Andreas Park PRO

Professor of Finance at UofT

gold &silver

sterling

USD

???

pre-1800

British imperial trade

post-Bretton Woods

"Pax" Americana

1944-

multi-lateral stablecoins

MXN

USD

THB

Micro-founded mechanism: AMM attracts volume \(\to\) attracts liquidity \(\to\) lowers per-trade costs

Identify parameter region where the AMM designer prefers vehicle routing but cross-pair traders don't

Identify parameter region where multi-asset pool improves vehicle routing; extend to \(n\) small currencies

1

2

3

Our work and this talk is all V2

A pool of reserves + a pricing rule \(R_0\cdot R_1=k\). Three things to know:

① Price = slope

S = R₀ / R₁

② Trade walks the curve

price moves → impact

③ LPs shift it out

more depth, same price

Liquidity pool

\(R_0\) (USD)

\(R_1\) (MXN)

liquidity invariant \[R_0\cdot R_1=k\]

marginal price \[S=\frac{R_0}{R_1}\]

pool depth (at market price)

\[D=R_0+S\cdot R_1=2R_0\]

larger pool \(\to\) smaller price impact

define a trade's price impact:

\[\frac{S^{\text{paid}}-S^{\text{initial}}}{S^{\text{initial}}}\]

\(S^{\text{paid}}\): average rate over the whole trade — the VWAP of "walking" the pool

Proposition: A trade of size \(\Delta\) incurs a price impact of \(\frac{2\Delta}{D}\)

A trade ("swap") moves the price along the curve.

Liquidity providers have no positional gains on a round trip → they earn on AMM fees.

Fees accrue on all volume; adverse selection only on the imbalance.

buy & hold

AMM LP: concave relative to buy & hold

exchange rate change

holding value one currency rel. to other

Proposition: Adverse selection, priced from returns + volume alone.

Our closed form (Learning from DeFi):

\(\mathbb{E}[\text{IL}] = \dfrac{\sigma^2}{8}\)

The AMM fee must cover it.

Constant product (Uniswap) is the prevalent AMM — but other pricing curves exist.

Decentralized Exchanges for Stablecoins · Huang, Rostova & Song

Flatter curves suit same-currency stable pairs (USDT–USDC).

Pool Designer picks fee \(F\)

A protocol parameter, set at the pool level.

LPs commit liquidity until dpeth equates \(F\) to expected IL

Competitive break-even provision \(\to\) equilibrium pool size \(V^*(F)\)

Traders face price impact (liquidity driven) and fee

Deeper pool \(\to\) lower PI for given trade

All-in trading cost = price impact + fee.

The pool designer chooses F to minimize the sum (loose idea: pre-empt entry of competitor).

liquidity is increasing in fee \(\to\) price impact is decreasing in fee \(\to\) interior optimal \(F\)*

*we solve model for exogenous noise volume for simplicity; condition for endogenous volume is that elasticity relative to fee is \(<1\)

Closed-form

from returns + volume, no intraday data

Square-root law

optimal fee \(\approx \sigma\sqrt{\frac{\Delta}{V}}\) — the price-impact law, as adverse-selection compensation

A lower bound

same scale as spreads, ~30% below — prices only adverse selection

AMM as a limit order book

the pricing schedule can be interpreted as a continuous order book

We take this to FX: view passive, competitive V2-style LP as a conservative benchmark for the status quo.

A model of an AMM: the AMM fee that minimizes trading cost (price impact + fee) → a measure of per-period adverse selection, calibrated to equities.

When period volume is large relative to any single trade:

Optimal fee

\[F^{*}=\frac{\sigma}{2}\sqrt{\frac{\Delta}{V}}\]

Pool depth

\[D^{*}=\frac{4}{\sigma}\sqrt{\Delta V}\]

Per-trade cost

\[c^{*}=\sigma\sqrt{\frac{\Delta}{V}}\]

\(\sigma\) = period return volatility — captures adverse selection, reminiscent of the square-root price-impact law

\(V\) = expected "noise" (balanced) volume · \(\Delta\) = representative order size · \(D\) = pool depth

now starts the FX paper; this was the level-setting warm-up

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

Status Quo (SQ)

Two bilateral USD pools. MXN/THB route through USD

Three Bilateral Pools (BP)

One pool per pair. No forced routing but fragmented capital and volume

Single multilateral pool (MP)

all three currencies in one pool; direct trading of all pairs

Same approach as single pool: LP break even, cost-minimizing planner

Split the capital and each pair gets a book only ⅓ as deep — price impact rises. Pool it, and every dollar backs all three pairs.

⅓ D

⅓ D

⅓ D

USD/MXN

USD/THB

MXN/THB

capital split 3 ways

pool the capital →

D

every dollar backs all 3 pairs

price impact, split capital:

\[\frac{2\Delta}{D/3}=\frac{6\Delta}{D}\]

price impact, pooled:

\[\frac{2\Delta}{\frac{2}{3}D}=\frac{3\Delta}{D}\]

liquidity invariant (equal weights) \[R_0\cdot R_1\cdots R_n = k\]

marginal rate vs numeraire \((S_0\equiv 1)\) \[S_i=\frac{R_0}{R_i}\]

pool depth (at market prices) \[D=\sum_i S_i R_i = n\,R_0\]

Lemma (equal thirds). Each currency holds one third of pool depth: \(\;S_i R_i = \dfrac{D}{3}\)

Price impact. A trade \(i\to j\) touches 2 of 3 currencies — backed by \(\tfrac{2}{3}D\):

\[\Pi=\frac{2\Delta}{\frac{2}{3}D}=\frac{3\Delta}{D}\]

Impermanent loss — our closed-form approximation:

\[\mathbb{E}[\text{IL}]=\frac{\Sigma}{18},\quad \Sigma=\sigma_{01}^2+\sigma_{02}^2+\sigma_{12}^2\]

extends bilateral \(\;\sigma^2/8\) · this is what the AMM fee must cover

① LPs commit liquidity

until fee revenue covers expected IL — this pins down depth D.

② Designer picks fee F

to minimize price impact + fee — depth substitutes out, leaving the cost.

\(R_n\)

\(R_0\)

liquidity invariant \[{R_0}^{w_0}\cdot {R_1}^{w_1}\cdot \ldots \cdot {R_n}^{w_n}=k~\text{with}~w_i\ge0 ~\text{and}~\sum_i w_i=1.\]

marginal exchange rate relative to numeraire \(i=0\) and \(S_0=1\)\[S_i=\frac{R_0}{R_i}\]

pool value (at market price)

\[V=\sum_{i=0}^N S_iR_i=NR_0\]

we will use \(w_i=w_j\) for all \(i,j\)*

* we have a 3-currency optimal solutions for the model studied below and in Li, Park, Singh, Veneris (2026) we develop a numerical algorithm for optimal weight and pool contruction

\(R_1\)

\(\ldots\)

Lemma - equal thirds

When pool prices match fundamental value, \(S_i R_i=V/3\) for every currency \(i\).

Proposition - price impact

A trade of \(i\to j\) of size \(\Delta\) incurs price impact \(\frac{3\Delta}{V}\)

USD/MXN

1/3

USD/THB

1/3

TBH/MXN

1/3

USD \(\cdot\) THB \(\cdot\) MXN

every dollar backs all 3 pairs

price impact on any pair: \[\frac{2\Delta}{\frac{1}{3}V_{\text{tot}}}=6\cdot \frac{\Delta}{V_{\text{tot}}}\]

price impact on any pair: \[3\cdot \frac{\Delta}{V_{\text{tot}}}\]

Impermanent loss:

\[\text{IL}=\frac{\text{pool value at }T -\text{pool value buy-and-hold at} T}{\text{pool value at start}}\]

\[=\left(\prod_{i=1}^nx_i\right)^{\frac{1}{n+1}}-\frac{1}{n+1}\left(1+\sum_{i=1}^nx_i\right)\]

gross return of currency i relative to numeraire 0: \[x_i:=\frac{S_i(T)}{S_i(0)}\]

Proposition: For three currencies with \(E[x_i]=1\), \(x_i:=1+\epsilon_i,\), \(\sigma_{ij}^2:=Var(\epsilon_i-\epsilon_j)\), and \(\Sigma:=\sigma_{01}^2+\sigma_{02}^2+\sigma_{12}^2\)

\[\mathbb{E}[-\text{IL}]=\frac{\Sigma}{18}\]

recall: bilateral pool \(\mathbb{E}[\text{IL}]=\frac{\sigma^2}{8}\)

Define \(Q\) as the total expected noise volume in all currencies in terms of the numeraire.

The LP breakeven condition is \[\text{fee}\cdot\text{volume}=\text{initial pool value}\cdot \text{proportional loss}~\Leftrightarrow~f\cdot Q=V_0\cdot\mathbb{E}[-IPL]\]

Loosely, pool designer wants lowest cost to attract volume

The total cost is price impact plus fee

\[c^\text{multi}(f)=\frac{\Delta\Sigma}{6Q}\frac{1}{f}+f~~~~~~c^\text{pair}(f_{ij})=\frac{\Delta \sigma^2_{ij}}{4Q_{ij}}\frac{1}{f_{if}}+f_{ij}\]

\(f^*=\sqrt{\frac{\Delta\Sigma}{6Q}}\)

\(f^*_{ij}=\sqrt{\frac{\Delta\sigma^2_{ij}}{4Q_{ij}}}\)

equilibrium price impact \(\approx\) \(2\times f\)

Proposition: If all three pairs have equal volume and volatilities then multi-pool cost is \(\sqrt{\frac{2}{3}}\) of pairwise

① LPs commit liquidity

until fee revenue covers expected IL — this pins down depth D.

② Designer picks fee F

to minimize price impact + fee — depth substitutes out, leaving the cost.

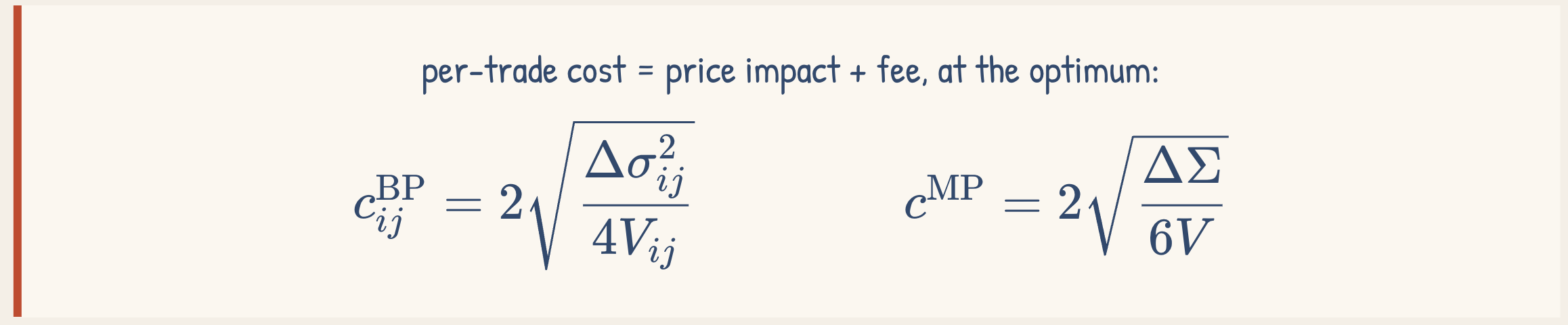

per-trade cost = price impact + fee, at the optimum:

\(c^{\text{BP}}_{ij}=2\sqrt{\dfrac{\Delta\sigma_{ij}^{2}}{4V_{ij}}}\qquad\qquad c^{\text{MP}}=2\sqrt{\dfrac{\Delta\Sigma}{6V}}\)

Symmetric case: \(\;c^{\text{MP}}=\sqrt{\tfrac{2}{3}}\,c^{\text{BP}}\;\) — about 18% lower.

Real FX is not symmetric: dollar pairs dominate volume, cross pairs are (or would be) thinly traded

volume \(V\)

volatility \(\sigma\)

volume \(V\)

volatility \(\sigma\)

volume \(v\times V\)

volatility \(s\times\sigma\)

\(v\) cross-pair volume, relative to a vehicle pair

\(s\) cross-pair volatility, relative to a vehicle pair

— typically \(v<1\), cross pairs are thin

Real FX is not symmetric, dollar pairs dominate volume, cross pairs are (or would be) thinly traded

volume \(Q\)

volatility \(\sigma\)

volume \(Q\)

volatility \(\sigma\)

volume \(v\times Q\)

volatility \(s\times\sigma\)

\(v\) cross-pair volume, relative to a vehicle pair

\(s\) cross-pair volatility, relative to a vehicle pair

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

MXN

USD

THB

Status Quo (SQ)

Two bilateral USD pools. MXN/THB route through USD

Three Bilateral Pools (BP)

One pool per pair. No forced routing but fragmented capital and volume

Single multilateral pool (MP)

all three currencies in one pool; direct trading of all pairs

narket designer considers the volume-weighted costs for all groups

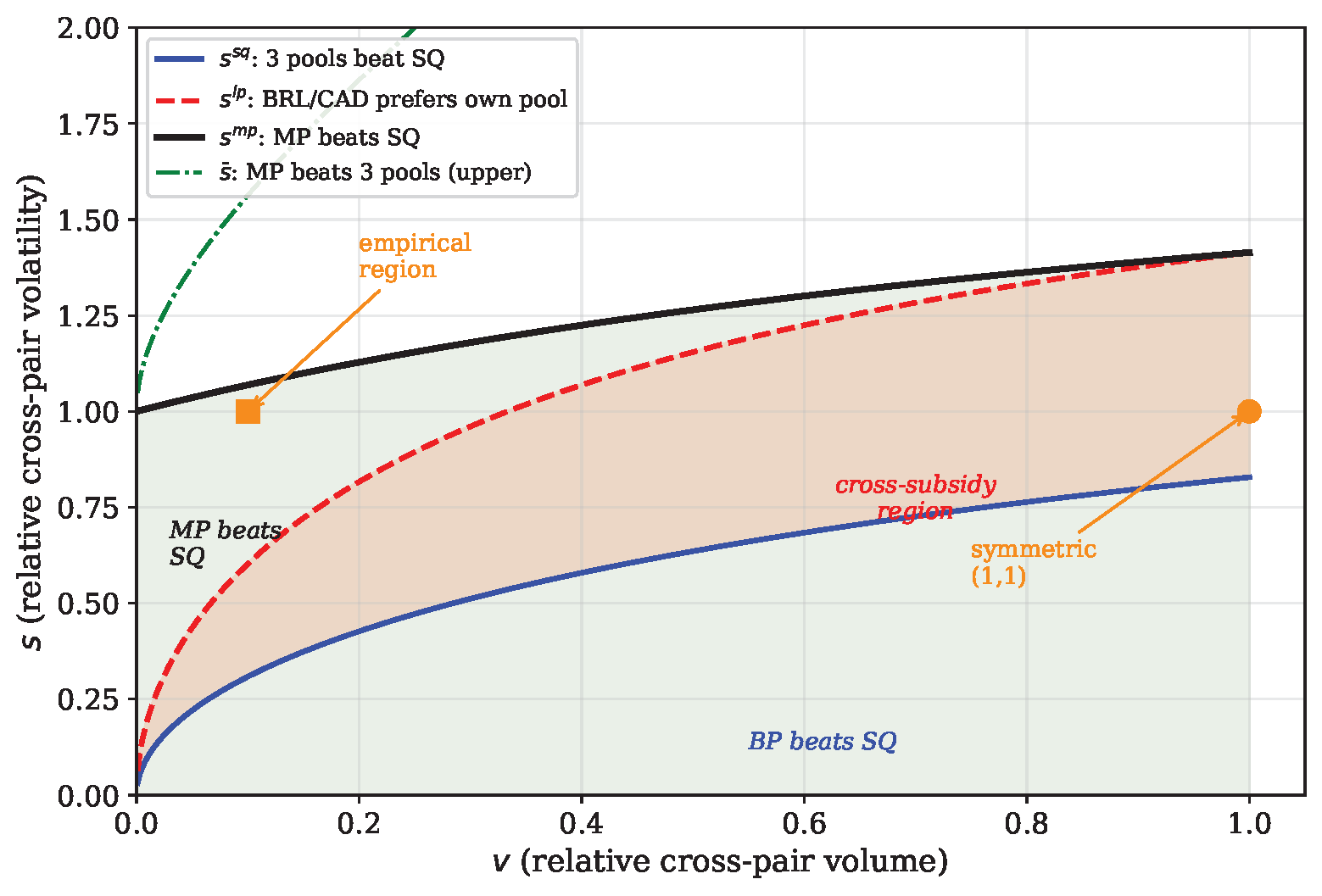

multi-currency pool is better than three bilateral pools

vehicle routing beats three pools

three bilateral pools are better than vehicle routing

multi-currency pool beats vehicle routing

but: small traders would prefer their own pool

MXN/THB

Many small currencies: which to pool?

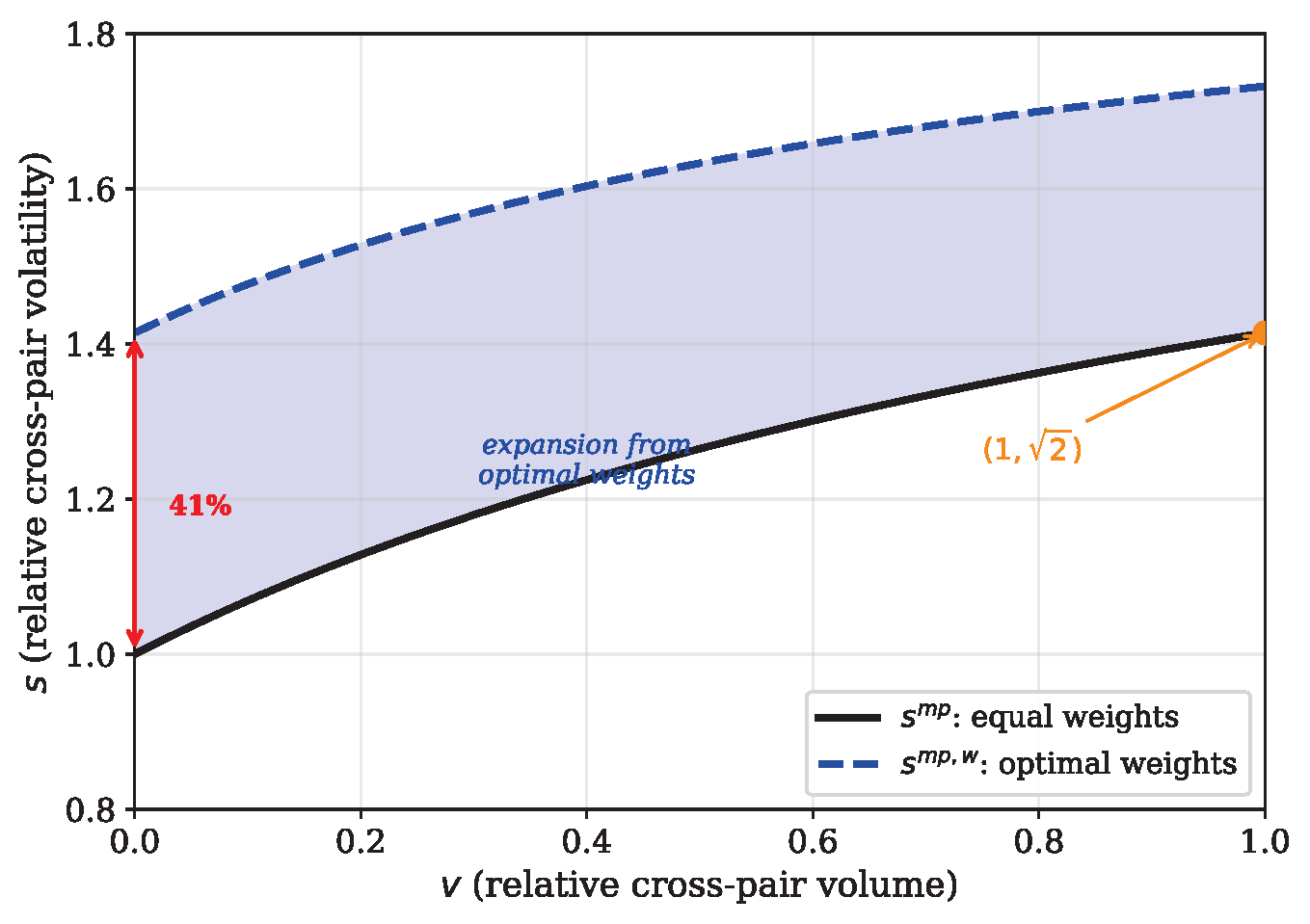

Optimal weights (AMM curve design)

More broadly: multi-asset AMM

weighted pools may yield better outcomes: \(R_0^\alpha R_1^\beta R_2^\beta=k\) with \(\beta=(1-\alpha)/2\)

Proposition: For given \(v,s\) and \(s<2\), the optimal weight for the numeraire is \(\alpha(v,s)=\frac{s}{\sqrt{(1+2v)(4-s^2)}}\).

generally speaking, when optimally weighting the pool, we expand the region of parameters where multi-lateral pools are optimal

Disclaimer: these currencies trade against one another, vehicle routing is not the issue here

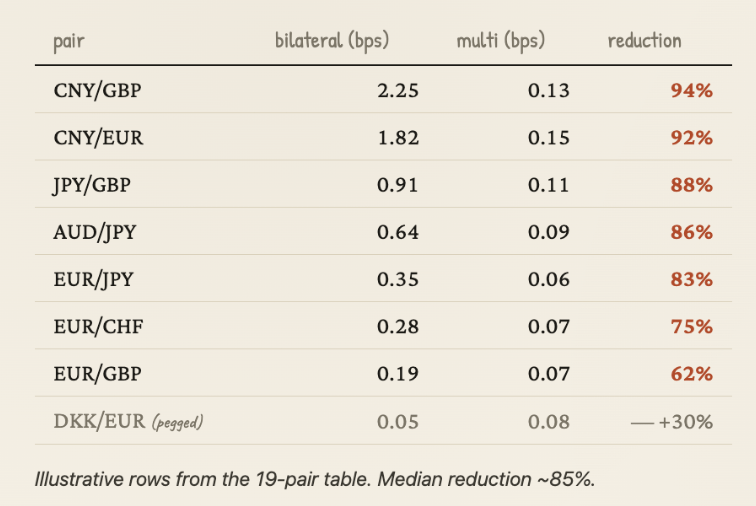

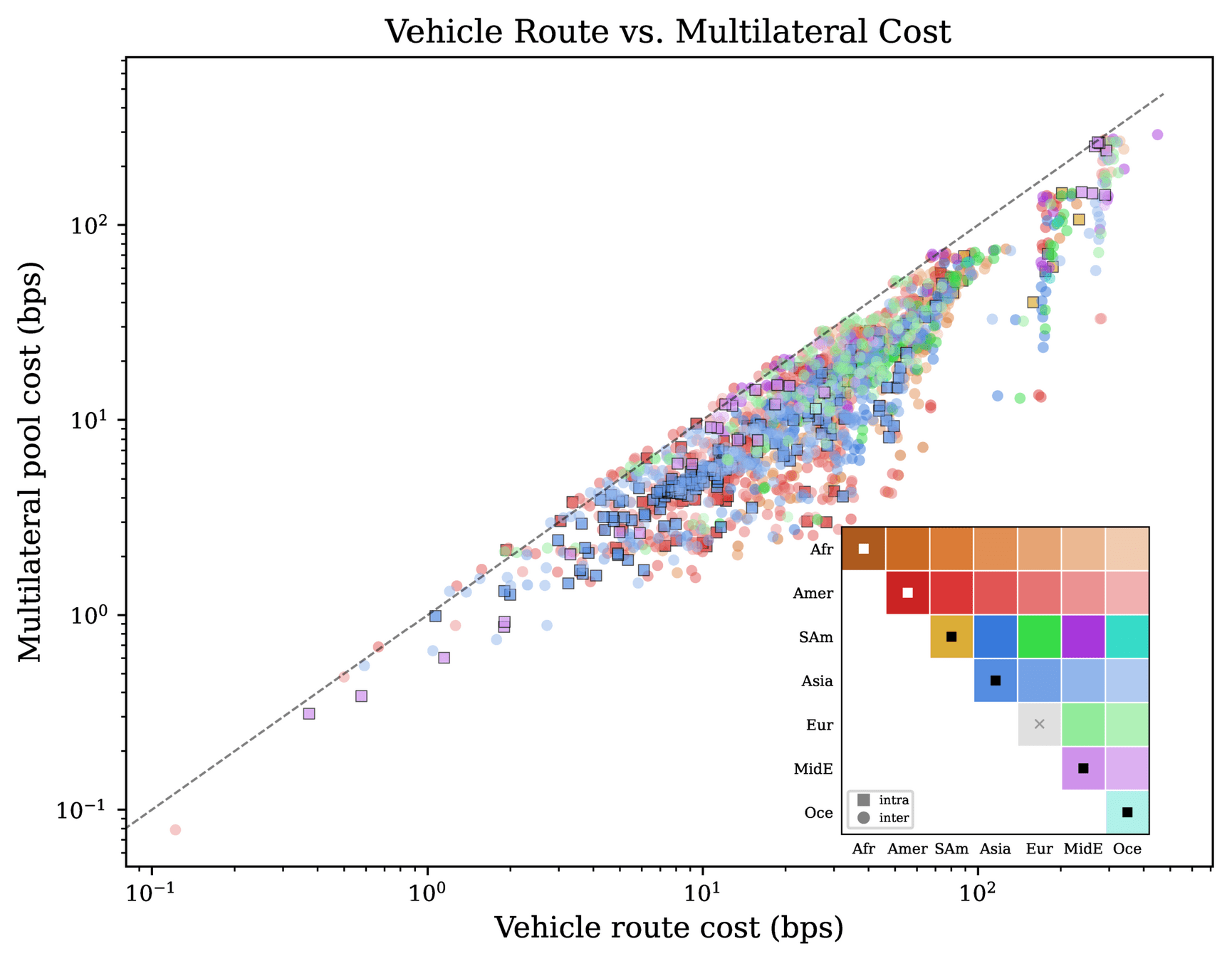

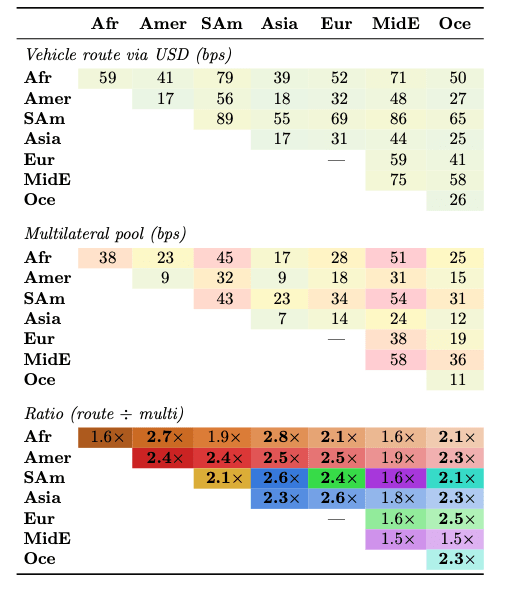

based on bilateral trade data from the IMF

Vehicle-currency routing is not a coordination failure.

In a wide parameter region it is welfare-maximizing. The dollar earns its role.

But it embeds a cross-subsidy.

Small-pair traders — smaller firms, emerging economies — pay twice so majors pay less.

A multilateral pool resolves the tension.

In the empirically relevant region it beats routing, and the cross-pair trader individually prefers it. Capital multiplexes across all pairs.

The collective of small currencies, not any one challenger, is the threat.

"High enough correlation" threshold collapses as the number of currencies grows.

Design the stablecoin FX layer accordingly.

Closed-form fees and optimal weights are ready for implementation.

Equities: easy — returns + volume, observed.

FX: bilateral volume is unobserved — because of vehicle routing.

Trade data as a proxy?

Impermanent loss:

\[\text{IL}=\frac{\text{pool value at }T -\text{pool value buy-and-hold at} T}{\text{pool value at start}}\]

\[=\left(\prod_{i=1}^nx_i\right)^{\frac{1}{n+1}}-\frac{1}{n+1}\left(1+\sum_{i=1}^nx_i\right)\]

gross return of currency i relative to numeraire 0: \[x_i:=\frac{S_i(T)}{S_i(0)}\]

Proposition: For three currencies with \(E[x_i]=1\), \(x_i:=1+\epsilon_i,\), \(\sigma_{ij}^2:=Var(\epsilon_i-\epsilon_j)\), and \(\Sigma:=\sigma_{01}^2+\sigma_{02}^2+\sigma_{12}^2\)

\[\mathbb{E}[-\text{IL}]=\frac{\Sigma}{18}\]

recall: bilateral pool \(\mathbb{E}[\text{IL}]=\frac{\sigma^2}{8}\)

liquidity invariant (equal weights \(w_i=\tfrac1n\)) \[\prod_{i} R_i^{\,w_i}=k\]

marginal rate vs numeraire \((S_0\equiv1)\) \[S_i=\frac{R_0}{R_i}\]

pool value (at market prices) \[V=\sum_{i} S_i R_i = n\,R_0\]

3-currency closed form below; for general \(n\), Li, Park, Singh & Veneris (2026) give a numerical algorithm for optimal weights and pool construction.

Lemma (equal thirds). At market-consistent prices each currency holds one third of pool value: \[S_i R_i=\frac{V}{3}\]

Proposition (price impact). A trade \(i\to j\) of size \(\Delta\) hits a sub-pool of value \(\tfrac23 V\), so \[\Pi=\frac{2\Delta}{\tfrac23 V}=\frac{3\Delta}{V}\]

Looks worse than the bilateral \(2\Delta/V\) — but here \(V\) is the whole pool. (next slide)

Trades hit ⅔ of the pool, so LPs bear adverse selection on every pair — the fee must cover it.

Liquidity providers enter until fees cover expected IL — break-even pins depth: \[F\cdot V = D_0\cdot \mathbb{E}[\text{IL}]\]

Pool designer picks \(F\) to minimize all-in cost (price impact + fee):

\[c^{\text{multi}}(F)=\frac{\Delta\Sigma}{6V}\frac{1}{F}+F,\qquad c^{\text{pair}}_{ij}(F)=\frac{\Delta\sigma_{ij}^2}{4V_{ij}}\frac{1}{F}+F\]

\[F^{*}=\sqrt{\frac{\Delta\Sigma}{6V}},\qquad F^{*}_{ij}=\sqrt{\frac{\Delta\sigma_{ij}^2}{4V_{ij}}}\]

at the optimum: price impact \(\approx 2F\) — half impact, half fee

symmetric case: multi-pool cost is

\[\sqrt{\tfrac{2}{3}}\ \text{of pairwise}\]

≈ 18% lower

Status Quo (SQ)

Two USD pools; MXN/THB routes through USD.

Three Bilateral Pools (BP)

One pool per pair; capital fragmented.

One Multilateral Pool (MP)

All three in one pool; direct trading.

Similar analysis as one pool — LPs break even, planner sets the cost-minimizing fee.

Benchmark: every pair is identical: volume \(V\), volatility \(\sigma\). We relax this with later.

By Andreas Park