:

Discretize a solution to a stochastic calculus problem

[HLPR '20]

How to exploit the knowledge of \(T\)?

Non-zero discretization error!

Insight:

Cover's algorithm has connections to stochastic calculus!

This connection seems to extend to more experts and other problems in online learning in general!

IAM Student seminar - OL via the Expert's problem

By Victor Sanches Portella